After a three week hiatus from our safe withdrawal rate research, welcome back to the next installment! If you liked our work so far make sure you head over to SSRN (Social Science Research Network) and download a pdf version. It’s a free 47-page (!) pdf working paper covering parts 1 through 8:

But let’s move on to part 11. In our previous posts (Part 9 and Part 10), we wrote about the Guyton-Klinger dynamic withdrawal rule and why we’re not great fans. Add to that our two-month-long bashing of the static 4% rule and people may wonder:

What withdrawal rule do we like?

True, we proposed a lower initial withdrawal rate (3.25-3.50% depending on future Social Security income), but that’s just the starting point. We have written here and elsewhere that this withdrawal rate is not set in stone. How do we go about adjusting the withdrawals in the future? How did different dynamic withdrawal rules perform in the past? How do we even measure how much we like a withdrawal rate rule? Today, we like to take a step back and gather a list of criteria by which we like to evaluate different (dynamic) withdrawal rules. Then simulate a bunch of withdrawal rules and assign grades.

Withdrawal rate rules we consider

- The Fixed 4% rule: Set the initial withdrawal amount to 4% of the portfolio and then adjust by the CPI every month.

- Guyton-Klinger with a 4% initial rate. +/-20% guardrails and 10% adjustments. For a primer on what this rule does and some of the skeletons in the closet, check our previous posts on that topic, Part 9.

- The same Guyton-Klinger rule but with a 5% initial rate.

- Constant percentage: withdraw a fixed 4% p.a. of the portfolio over time (i.e., 0.333% each month).

- The Variable Percentage Withdrawal (VPW) rule, see the Bogleheads link on this, assuming a 40-year retiree (mid-point between Mr. and Mrs. ERN’s age at our planned retirement date). The same mechanics as the constant percentage, though we start at 4.6% and increase the rates based on the remaining life expectancy, calculated by smart folks at Bogleheads. In our simulations we cap the withdrawal rates at 8%, though, to ensure we don’t deplete the principal in year 60. We still like to leave a nice size bequest.

- A rule based on the Shiller CAPE: Calculate the Cyclically-Adjusted Earnings Yield (=1/CAPE) and use this as a proxy for expected equity returns. Then set the withdrawal rate to W = a + b*CAEY with the appropriate parameters for a and b. The first time I encountered this rule was at the cFIREsim site where they use this exact parameterization as their default values: a=1% and b=0.5. (There is some science behind the parameter choice and we will deal with the details in a later post!)

- Same as 6 but with a=1.5%, i.e., shift up the withdrawal rate in 6 by another 0.50% p.a.

- Same as 7 but with a=2.0%.

Here are our criteria to grade the different withdrawal rules:

- Respond to changing fundamentals in financial markets and the economy

- Provide guidance on the appropriate initial withdrawal rate

- Withdrawal amounts should display low short-term volatility.

- Withdrawal amounts don’t suffer significant and long-lasting drawdowns.

- Withdrawals have the potential to maintain purchasing power over at least 30 years

- The initial withdrawal amount is not unnecessarily low.

We will elaborate more below. For now, they should appear pretty intuitive, albeit a bit subjective. For example “low short-term volatility” means different things to different people. We will grade those criteria on a scale A = best, F = worst.

Simulation assumptions

- 80% equity, 20% bond share (S&P500 total return and 10-Year U.S. Treasury Benchmark Bond total return).

- 60 years horizon, with actual returns Jan 1957 – Dec 2016.

- Monthly simulations.

Simulation Results

Apparently, 1957 wasn’t such a bad year to start retirement. At least the 4% rule didn’t run out of money! But also notice the bumpy road during the first 30 years with a significant reduction for most of the withdrawal rules during the 1970s. In the table below we report some more stats on the final portfolio value and the withdrawals over time. Notice that the 4% rule would have accumulated a massive portfolio, more than 4 times the initial size. And that’s adjusted for inflation! So, there was ample opportunity for adjusting the withdrawal amounts upward.

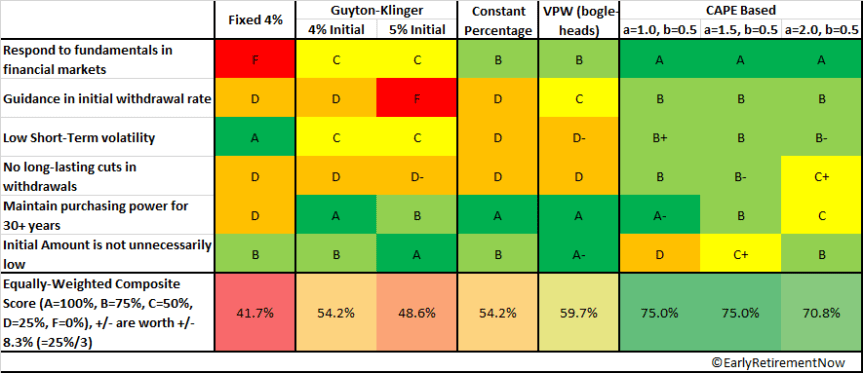

And here’s the Report Card

The summary of the grades we assigned here is in the table above, completely subjective and open for discussion, of course! The explanation of the grades follows.

