Almost everywhere in life, the word “active” has a positive connotation. An active lifestyle, an active personal life, an active participant in a discussion, etc. In contrast, “passive” stands for low-energy, dull and boring. Imagine setting up a friend on a blind date with a nice gal/guy who has a really great “passive lifestyle” and see how much excitement that generates.

But investing is different. Passive investing is the rage right now! It is a noticeable market trend in finance overall and the Financial Independence blogging world seems particularly subscribed to the passive investing idea. For the most part, I agree with the superiority of passive investing. But then again, not all active investment ideas are created equal. And that means that we are at risk of throwing out the baby with the bathwater!

Has the Personal Finance Passive-Pendulum swung too far? Are we willfully ignoring some useful principles from active investing for fear of shaking the foundations of the Passive Investing Mantra?

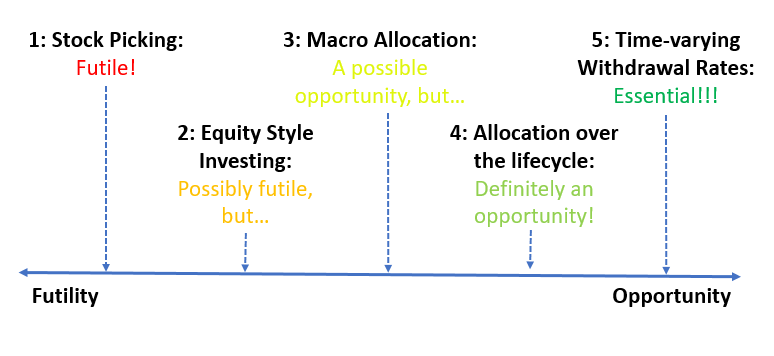

Take the following five examples of active investing. They all fall into different spots on the Futility vs. Opportunity spectrum:

- Stock picking.

- Style investing, i.e., tilting the portfolio toward a theme such as dividend yield, small stocks, value stocks, low volatility stocks, etc., or a combination of them.

- Allocation to different asset classes (e.g. stock, bond, cash, alternatives) in response macro fundamentals (P/E ratios, bond yields, volatility, etc.).

- Changing the major asset weights over the life cycle, e.g., using an equity glidepath to retirement and even throughout retirement.

- Setting the initial safe withdrawal rate in retirement and all subsequent withdrawal rates in response to changing market conditions.

It would be a mistake to apply the same passive investment mantra to all five aspects of personal finance. So, that’s what today’s post is about: Where should we stay away from active investments and where can we learn something from active investment principles? Let’s look at the five active investment themes in detail…

1: Stock picking – Futile!

The way I usually rationalize the futility of stock picking and the superiority of indexing is the following simple line of reasoning:

- All equities in a specific stock index are exactly weighted by their capitalization. By definition!

- If we split all investors into active and passive, then note that passive investors hold their investments in exactly market cap weights, by definition.

- If you start with market capitalization weights for the index and take out the chunk of passive investors who hold their stocks according to market cap weights then the remaining active investors, in aggregate, have to also hold exactly the market capitalization weights!

So, individual active investors can outperform the index but in aggregate, all actively managed portfolios can only track the index.

And, of course, once you take into account trading costs and expense ratios for actively managed funds they will likely underperform. Now, supporters of active management can argue that not all active portfolios are created equally. Maybe there are lots of unsophisticated investors. Suckers who will consistently underperform and serve as cannon fodder for the smart investors. But I doubt there are enough suckers out there to provide the excess returns for overcoming active management fees or the value of my personal time to perform the analysis myself. I’m a passive investor in that sense and recommend everybody I know to do the same.

2: Style investing – probably futile, but…

A variation on the stock picking theme is to deviate from index weights, but doing so in a systematic way. Think of this as tilting the weights of the portfolio to overweight certain styles that – hopefully – outperform over the long-run. Two prominent examples: Over the very long-term, both small cap stocks and a value stock tilt (stocks with a high book to price ratio) would have outperformed the market overall, see data from the Fama-French Factor database below.

It was a bumpy ride for the small stocks factor for the last 35 years or so. The blue line has been flat since the early 1980s, indicating that a small stock bias has not outperformed the overall index since then. The Value tilt was a bit more consistent for about 80 years and has outperformed the cap-weighted index from 1926 to 2006. But for the last 11 years, value lagged behind the index (orange line flat to slightly down).

