March 16, 2023 – After the tumultuous year 2022, it looked like 2023 was off to a great start. But banks threw a monkey wrench into the machine, with the S&P almost erasing the impressive YTD gains, several bank failures, and the prospect of a worldwide banking crisis that all changed. So folks contacted me and asked me if I could weigh in on this and some other issues.

Here are some of my musings about bank failures, government failures, moral hazard, and why the FDIC should eliminate the $250k limit and simply insure all deposits…

Bank Runs in Practice: The Silicon Valley Bank Failure

My blogging buddy Mr. Shirts wrote an excellent post-mortem about the stunning Silicon Valley Bank (SVB) failure, and I highly recommend you check out his post. In a nutshell:

- SVB experienced large inflows of deposits over the past few years. Most of the deposits exceeded the $250k FDIC-insured limit. That’s because many depositors were startups who received sizable cash injections from VC firms and needed to store that money somewhere “safe,” like a checking account at SVB.

- SVB wasn’t heavily involved in the traditional bank business like loans and mortgages. Startups don’t usually get traditional bank loans. So, to make money off all those deposits, SVB invested a large chunk of its assets in interest-bearing assets, like Treasury bonds, Mortgage-Backed Securities (MBS), etc. All very safe instruments with essentially zero credit risk.

- The asset portfolio was heavily biased toward longer-maturity bonds to earn more interest income. As you all recall, bonds went through a brutal bear market last year after the Federal Reserve moved up short-term rates from zero to almost 5% at the beginning of 2023, taking all longer-maturity bond yields with it for the ride. SVB learned painfully that Treasury bonds might not have credit risk, but the duration risk can be just as bad!

- With a balance sheet underwater and many fickle depositors worried about losing their uninsured deposits above the $250k limit, a bank run ensued. Customers were lined up outside their branches and wrapped around the block, invoking unpleasant memories of the 1930s. But of course, the death blow came from $42b of electronic withdrawals, nicely coordinated by the Silicon Valley VC community. With friends like these, who needs enemies?

Businesses fail all the time. A bank is a business, too, so what’s the big deal about a bank failure, then? Simple: investors now wonder how many more SVBs are out there. That’s a unique feature of the financial sector. In contrast, if you run a sandwich shop and one of your competitors goes out of business, you might even celebrate; less competition likely means more profit for you.

But in the banking sector, three bank failures in less than a week will put the entire industry under scrutiny. Everybody is guilty by association. Sometimes, even healthy banks can fail during a coordinated bank run. It would be mightily unpleasant if a bank failure in California or New York drags down the entire world banking system. As much as I am a free-market capitalist in many other aspects, there are reasons for the government to step in and assist the banking system because of systemic contagion risk.

How can healthy banks get sucked into a crisis? This brings me to the next item…

Bank Runs in Theory: The Diamond-Dybvig Model

The Diamond-Dybvig Bank Run model was published in 1983 (“Bank runs, deposit insurance, and liquidity.” Journal of Political Economy. 91 (3): pp. 401–419). Intriguingly and in an outright creepy coincidence, Professors Diamond and Dybvig received the Nobel Prize in Economics in late 2022 for this work, alongside famous macroeconomist and former Fed Chairman Ben Bernanke for his (separate) academic work in understanding financial crises. You can’t make this up; maybe the folks at the Sveriges Riksbank knew more about the coming chaos in 2023 than our U.S. regulators, but I’m not into conspiracy theories.

In any case, in a Diamond-Dybvig model (DDM), you could have a completely healthy bank with sufficient assets relative to its deposits. However, suppose all depositors, in a coordinated attack, wanted to withdraw all their deposits. In that case, the bank might not get a fair market price for all assets and must now liquidate assets at “firesale” prices. The proceeds may now fall short of satisfying all depositors.

In essence, the model creates two equilibria. If the other customers don’t withdraw their funds, I have no incentive to do so either, and the bank keeps operating as usual. On the other hand, if a critical mass of depositors withdraws money, then I don’t want to be last in line and left holding the bag. Thus, whether I need the money or not, I participate in the run, too.

So, even a perfectly healthy bank could fail in this unpleasant equilibrium. Also, the failure has nothing to do with Moral Hazard. It’s a self-fulfilling prophecy that takes down an otherwise healthy bank. As a policy recommendation, Professors Diamond and Dybvig pointed out that deposit insurance can improve outcomes and break the vicious cycle of a bank run. Note that the absence of deposit insurance can cause a bank run. And deposit insurance can prevent a bank run. It’s the opposite of moral hazard!

But for the record: SVB was not healthy!

