The other day I was browsing on Amazon to look for the book “The Simple Path to Running a Pension Fund” and couldn’t find anything. Maybe Jim Collins is working on that right now? Or Mr. Money Mustache might have a blog post on the “simple math” or wait, I mean the “shockingly simple math” of running a pension fund? Duh’uh! Of course, there is no such simple path/simple math! Because it’s no simple task. Lots of people are involved in running a pension fund. And we’re not just talking about the operational people; customer service reps, lawyers, etc. There would also be a bunch of highly-trained investment professionals taking care of the portfolio. When I worked in the asset management industry I talked to them frequently because a lot of our clients were indeed pension funds.

And I realize that – strictly speaking – I’m actually running a pension fund right now. For a married couple like us, it has only two beneficiaries, my wife and myself. I could count our daughter as beneficiary #3 because she’ll get some money for the first two decades or her life, but strictly speaking, she’s more of a “residual claimant” who’s going to get most of the “leftovers” when Mrs. ERN and I are gone. All of us in the FIRE community are running our own little one-person or two-person pension funds. And of course, in a lot of ways, running these small-potato pension funds is a lot easier than what the big guys (and gals) are doing. We don’t need fancy buildings, lawyers, customer reps, etc. But that’s the bureaucracy side. How about the mathematical and financial aspects? I’ve obviously written about how decumulating assets in retirement is clearly more complicated than accumulating assets while working (see Part 27 of this series – Why is Retirement Harder than Saving for Retirement?) but I was surprised how my DIY pension fund faces math/finance challenges greater than even a large pension fund. So, here are seven reasons why I think my personal pension fund is a heck of a lot more challenging than a corporate or public pension fund…

1: The “Law of Large Numbers” won’t work for us

In other words, we face much more longevity risk! What do I mean by that? A pension fund with thousands of beneficiaries can rely on actuarial calculations and thus make reasonable assumptions on how many people die along the way and how that will reduce future expected liabilities. It sounds very morbid but it is actually perfectly legal and even the proper and prudent thing to do.

Let’s look at an example. Imagine a pension fund has 1,000 retirees, all 65 years old males, then we can plot how many of them will still be alive over the next 5, 10, 15, etc. years. That’s what I do in the chart below. The blue line is the share of 65-year-old males still alive at the ages plotted on the x-axis. For example, not even half of the original group makes it to age 85, according to the survival tables from the Social Security Administration. And the pension fund will have to put aside less money because of that. (side note: this is just for illustration. An actual pension fun will undertake much more sophisticated calculations taking into account more demographic characteristics, survivor benefits, etc.) A DIY pension fund doesn’t have that luxury. What most retirees will do is to assume a “reasonable” life expectancy of, say, 95 years that you don’t outlive with a high enough probability (hopefully higher than 90%) and then plan for that 30-year retirement. So, the DIY pension fund would have to plan for larger payments, see that green area, to hedge the one-person longevity risk! For full disclosure, there’s also that small red area that the pension fund has to cover past age 95, but it’s so much smaller and also so far in the future that it’s likely negligible.

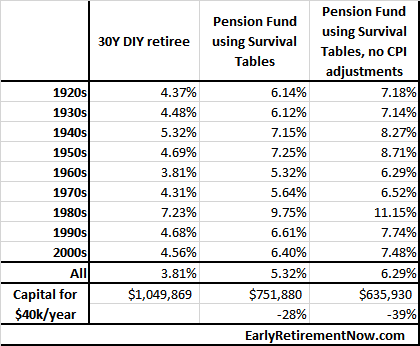

In any case, how much of a difference does that make, mathematically speaking in a safe withdrawal analysis? A huge difference! I ran some safe withdrawal simulations and looked at the two different scenarios: 1) a DIY pension fund, i.e., a 30-year retirement horizon with level withdrawals and 2) a pension fund that takes into account the conditional survival probabilities of a large number of participants and where the expected payments decline due to participants passing away.