Another popular tilt, especially in the FIRE crowd, would be overweighting dividend stocks. Some people swear by it. See Ten Factorial Rocks, Tawcan and many others. I have thought about dividend and dividend growth investing myself but never actually pulled the trigger. My concern is that styles go in and out of fashion and any excess return we might have observed in the past can quickly be arbitraged away in the future, especially considering the growing specialty ETF industry that jumps at the opportunity of offering the next hot style.

So, what’s the verdict? Sure, the value and small-cap premium might come back. Dividend stocks might save you during the next downturn. I wish all style investors the best of luck but personally, I’m not “buying it,” neither figuratively nor literally.

3: Macro Asset Allocation – a potential opportunity, but…

OK, so picking individual stocks is hard. It’s so hard that retail investors, even those with a finance background like yours truly probably want to skip this and just stick with an index fund. So, let’s look at the most die-hard Boglehead who invests x% in a global equity index fund and 100-x% in a bond fund. Is it wise to keep the target weights the same all the time? Regardless of bond yields and equity valuations? I would argue that it’s not. Nobody could have said it better and more succinctly than Warren Buffett:

“Be fearful when others are greedy and greedy when others are fearful”

Expected returns of different asset classes vary over time. I can make this case easily for bonds where, in the case of default-free U.S. government bonds, we can even read off the expected return over the remaining life of the bond. It’s the yield to maturity, e.g., currently about 2.3% for the 10-Year Treasury. That yield has fluctuated over the decades from the low 1% during the aggressive Federal Reserve accommodation to well into the double-digits in 1979-1985. But even expected equity returns vary over time. They are a lot harder to measure, but some smart folks have weighed in on that discussion:

- Jack Bogle recently pointed out that he expects only about 4% nominal returns over the next 10 years for equities.

- Another icon of the passive investing world, Burton Malkiel, author of the investing classic A Randon Walk Down Wall Street pointed out last year that equity returns may be a bit leaner going forward. (Oh, how much it pains me to link to a Wealthfront blog entry! Readers of this blog know about my opinion of the Robo advisers. Remember, we saved $42,000 by not moving money to a Robo adviser?!)

So, two of the heroes of the passive investment world, Bogle the practitioner and Malkiel the legendary finance professor, point out that equity returns will be a bit lower than usual. What should we make of this? Have these two icons of the passive investing world suddenly changed their decade-long held beliefs? Have they fallen off the wagon? Of course not. Time-varying equity expected returns are neither at odds with Bogle’s idea of indexing nor Malkiel’s Random Walk hypothesis. Remember, the stock market is, mathematically speaking, a random walk with drift (to account for the positive expected return). Bogle and Malkiel simply pointed out that the drift rate can change due to changing valuations (e.g., P/E Ratios, CAPE ratios, etc.).

Notice that Bogle and Malkiel don’t argue for selling all your equities and running for the hills. Neither do I. Bond yields are also low, remember? Actively timing the Stock vs. Bond allocation isn’t trivial. Looking at equity valuations only, you’d run the risk of getting out of equities too early; Shiller’s CAPE went above 30 in 1997, years before the equity market peak. Likewise, you could get back into equities too early; equities appeared cheap again in late 2008, months before the actual market trough in March 2009. But being cognizant about today’s underwhelming equity return expectations and watching out for the next inevitable excesses of greed (for full disclosure, I don’t believe they have arrived yet), and the subsequent period of excessive fear, will be a prudent move. But don’t call me an equity bear! Forecasting the next bear market is a futile exercise as our blogging friend Physician on FIRE pointed out just yesterday. But I admit that I have shifted a portion of the ERN family portfolio into alternative investments such as real estate and options trading in response to the poor equity and bond expected returns.

What about the recent JL Collins “time machine” post?

JL Collins had a nice post about the 1975-2015 episode showcasing all the different obstacles the stock market has overcome in that 40-year window. Also check out the excellent ChooseFI podcast featuring some of the same discussion. Does that deny the Bogle story? Quite the contrary. It actually confirms the whole valuation-based expected equity return narrative. In other words:

1975 was a great year to start investing in equities, not despite the macroeconomic woes, but exactly because of the business cycle trough in early 1975.

Specifically, 1975 was exactly one of those times with a lot of “fearful” investors mentioned in the Buffett quote. Unsophisticated investors got scared out of the market and caused the attractive, bargain-basement equity valuations with a Shiller CAPE of only 10. If you had the stomach to invest in equities and ignored the naysayers back then (JL Collins did, good for him!) you were in for a very profitable, albeit bumpy ride.