1: Respond to fundamentals in financial markets

The top performers here are the CAPE-based rules. We set our withdrawal amounts not just based on price movements but also based on economic fundamentals (earnings yield), which earns a big fat A.

The Constant percentage and VPW both get a B because they clearly react to changes in financial conditions. If your portfolio is down by x% your withdrawal amount goes down by roughly x%, so you can’t blame it for not being responsive. But both rules lose some points for chasing price movements only and ignoring economic fundamentals (earnings!). You will overreact with the withdrawal amounts during the late 1990s equity bubble and also slash withdrawals dramatically during an equity market downturn when prices overreact on the downside.

Another notch down is Guyton-Klinger. That rule responds to changing asset prices but potentially with a delay of multiple years. You wait until you hit one of guard rails! Sorry, you get only a C for that. Of course, the static 4% rule gets an F for being completely oblivious to what’s going on in the world out there.

2: Guidance in the initial withdrawal rate

Both the fixed 4% and Constant Percentage 4% rules get a D. The 4% Guyton-Klinger Rule gets a D as well. Just picking some arbitrary percentage number is not sufficient. As we showed before in part 3 of this series, the 4% rule has very different success probabilities depending on where we are in the earnings yield cycle. The Guyton-Klinger rule with a 5% initial rate gets an F for its deceptive marketing. Sorry, but this rule cannot magically generate 1% p.a. excess return (alpha), see our posts from the last two SWR posts, here and here.

The VPW gets a C. It’s still not very good guidance given their percentage is also oblivious to market conditions, such as equity earnings yields and thus runs the risk of being too low if stocks are cheap or too high when stocks are expensive. But the effort of setting the initial withdrawal rate in response to different asset allocations and ages definitely earns the VPW a nice solid C. The CAPE-based rules get a B for at least thinking about different initial equity P/E ratio regimes. But there’s still some ambiguity about what the appropriate values for a and b should be.

3: Short-term Volatility

In retirement, we obviously have some spending flexibility, but we don’t like to go from top to flop, e.g., from a very generous travel budget in one year to a zero travel budget in the next year. We like to keep year over year withdrawal amount fluctuations to a minimum.

The simple 4% rule gets an A for having, well, zero volatility in the withdrawals. Though, when you are unlucky enough to run out of money that would be the mother of all short-term volatility, i.e., -100%. We are generous and decided to penalize the 4% rule grade in categories 4 and 5, not the short-term volatility grade, though.

Guyton-Klinger gets only a C. There is some pretty significant volatility year over year and the worst Y/Y drop is more than 25%. The CAPE-based rules have much more subdued year-over-year volatility, by construction, and get a nice, solid B; a B+ for the less aggressive rule with a=1.0% and a B- for the more aggressive rule with a=2.0%.

Both the constant percentage 4% rule and VPW get a big fat D on this one. Your withdrawal amounts become just about as volatile as your portfolio. And keep in mind that these numbers are already smoothed 12-month average withdrawals. The drawdowns peak to bottom are the same or worse as the portfolio drawdowns. To us, this seems quite undesirable. Of course, someone at the Bogelheads forum seems to claim that the VPW actually smoothes the withdrawal amounts:

“Q: Why not simply use a Constant-Percentage withdrawal instead?

A: Because VPW takes into account your current age, and allows you to eat more and more into your capital, as you age, while trying to smooth out the withdrawals.”

Though the first two claims (taking into account the age and generating an orderly exhaustion of capital all the way to age 100) are true, the VPW doesn’t do much smoothing at all. It’s just as volatile and even slightly more volatile than the Constant-Percentage Rule, and hence gets penalized another notch to a D-! The VPW percentage withdrawals increase over time and, true, if you’re lucky and increase the age-dependent withdrawal rate in a year with negative returns you would cushion the drop a little bit. But if you increase the VPW value in a year with positive returns you’d exacerbate the volatility. Most of the variance in withdrawal amounts still comes from the portfolio returns and, for all practical purposes, this method generates highly volatile withdrawal amounts.