The difference between SVB and the bank in a Diamond-Dybvig model is that SVB was unhealthy. It was underwater, not because illiquid assets needed to be liquidated at firesale prices. Treasury bonds trade in a very liquid market, and bond prices were down not because of a firesale but because the Fed raised short-term rates, shifting the entire yield curve as well. Thus, SVB was insolvent even at fair and competitive market prices, not just firesale prices. Worse, SVB was mathematically insolvent before the bank run even began! It wasn’t a multiple-equilibrium problem. There was only one single equilibrium, and that’s called “SVB is toast!”

You may ask, don’t we have regulators? How did this go undetected? This brings me to the next point…

Regulators failed!

If SVB had regularly valued its assets at market prices, a process called mark-to-market, the hole in the balance sheet would have been apparent very quickly. However, SVB used an accounting trick to hide this hole. A bank can keep two buckets of assets: assets available for sale (AFS) must be marked to market. Assets the bank intends to hold to maturity (HTM) don’t have to be written down in response to price drops. The logic behind this is that, for example, during the Global Financial Crisis (GFC), many banks feared having to write down their loan and mortgage portfolios. Nobody wanted to touch those assets, and the market priced them at steep discounts. So, on paper, a bank may look insolvent, but only when applying fire-sale-like prices. In contrast, those assets could have likely paid off if held to maturity. But this two-bucket approach helped avoid the effects of dramatic price drops of highly illiquid assets, not the market repricing of highly liquid Treasury bonds.

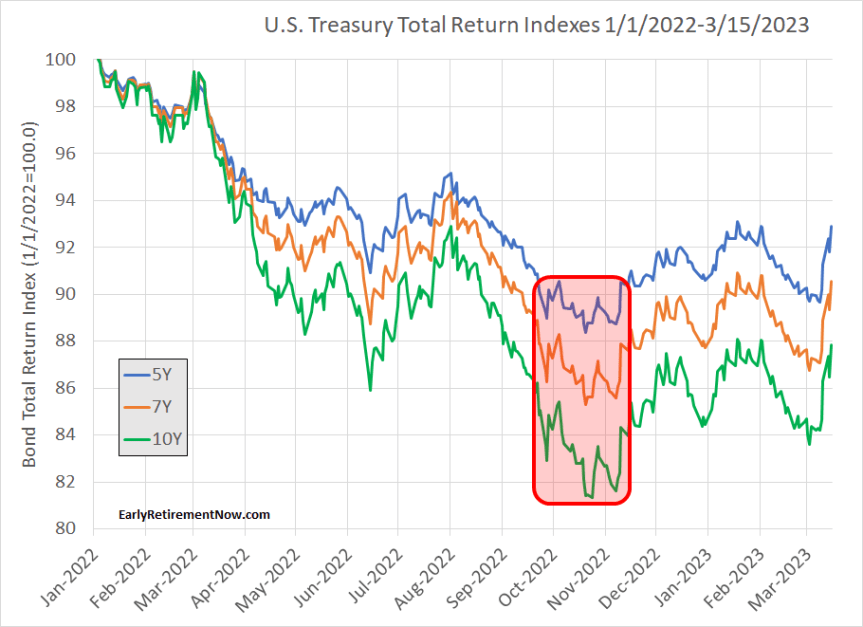

This begs the question, why didn’t banking regulators catch up to this? It’s not like bond yields just recently rallied. Indeed, U.S. Treasury yields in early March 2023 were still well below their October 2022 peaks. If SVB was insolvent on March 10, it should have been in even worse shape between late September and early November 2022. As you can see in the chart below, Treasury total return indexes have since recovered a little bit. If this is all due to a duration effect, why didn’t the CA State regulator and Federal Reserve Bank of San Francisco act six months ago? Why wait for so long to attempt to recapitalize SVB? The risk managers at SVB and the “experts” at the relevant government regulatory agencies must have been asleep!

Moral Hazard

One widespread myth is that banking crises result from Moral Hazard because reckless bankers played a game of HIWTTGBMO – “Heads I win, tails the government bails me out.” I find that story very unconvincing. Not just because the Diamond-Dybvig model generates bank runs without any moral hazard. But also because I’ve worked in finance all my life. Between 2008 and 2018, while working in asset management at BNY Mellon, I operated under the principle “If I do well, I get paid well. If I screw up, I lose my job, reputation, CFA charter, and money, and depending on the severity of the screw-up, I might be banned for life from working in the securities industry again.” I always felt those incentives were pretty well aligned with what’s best for the banking world and society at large.