For the results, please see the table below:

- The fail-safe initial withdrawal rate would be 3.81% for a 30-year retirement horizon with level withdrawals over that period. The worst-case scenario that pushes the SWR below 4% occurs during the mid-1960s where you have lackluster investment results for a number of years before the sequence of recessions hit in the 1970s and 1980s.

- In order to fund a $40,000 a year retirement budget, we’d need just under $1,050,000 (=40k/0.0381) to guarantee not running out of money in the historical simulations

- A pension fund using the actuarial assumptions of average 65-year olds could offer 5.32% initial withdrawals to all living participants. But over time, as participants die, the outflows will trend lower according to the Social Security survival table.

- In order to fund a $40,000 benefit to the surviving participants, the pension fund would need only about $752,000 per participant. A full 28% less than the DIY retiree! That’s because the real pension fund can average out the longevity risk among all participants.

So, in other words, a real pension fund with a large number of participants can offer a much higher fail-safe benefit than our DIY retiree. Conditional on surviving, a participant receives over $53k a year, while the DIY retiree planning on a 30-year horizon can withdraw only about $38k per year (with COLA) for 30 years to guarantee not running out of money in the worst historical episode. The pension plan would pay out slightly more initially, but then after about 12 years start paying less overall (though still paying $53k per survivor) to make up for that. See the cash flow chart below.

Also, just in case people are interested, here’s how that same picture looks like for a 45-year-old male retiree, i.e., my age. The decline in expected survivors is clearly more gradual because the initial death probabilities are smaller (phew!!!) but you can still see that large green area of “wasted” resources that a DIY pension fund needs to set aside relative to a “real” pension fund.

2: A pension fund’s payouts are (more) predictable

The pension fund has to pay what it promised to pay to the surviving beneficiaries according to some pretty explicit benefit formula. If a beneficiary can’t make ends meet in retirement with that benefit, that’s the beneficiary’s problem. Not so in my DIY pension fund. We also have tons of additional uncertainties: paying for little Ms. ERN’s college, maybe graduate school, and also our future health expenses, nursing home expenses, etc. In fact, some of the most frequent concerns and questions from readers are related to exactly this issue: people are worried about the uncertainty of health expenditures, long-term care, nursing home costs, etc. Not just the expected values but also the great uncertainty about their personal idiosyncratic expenses. In contrast to a regular pension fund, your personal DIY pension fund faces all those risks in addition to the portfolio risk!

3: A corporation running a pension fund is a “going concern” and finds it much easier to deal with future shortfalls

Before retiring in 2018, I worked for a corporation with roots going back over 200 years (!) to a bank founded by Alexander Hamilton! It also has a pension fund. Though it’s been phased out over time, I’m still eligible for a small pension when I turn 55. If that pension fund ever were to get into financial trouble, sure, the CFO would be bitching and moaning but as long as the corporation is run profitably it can and will be done. That’s a lot harder for a DIY pension fund like myself. Humans, in stark contrast to corporations, have a limited “shelf life.” It’s a lot harder for a 70-year-old retiree to replenish his or her pension fund than a 70-year-old or even 200-year-old corporation.

Of course, the mantra in the FI/FIRE community is that the solution to Sequence Risk is to just be flexible. True, I could probably get my foot in the door in my old industry again (finance/asset management) if I wanted or had to. In the next year or two! But I have no illusion that the prospect of getting a job as lucrative as my old one will dwindle over time. And that’s just the way things are: both due to our advancing age and the growing gap in our resume we’ll have a harder and harder time supplementing our DIY pension fund in the future. It may not even be hard in absolute terms – I guess I could become a greeter at Walmart – but it certainly is in relative terms; relative to my earnings potential pre-retirement. That’s in stark contrast to a corporation which will hopefully stay profitable no matter how long it’s been running. Of course, even a corporation might get into economic trouble and may even go bankrupt. But the expected rate of decline in earnings potential for a large established corporation is certainly less than for a human.