4: No significant drawdowns in withdrawals

This was our pet peeve with Guyton-Klinger. We don’t like a multi-year or even multi-decade reduction in our standard of living. It’s easy to smooth out yearly fluctuations with some smart budgeting and a side gig here and there. But significantly reducing spending for 10-20 years means going back to work. Something we like to avoid.

Well, the 4% rule never has a drawdown until it runs out of money. As we showed in previous posts, the risk of running out of money is a serious concern when targeting 50 or 60-year horizons and considering today’s lofty equity valuations. Only a D grade here. Even though the 1957 starting date saw a great success of the 4% rule!

Guyton-Klinger, the Constant 4% and VPW all get a D on this one. The 5% Guyton Klinger even a D-. Some of the stats like the drawdown peak to bottom are truly scary.

Finally, we were very positively surprised about how smooth the CAPE-based withdrawal amounts were. The drop in withdrawals also lasts long, but it is a lot more shallow than for the other rules. Example: The intermediate rule starts at 4.5 in 1957, goes to a bit over 5.0 during the first decade, drops to 3.6 during the late 1970s and 1980s and then recovers again. During the volatile years since 2000, the declines in the withdrawal amounts were also shallow and short-term in contrast to the other rules. Good job, CAPE! We assign a B, B- and C+ for the three CAPE-based rules.

5: Maintain purchasing power after 30+ years

This one has a similar flavor as item #4 but it still a slightly different animal. We want to avoid a slow and permanent erosion of purchasing power, see illustration below:

The 4% rule has a 2.5% probability of running out of money after 30 years (80% stocks, 20% bonds), but a 37.2% probability of not maintaining 100% of its purchasing power. That doesn’t get you more a D grade in our household, and that’s when we feel generous.

Guyton-Klinger definitely does much better. True, it suffers from potentially year-long, even decade-long drawdowns in withdrawals, but after 30+ years you’re likely back to the initial net worth and the initial withdrawal amounts. In fact, if anything, you might withdraw too little and over-accumulate because the withdrawal rate is likely to be stuck at the lower guardrail. GK gets a nice solid A for the 4% initial rate and a B when starting with a 5% rule.

The constant percentage 4% rule rate gets an A because over the very long haul the expected real return of your 80/20 portfolio is higher than 4%. VPW gets an A as well. It’s obviously designed to exhaust the capital but the withdrawal amounts definitely have an upward moving trend.

The CAPE rules get grades between A- and C, depending on how aggressive you structure the parameters. Especially, the rule with a=2.0% might be a notch too aggressive and could create a slow erosion of real withdrawals over time.

6: The initial withdrawal is not too low

Any rule that withdraws a crazy low initial amount might ace some of the other criteria above but is still useless. All rules with 4%+ initial withdrawal rates clearly pass this criterion. The CAPE rules will likely fall below that 4% withdrawal rate most of the time. They had pretty competitive initial withdrawal rates back in 1957, but today, we’d be looking at only 2.7% when using the most conservative parameters (a=0.01,b=0.50) to 3.7% with the more aggressive parameters (a=0.02, b=0.50). That’s quite unattractive. But intriguingly, the one with parameter a=1.5% generates an initial withdrawal rate almost exactly at the 3.25% we proposed earlier in Part 3, and its overall grade is the highest (tie with a=1.0%). So, this might be something we will apply in our own withdrawal strategy!

Conclusion

Today’s case study taught us a lot. For a change, we intentionally didn’t look at a worst-case retirement date. 1957 was a pretty decent starting date that would have preserved the purchasing power of the classic 4% rule. But the path was rocky! The recession in the 1970s, the dot-com bust, and the Global Financial Crisis would have caused some crazy swings in the withdrawal amounts of the dynamic rules.

The Guyton-Klinger rules, Constant Percentage 4% and VPW all beat the Fixed 4% Rule. The CAPE-based rules perform a lot better at least according to our subjective grading scheme. They may afford a slightly lower initial withdrawal amount but the lower volatility going forward might be worth that cost.

Thanks for stopping by today! Please leave your comments and suggestions below! Also, make sure you check out the other parts of the series, see here for a guide to the different parts so far!

Thanks for a great post and a great addition to a very interesting series!

I was wondering if you plan to try to test this with your Monte Carlo engine to see how the different methods would look under different series of returns.

I’m specifically curious about the CAPE methods. While they seem to have done well in this analysis, it bugs me that they may actually encourage you to drain substantial proportions of your portfolio in the worst times possible. For example, in the beginning of the 30’s CAPE was around 6. Even according to the conservative method this would result in a WR of around 9%.

It could be that the fact that the rule tames you from withdrawing too much in times of expansion compensates for this high WR and helps it achieve the relatively smooth withdrawal, but this can be better seen in the multiple-scenario MC simulation.

