November 16, 2021 – My Safe Withdrawal Series has grown to almost 50 parts. After nearly 5 years of researching this topic and writing and speaking about it, a comprehensive solution to Sequence Risk is still elusive. So today I like to write about another potential “fix” of Sequence Risk headache: Instead of selling assets in retirement, why not simply borrow against your portfolio? And pay back the loan when the market eventually recovers, 30 years down the road! You see, if Sequence Risk is the result of selling assets at depressed values during an extended bear market, then leverage could be the potential solution because you delay the liquidation of assets until you find a more opportune time. And since the market has always gone up over a long enough investing window (e.g., 30+ years), you might be able to avoid running out of money. Sweet!

Using margin loans to fund your cash flow needs certainly sounds scary, but it’s quite common among high-net-worth households. In July, the Wall Street Journal featured this widely-cited article: Buy, Borrow, Die: How Rich Americans Live Off Their Paper Wealth. It details how high-net-worth folks borrow against their highly appreciated assets. This approach has tax and estate-planning benefits; you defer capital gains taxes and potentially even eliminate them altogether by either deferring the tax event indefinitely or by using the step-up basis when your heirs inherit the assets. Sweet!

So, is leverage a panacea then? Using leverage cautiously and sparingly, you may indeed hedge a portion of your Sequence Risk and thus increase your safe withdrawal rate. But too much leverage might backfire and will even exacerbate Sequence Risk. Let’s take a look at the details…

Some preliminary calculations

Let me first demonstrate how attractive the leverage strategy looks on paper, especially when focusing on the final portfolio value only. In the chart below, I plot the final value of both a 75%/25% and 100%/0% stock/bond portfolio after 30 years in the absence of withdrawals (i.e., buy and hold). This is for cohorts retiring between 1925 and 1990. I adjust the portfolio value for inflation using the CPI index, as usual. Quite an impressive performance. For the 75/25 portfolio, the final value ranged from $2.63 to $13.25 per dollar of initial capital. That’s a geometric average return of between 3.27% and 8.99%. For the 100% equity portfolio, the worst-case outcome was a 3.23x multiple and in the best-case scenario, the portfolio grew more than 26.4x. So, even in the worst-case scenario you still had a 3.99% real return in your equity portfolio.

If we want to model the safe spending amount when using a margin loan to fund our retirement expenses, we’d have to make assumptions about two major parameters:

What’s the interest rate for that loan? Let’s assume that over a 30-year retirement horizon, we have access to a line of credit and/or a portfolio margin loan at a (fixed) real rate. Just as a reference, Interactive Brokers which offers the most competitive margin rates (to my knowledge, at least), currently offers margin rates on a tiered system between 0.3% and 1.5% above the effective Federal Funds Rate, with the lowest interest tier starting at balances above $3m. This is for their “IBKR Pro” account.

For very large loan sizes ($4m+) you can indeed push that weighted spread to around 0.5%, but between $1m and $2m we’re looking at closer to 0.75 to 1.00%. Let’s work with a round number, 1%! If we assume that the long-term forecast for the Fed Funds Rate is 2.5%, the long-term CPI inflation forecast is 2%, and the IB spread is 1%, then we should be able to borrow at about 1.5% above inflation from our brokerage account. But I want to keep an open mind about how high or low that interest rate would be, so I will use three alternative real rates: 0%, 1.5%, and 3% just to see how sensitive the results are.

Side note: I can already hear the complaints: The most recent CPI headline inflation number was 6.2% year-over-year and I can borrow at IB for 1%. Shouldn’t I use a -5% real interest rate then? Well, you could but don’t assume that these attractive terms will last. The FOMC will likely bring interest rates back to 2.5% or above by 2024 and inflation should stabilize at around 2% before too long. Don’t extrapolate the ultra-low interest rates much beyond the next few years.

What’s the maximum size of the loan at the end of the 30-year horizon? No bank would give us a loan worth the entire 3x initial capital. Interactive Brokers, for example, mandates a minimum 25% margin requirement for stocks and mutual funds. In other words, if we start with a $1m portfolio that grows to $3m after 30 years, we’d need at least $750k net equity in the account at T=30, limiting the loan to “only” $2.25m in the final year. But even that is pushing it. Prudent investors would likely target a much lower leverage ratio for several reasons:

- There is no guarantee that brokerages and regulators will keep a promise of letting you borrow an additional $2.25m for the $750k net worth in your account. What’s worse, the greatest risk of regulators and brokerages cracking down on margin constraints always seems to come up during the worst market drawdowns. When it rains it pours!

- Most retirees will not hold their entire net worth in a taxable account at Interactive Brokers. More likely, you will hold a whole range of accounts: taxable, 401(k), IRAs, Roth IRAs, HSA, etc. But only the taxable accounts are marginable. To the best of my knowledge, you cannot borrow against your retirement account, at least not directly from your broker. Maybe a bank will give you a loan, but probably not at terms and rates comparable to the IB margin loan.