So, depending on how one interprets the Collins post I would either wholeheartedly agree or vehemently disagree with the conclusion:

- If the message is that the U.S. economy has shown great resilience during the last 42 years I wholeheartedly agree. Just like JL Collins, I am generally bullish on the U.S. economy and U.S. stocks and it’s nice to keep in mind JL Collins’ list of disasters that were unable to derail the economic expansion and strong equity performance. This post will come in handy when folks get weak-kneed following the next big drop in the market!

- If someone argues that we should disregard the Bogle/Malkiel expected return estimates because stocks performed well after 1975 and today’s economic fundamentals appear a lot better than in 1975, then I’d have to disagree. This is precisely the faulty logic of the unsophisticated investors who overreact to cycles of fear and greed, as mentioned in the Buffett quote. The prospects of good equity returns in today’s environment (300%+ equity rally, 8 years into an economic expansion, CAPE at 30) is actually worse than at the beginning of a new expansion in 1975. Now, if you think that I ignore the economic environment, I’m not; I have a Ph.D. in economics and I eat, sleep and breath economics. The forward-looking economic conditions, namely, the prospects for strong GDP growth right after the recession ended, strong earnings growth and earnings multiples expansion due to the low initial CAPE all looked very attractive in 1975. Not so much in 2017.

So again, I am not saying that the U.S. economy will falter. Don’t buy gold coins!!! I’m just saying that today’s conditions (a CAPE three times as high as in 1975) look less conducive to strong future equity returns than in 1975. Prepare for a continued bumpy ride over the next 10 and likely 40 years with slightly lower expected returns than over the last 40 years!

4: Strategic Asset Allocation over the life cycle – a big opportunity

Even the most passive investors have to make one active decision: What’s the initial asset allocation. Take the Boglehead two-fund portfolio again: global equities and U.S. bonds. What should be the percentage of the two index funds? And should that asset allocation stay the same over the entire life cycle? Research has shown that the asset allocation should ideally change over the life cycle, even completely independent of the changing equity/bond valuation landscape. The following two results hold even in pure Monte Carlo simulation simulations with Random Walk returns and constant expected asset returns over time:

- During the accumulation phase, start with a high (even 100%!!!) equity share but then scale down the equity share and increase the bond share as you approach retirement. Also known as the Equity Glidepath.

- During the withdrawal phase, the equity share should rise again. That’s not a typo! Wade Pfau and Michael Kitces wrote an excellent research paper on this topic. Yours truly also pointed out in Part 16 of the SWR series that an increasing equity allocation (80/20 moving to 100/0) is quite well-suited to making it through a hypothetical Bogle-low-return scenario for the next 10 years. I also did extensive simulations in the SWR series post on Prime Harvesting (Part 13) and showed that the success of the Prime Harvesting method in retirement comes mostly from the glidepath feature inherent in Prime Harvesting.

The reason for all of this is, you guessed it, Sequence of Return Risk (see our SWR series Part 14 and Part 15). In the accumulation phase, you shouldn’t worry much about risky investments early on when your portfolio is small. The percentage risk may be high, but the risk measured in dollars is low. But it’s best to take some risk off the table when approaching retirement with a large portfolio. Likewise, in retirement, you want to have a bond cushion early on to hedge the sequence of return risk, but then a higher equity share later in retirement, especially when facing a 50+ year horizon. Being a completely passive investor with a fixed asset allocation throughout your entire life you wouldn’t do horribly but you could likely improve the risk vs. return trade-off with a more active asset allocation. See our post on Equity Glidepaths in Retirement!

5: Dynamic Safe Withdrawal Rates – a necessity

I have written about this topic extensively. Forget about the 4% Rule! It’s should be called the 4% Rule of Thumb! Specifically, withdrawal rates should actively respond to economic fundamentals (in addition to idiosyncratic factors):

- The initial safe withdrawal rate is clearly a function of equity valuations, as we showed in Part 3 of the SWR series. If the Shiller CAPE is around 30 then a 3.25% SWR seems prudent. If the CAPE is around 10, by all means, go to town and withdraw 5% or even 6%.

- The subsequent safe withdrawal rates should respond to subsequent changes in valuations. Ideally, a CAPE-based rule, as showcased in Part 11 would do the trick. One way or another, we will all respond to changing market conditions. Even without the CAPE-based rule, retirees will eventually resort to a Guyton-Klinger-type rule (see Part 9 for details). That’s because no retiree will ever literally run out of money. Once a $1,000,000 initial portfolio is drawn down to $600,000 or $500,000 or certainly at $400,000 any sane retiree would adjust the withdrawal amounts.

Conclusion

I hope I didn’t offend too many folks in the passive investing community today. If I did, remember we probably have much more common ground than disagreement! Thanks!