4: We face more asymmetric risk than a pension fund

Let’s face it, chances are we vastly over-accumulated assets. In other words, by the time my wife and I are gone, we’ll still have a sizable nest egg. Of course, the money isn’t wasted because our daughter will get it eventually but, still, this means that we obviously worked too long. How long is anybody’s guess but I figure I could have retired at least one year before our actual retirement date in 2018. Will I beat up myself over this? Certainly not. It’s the rational thing to do because we face a very asymmetric risk: Running out of money in retirement is a lot more catastrophic than working a year longer than I have to (unless, of course, you work in a really, really horrible work environment!!!). And in light of this kind of asymmetric risk, it’s rational to err on the side of caution. There are many examples where you do so:

- I’d rather arrive 30 minutes before my plane’s departure than 5 seconds after the gate closes. Think of all the time I’ve wasted waiting for my flight! But missing a flight is enough of a hassle, so I’m willing to pay that price.

- Imagine you prepaid your rental car’s gas. The optimal thing to do is to return the rental car with the tank completely empty. But who does that? I’d rather leave a gallon reserve in the tank before risking running out of gas one mile before the rental car agency. (and I’d miss my flight in that case, too, oh my!)

- Any kind of insurance: auto, life, liability, etc.. Or running extensive medical tests to rule out serious diseases, etc.

And any time we err on the side of caution there is this inefficiency of wasted resources. Wasted hours at the airport, wasted gas in the rental car and “wasted” money in our nest egg. A pension fund, on the other hand, has a much more balanced risk profile. The money to fund the pension plan comes from the cash flow of this going concern. It’s just a matter of when. If the pension fund is overfunded now it means that at a past date too much money was diverted from operations to the pension fund. Thus, a slightly underfunded pension plan isn’t as scary as a DIY retiree with an underwater portfolio! Which brings us to the next point…

5: A mildly underfunded pension plan might even be optimal!

Going back to the previous point, I suspect that for a corporation, not only are the risks roughly balanced. There may even be a rationale for a corporation to keep its pension plan slightly underfunded. An overfunded pension plan means that precious resources have been taken away from operating a (hopefully!) profitable business enterprise. Just to give you some numbers here: Most corporations I looked at have ROEs (return on equity) in the high single digits, even 10+%. Some of the tech companies even 20% and more, although I doubt that many of them have pension funds. Why would you divert money away from such profitable ventures and into a pension fund that’s likely very bond-heavy with returns in the low single-digits? Of course, a corporation can’t take this too far. It can’t be severely underfunded or even get rid of the pension fund portfolio altogether and promise to pay benefits from future profits. That would run afoul with the regulators. But within bounds, it indeed seems optimal to be slightly underfunded.

But for us DIY retirees, living years or even decades with an underfunded plan might not be so ideal. It doesn’t make for a very relaxing early retirement if your personal pension fund is underwater and you have to think about that Damoclean sword or retirement ruin when you’re supposed to enjoy your retirement! I enjoy my stress-free retirement knowing that we have multiple layers of safety margins! Another dimension where my DIY pension fund seems a lot more challenging!

6: Most corporate pension funds don’t offer inflation adjustments

If you have a government pension with COLA (cost of living adjustments) count yourself lucky. Most corporate pension plans don’t. So, how much of a difference does it make if a (corporate) pension fund gets to skip the CPI adjustments? Even though this is a simple question, there is no simple answer to this one. I would normally assume a “reasonable” inflation estimate going forward, say, 2% per year, and see how a portfolio would have performed in the historical simulations if we had shrunk the real withdrawals by this 2% figure every year (even though inflation has been been very different from 2% for most of U.S. economic history!!!). So, let’s do that in the context of our little pension fund example above. Let’s look at the fail-safe withdrawal rates if we assume the pension fund can also shrink real benefits by 2% per year, see the table below:

- Say hello to the 6% Safe Withdrawal Rate! Even in the tumultuous 1960s-1980s, a pension fund could have offered a fail-safe withdrawal rate that’s way out of reach of a DIY retiree like myself: More than 6% in the 1960s and more than 7% at the stock market peak before the Great Depression.