So, if you start with a $1m portfolio and figure it will grow to at least $3m after 30 years, let’s see how much of a “safe withdrawal rate” we can generate through a loan. I calculate that for different loan targets and real interest rates in the table below.

So, to summarize the calculations so far, if you start with a $1m portfolio and budget for a $3m worst-case scenario final portfolio value after 30 years, you could pull off a “safe withdrawal rate” of somewhere between 3.96% and 5.28% when facing a 1.5% real margin rate and you target a final loan size between $1.5m-$2.0m. That’s pretty amazing because this would imply a 5.28% safe withdrawal rate with capital preservation! In contrast, you’d normally just scrape by with a 4% Rule and a zero final portfolio target. What’s not to like about this approach then?

Well, the problem with the margin requirement is that it has to be satisfied not just after 30 years, but at all times along the entire retirement horizon. Let’s see how that would have worked out in some of the Sequence Risk worst-case scenarios.

A 1965 Case Study

The mid-to-late 1960s were a true nightmare from a Sequence Risk perspective. That’s because both stocks and bonds had underwhelming returns in the late 60s and early 70s, followed by three bad recessions in 1973-1975, 1980, and 1981-1982. Because of both the length of the low return phase and the depth of the mid-70s and early-80s recessions and bear markets, the 1965 retirement cohort is often considered the worst-case scenario, often worse than even the Great Depression!

So, let’s look at the November 1965 cohort and assume that this cohort had started with a $1m portfolio. In the chart below, I plot the buy-and-hold portfolio values for both a 75/25 and a 100/0 asset allocation. I also plot the size of the loan, both for a 1.5% and a 3.0% real loan interest rate. The reason I also plot the 3.0% interest rate line is that during the 1965-1995 time span, the real, CPI-adjusted Federal Funds Rate was about 2.1%, so if we add a 1% loan spread, we’ll indeed arrive at a 3% real margin loan for that 1965 cohort. Of course, there is no way of telling what margin rate anyone could have gotten around that time. I suspect that the conditions would have been less attractive than today. That’s the main reason I ignore the 0% real borrowing rate for now! A rate that low would have been difficult to get during that time!

After 360 months, the leverage strategy would have indeed worked out splendidly. The loan of $1.5m and $1.9m for the 1.5% and 3.0% margin interest loans, respectively, could have easily been paid off by the final portfolio of close to $4m. But do you notice a problem with this calculation? Somewhere around 180-200 months into retirement, during the 1982 recession and bear market, your portfolio value dropped below the loan balance. Not just for the 3.0% real rate but even for the 1.5% real rate loan assumption. Well, that’s a problem. You would have wiped out your portfolio and actually run out of money after only about 15 years. And by the way, the subsequent recovery of the portfolio during the 1980s stock market rally is irrelevant. You would have gotten a margin call from your brokerage, forcing you to liquidate your assets. And you would have gotten a bill for any potential shortfall!

That’s bad news! Most of the failures of the 4% Rule in unleveraged portfolios and over a 30-year horizon would have occurred much farther into retirement, usually past the 26-year mark. Using leverage to hedge against Sequence Risk actually made everything worse. You never liquidated a single dollar from the portfolio for over 15 years, but then you were force-liquidated exactly at the bottom of the 1982 recession.

Leverage exacerbated Sequence Risk in this case!

A 1929 Case Study

We can plot the same thing for the September 1929 cohort that retired right before the stock market blowup surrounding the Great Depression. A 100% equity portfolio would have still been depleted after only 12 years. Even the 75% equity, 25% bond portfolio came dangerously close to a wipeout in month 238 when the $1,085,000 loan was covered by a 1,185,000 portfolio. In other words, your net worth was only $100k – down 90% relative to the $1m initial portfolio – and that tiny net worth was utterly insufficient to support a $1m+ margin loan. Another margin call blowup of the leverage strategy!

What about a smaller margin loan?

The lesson so far: fully funding your retirement through a margin loan and completely forgoing any withdrawals seems too risky. Then why not try to fund only a portion of your retirement through the loan and still perform some withdrawals from the portfolio to make up the shortfall?

Again, let’s start with a $1m initial portfolio, 75/25 allocation. Assume that we withdraw $20,000 p.a. (but with monthly withdrawals of $1,666.67 each). The remaining $1,666.67 per month comes from drawing on the margin loan. In the chart below I plot the portfolio value and the loan amounts. This time I include all three interest rate assumptions, 0.0%, 1.5%, and 3.0%.

Quite intriguingly, the loan will still get precariously close to the portfolio value. Sure, we scale down the loan by one-half, but now the portfolio time series is also lower than before because we’re withdrawing funds instead of using a buy-and-hold portfolio. At the same point as before, 201 months into retirement and at the bottom of the 1982 recession, the loan-to-portfolio ratios were 93%, 84%, and just under 72% for the three alternative interest rate assumptions. That would have likely triggered a margin call in all but the most optimistic 0.0% real margin interest assumption, which would have been a bit unrealistic anyway as mentioned above.