The closest I came to HIWTTGBMO was during my time at the Federal Reserve: “Heads, I get a government salary and benefits, Tails I get a government salary and benefits.” Of course, I worked in economic research without any potential to cause harm to the real economy, but I’m sure that the bank examiners at the California Department of Financial Protection and Innovation and the Federal Reserve Bank of San Francisco that were asleep at the wheel will keep their jobs and pensions and will keep operating as usual after this. If people are looking for a Moral Hazard problem to solve, maybe start with the regulators!

Above all, I can’t emphasize enough that the bailout money goes to the customers, not the bank managers or equity owners. The bank leadership and employees will likely all lose their jobs, and the folks owning SVB stocks will lose their investment. By the way, we are all losers if we have money invested in U.S. equity index funds because SVB was big enough to be in the S&P 500 and certainly big enough to be in your U.S. Total Stock market Index. So we all bear the cost of the failure, and as equity investors, we should do so.

So, from a strictly economic point of view, the moral hazard problem occurs on the side of the depositors, not the bank leadership. Because depositors have coverage through the Federal Deposit Insurance Corporation (FDIC), they may indeed “recklessly” deposit their money at weak under-capitalized banks led by a bunch of Yahoos. But realistically, what’s the alternative here? There is an asymmetric information problem. Even if all of us were finance and accounting experts, we don’t have access to non-public bank records. You can’t require everyone to be CFO-grade experts for every bank we do business with! With the $6.8t Joe Biden wants to spend annually, the government should regulate banks effectively and reliably so we can all concentrate on our own businesses. You know, to be able to pay for those taxes to fund a $6.8t-a-year government!

In defense of bailing out funds above $250,000

I’ve never had more than $250,000 at any one bank. I usually keep less than $2,500 in my checking account at Wells Fargo. Of course, I have more than that at Fidelity, but the money there is in index funds, so the failure of a brokerage does not jeopardize the investment because those funds are held in custody away from Fidelity’s balance sheet.

So, since I’m so clearly below the $250k FDIC limit, does that mean I couldn’t be bothered if large businesses lose their deposits in a bank failure? Of course not. As an economist, I care about the efficient functioning of the economy, and even though I don’t have a horse in this race, I find it unfair that the FDIC insures funds only up to $250k.

Should Chief Financial Officers divert time and resources away from financial planning at their own companies to monitor the health of the financial institutions they bank with? That’s indeed what the moral hazard talking-head clowns are telling us: according to them, retail investors should not be bothered about researching banks because we’re so dumb. But suddenly, businesses are such expert financial wizards that they can see through all the asymmetric information problems inherent in banking. Essentially, they are telling us that large business clients of SVB ought to have better insights into the bank’s asset and liability positions than even the CFO and CRO (Chief Risk Officer) at SVB. And the bank client’s CFO ought to have better insights than even the government banking supervisors, e.g., the Federal Reserve, who have access to a bank’s non-public data. Come on, let’s be realistic. Business clients face the same asymmetric information problems as retail clients. If mom-and-pop checking accounts are insured, then so should business checking accounts up to any level.

And what about the advice of spreading your funds to multiple banks? It works for retail clients but not for businesses. Let’s take a medium-sized company with 1,000 employees and a monthly payroll of $10m. That company probably has at least $20m in cash sitting in a corporate checking account to satisfy monthly cash flow needs. Will we tell this company that it should just spread its money over 80 different banks to stay below the $250k limit? And if the company gets paid by a customer, will it ask for 80 different checks or 80 different ACH transfers to go to those different accounts? If businesses operated that way, they’d be busier managing their bank counterparty risk than running their own affairs. And large firms like Walmart, Amazon, Apple, Exxon Mobil, etc., probably couldn’t find enough banks in the entire U.S. to spread their cash and stay below $250k at each institution.

So, get rid of that stupid $250k FDIC insurance limit! Effectively we already have done so after the latest two bank failures at Silicon Valley Bank and Signature Bank. Why not make it official? Nothing in the Diamond-Dybvig model says we should limit the deposit insurance. Quite the contrary, the implication from the Nobel laureates is that we will keep repeating Silicon Valley Bank failures if a bank has enough uninsured deposits from large business clients. So, please spare me the Moral Hazard platitudes!

Conclusion

Back in the late 90s in graduate school at the University of Minnesota, the 1983 Diamond-Dybvig paper was one of my favorite reads. The model is simple and intuitive yet offers wide-ranging and valuable insights. Contrary to public opinion, deposit insurance leads to more financial stability, not less. I think that the concerns about moral hazard are overblown. The benefits of deposit insurance clearly outweigh the concerns over moral hazard.

So much for this week. A lot of venting today, I know. But I hope you still enjoyed it! Happy trading through this volatile market!

Thanks for stopping by today! Looking forward to discussing this more in the section below!

Title picture credit: pixabay.com