- Actually, the true historical SWRs would have been even greater because realized inflation was a heck of a lot bigger than 2% during the tumultuous 1970s and 1980s (going to double-digits in the worst years).

- So, to fund a $40,000 retirement benefit per beneficiary, the actual pension fund could reduce the portfolio size per beneficiary even further, to about $636,000, and still be confident that this would have survived even during the tumultuous past recessions. That’s 39% less than the DIY retiree!

7: Keeping up with the Joneses? Not a problem for a pension fund!

One other issue has been on my mind and this has been brought up by readers quite frequently as well: should our retirement budget increase faster than CPI inflation? You see, real GDP grows at a positive rate and that’s true even when accounting for population growth, i.e., calculating the per-capita real GDP numbers. Specifically, between 1950 and 2017, real per-capita GDP grew by about 2% annually (real GDP by about 3%, and the population growth was about 1%, so the ratio of the two grew by about 2%), see the chart below:

Do you see a problem if you adjust “only” for inflation? Over the years and decades, we will fall behind more and more relative to the average U.S. consumer. Sure, I can still afford my consumption basket from 2018 in the year 2048. But what if everyone around me has consumption budgets that grow at 2% above inflation and they can buy all those fancier gadgets? In 2048, will I feel like someone stuck in the 80s today? Maybe if you’re a traditional retiree you don’t care so much about falling behind with your gadget portfolio when you reach your 80s and 90s. But we retired at ages 44 (Mr.) and 35 (Mrs. ERN) and have many more decades to participate in the advancement of technology.

So, I simulated how different withdrawal patterns would have worked out in the historical simulations. Specifically, I ran my Google Sheet with six different assumptions:

- 2 different retirement horizons: 30 years and 60 years, i.e., traditional vs. (very) early retirement.

- For each, I look at 3 different spending patterns: “only” CPI adjustments, CPI+1% additional real growth and CPI+2% growth

- Throughout I assume a 60/40 Stock/Bond portfolio and zero final net worth target.

Let’s look a the results, see the table below. Growing your withdrawals to keep up with what your average fellow Americans’ consumption budget will dramatically reduce the safe withdrawal rates, or, equivalently, dramatically increase the required capital to fund a specific initial spending target. Just a 1% increase over the CPI requires a 13% and 18% larger nest egg for the 30 and 60-year horizon, respectively. With a 2% increase, we now push the fail-safe withdrawal rates to just under 3% over a 30-year horizon and into the low-2% range over a 60-year horizon.

Side note: the same results also apply if you assume that your personal inflation rate the posted CPI figures by 1% or 2%, also a frequent inquiry by readers. A lot of retirees are worried that their own personal inflation rate will be much higher than the average posted CPI rate when we age. You don’t even have to employ any kind of conspiracy theory (the evil government underreports CPI to lower the COLA of pensions and Social Security); older folks consume more on health care & nursing home care (traditionally high inflation rates) and less on tech gizmos (low, and even negative inflation rates).

So, in any case, maybe I’m worried for no good reason and our expenses for a healthy and comfortable retirement grow just in line with the CPI or less. But the fact that I think about this and the fact that readers have brought this up several times means I can’t ignore this issue. It’s something that a regular pension fund that offers COLA (most public funds) or no COLA at all (most corporate funds) wouldn’t have to worry about. The risk of future spending growth rates is completely outsourced to the beneficiaries!

Conclusion

Withdrawing money is harder than accumulating money, just from the mathematical and financial point of view. But I was surprised that my personal withdrawal math problem is even a bit more complicated than that of a real-world pension fund:

Accumulating Money < Pension Fund < DIY Pension Fund

The best defense against retirement uncertainty? Educate yourself! Make sure you check out the other parts of the SWR Series: a list of all parts and a summary and guide to first-time readers is available here on my new “landing page” of the SWR Series! Or anywhere else on the web! It’s harder than many people think but still easy enough that anyone can do it!