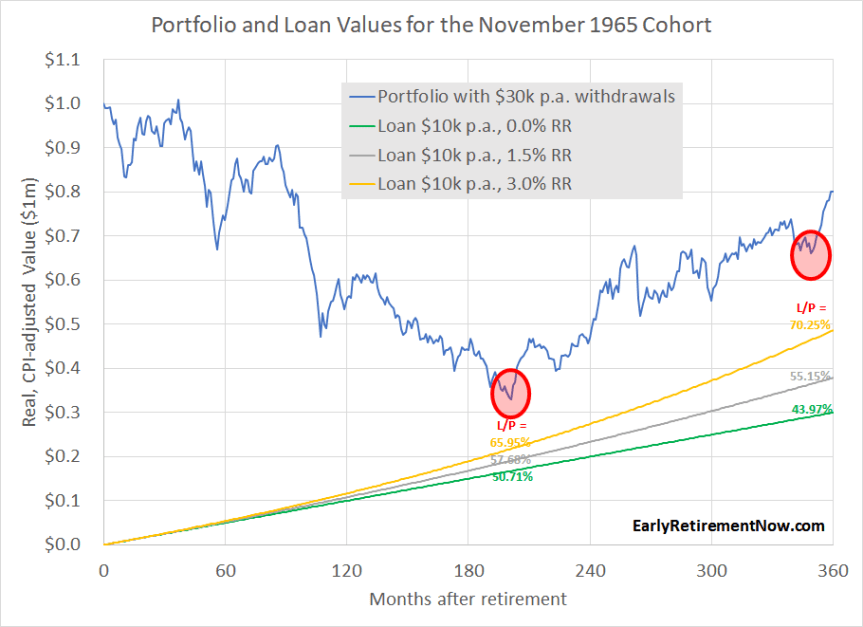

So, let’s take the leverage down another notch. Now we withdraw $30,000 p.a. from the portfolio and supplement it with $10,000 in annual draws from the margin loan. All done at a monthly frequency, i.e., $2,500 monthly portfolio withdrawals and $833.33 of monthly draws from the margin loan.

Now results look a little bit more palatable. Even with a 3% annual real interest rate, the loan to portfolio value always stays at 70% and below. Surprisingly, the largest margin utilization now occurs in 1994, right around the stock market volatility surrounding the Mexican Peso Crisis. With a 1.5% real margin interest rate you might have even stayed well below 60%.

But make no mistake: when your $1m initial portfolio is depleted by almost $700k after only 17 years and you also have a margin loan to service, this would have been a scary ride, because in 1982 nobody had any idea that the subsequent strong equity bull market would save your behind and the rest of your retirement. Recall the “The Death of Equities” Business Week cover from around that time and you be the judge if you had been comfortable with a $330,000 portfolio, a $200,000 margin loan, and $40,000 of annual withdrawals!?

Just for completeness, I also want to produce the same chart for the 3% plus 1% loan withdrawal strategy for the 1929 cohort. With similar results: The margin constraints seem OK, even when using the 3.0% real interest rate loan. Though, it must have been a tense retirement experience because the loan value would have come within just $200,000 of wiping out the portfolio.

Conclusion

If you’re a regular reader here on the ERN blog, you will notice that today’s material has a very similar flavor to my old classic post about the infamous blowup of an obscure derivatives trading firm in Florida: “The OptionSellers.com debacle: How to blow up your portfolio in five easy steps“. If they had been able to hold on to their portfolio of short natural gas futures options until expiration, they would have made a solid profit. But margin calls in between and the forced liquidation of all positions wiped out all customer accounts. And the same is true here: A strategy that may look attractive in the long-term could be subject to volatility along the way with catastrophic losses up to and including a complete wipeout of the portfolio. So, using excess leverage in retirement, specifically, funding most or even your entire retirement budget with a margin loan will likely exacerbate Sequence Risk if we were to have a repeat of the 1965-1982 asset return pattern. Unless you are so rich that, say, a ~1% initial draw rate is all you need to live comfortably. That leverage strategy works well for the 9-figure net worth households, but maybe not for us “lesser millionaires”!

But I have to concede this: If the margin loan is used cautiously to supplement the withdrawal strategy, we might have a winner here. It looks like a good point to start would be to target a 4% total spending rate, funded through a 3% withdrawal rate from the portfolio and another percentage point coming from a margin loan. Historically, that would have worked out extremely well. A 4% consumption rate would have never failed, and you would have ended the 30-year retirement window with a very solid net worth, even for the worst-case cohorts like 1929 and 1965. A possible improvement of this strategy would involve timing the margin loans, e.g., using the loan only after the portfolio drops below a certain level. Please see Part 52 for that research!

Thanks for stopping by today! Please leave your comments and suggestions below! Also, make sure you check out the other parts of the series, see here for a guide to the different parts so far!

Title Picture credit: pixabay.com