Thanks!

The difficulty with Monte Carlo is that it’s hard (impossible?) to draw from a joint distribution of returns and CAPE values.

I had to try really hard to like the CAPE rules but I rationalize the high withdrawal rates as follows: When the market is close to the trough you also expect high returns going forward. If the expected real equity return is roughly the CAEY and I withdraw 1% + half the CAEY I should still recover. The multiplier in front of the CAEY is crucial here. It has to be far enough below 1.0 to create that mean-reversion in the portfolio value despite withdrawing a higher rate when the portfolio is down.

Cheers!

ERN

Thanks!

I understand the difficulty… Presumably since there’s a correlation between between market behavior and the CAPE it might be possible to simulate a CAPE for each randomized scenario. But at the same time this would be an artificial derivative of the simulated market value rather than a real market fundamental, so I’m not sure if it’d add anything.

Anyway, a conservative investor could use different parameters. If a = 2 and b = 0.25, you get a withdrawal which is less volatile percentagewise but more volatile moeny-in-your-wallet-wise. In other words, you’re moving a bit closer to the fixed percentage method. This might also fit less aggressive investors (e.g. 70-30 or 60-40) who will not fully participate in market recoveries.

Thanks!

Exactly! a = 2 and b = 0.25 would imply less than 3% right now, so that’s quite conservative.

Cheers!

Great post, as usual! Thanks, ENR!

One thing which I did not get is the low grading of the 4% rule on the preservation of purchasing power. If the rule presumes that withdrawals are adjusted for inflation, how can it be that “it doesn’t maintain purchasing power in 37.2% of cases”? Thanks.

OK, I was being a bit harsh on the 4% rule. It didn’t run out of money in this particular example and that means you preserve purchasing power for 30, even 60 years. The danger is that if you retire in the wrong cohort, the withdrawal will drop to 0. There isn’t just the loss of inflation adjustment, there is the loss of all income. The mother of all risks!

Big ERN, you’re amazing. Simply, amazing.

Great, thanks for stopping by and the mention on Twitter. Glad you liked today’s post!!! 🙂

Great post ERN!

I love how you manage to politely call bullshit on urban myths, but then pull together the data that demonstrates why they don’t stand up to scrutiny… and then for bonus points you offer alternatives that may work better and explain why.

Thanks for putting in the time to educate the community, much appreciated.

Ha, awesome way of putting it! Thanks for stopping by!

Cheers!

Thank you ERN! Great analysis. Did you by chance run numbers with a less aggressive ptf? (Maybe 60/40 instead of 80/20). I’ve been struggling myself to find/develop a planning approach that reflected both market fundamentals and ptf balances over time without the significant SD in VPW. Best I could figure was to use VPW with all time high ptf balance less a % for estimated DD’s (in my case, with 60/40 ptf I used a DD allowance of 20%). This helped avoid taking high DDs in frothy markets, but I was still left with more than desirable volatility in withdrawals over time. I like the CAPE analyses you provided here, but wonder how a 60/40 ptf would hold up, and how much SD there’d be in the withdrawals over a 35-40 year retirement.

Thanks!

60/40 would have been a disaster in the 1970s. The drawdown using VPW would have been even slightly worse. It’s a “pick your poison” situation: You have lower short-term SD, but because the average return of a 60/40 is a lot lower than for the 80/20 you’re bound to run out of money in the long-term. There’s no free lunch from bonds. Especially now with nominal 10Y yields at 2.5% I wouldn’t keep 40% in an asset with <1% real return expectation.

Thanks for the quick reply!

I understand your point about the either/or nature of the decisions —especially if including more bonds/FI investments in the ptf…and it’s those trade offs that interest me. 🙂 I do still suspect there’s something more in the CAPE approach that can help those of us who are more risk averse. I’ll look forward to your future post on choosing the most appropriate parameters as I expect it may answer (or lead to a way of answering) how different parameters affect the outcomes of different ptf’s over time.

Thanks again. Your posts are very thought provoking! NL

Thanks! Awesome! 🙂

As always great analysis ERN. Do you have any plans to analyze the cape a and b values across a wider time period for suggested values. You indicated 1.5 to hit your desired withdrawal from the prior analysis, how does that fit in your previous runs over time?

Thanks! I most definitely plan to study more the sensitivity of outcomes to changing the parameters. Planned for a future post! 🙂

Cheers!

Perhaps another point for anyone considering the CAPE methods is that the global CAPE is at the moment a bit under 21, which gives a more attractive starting WR.

That’s a great point! A difference of 1.3% in the CAEY!

Another thing to consider: We’ll soon roll out the bad earnings numbers during the global financial crisis. So the CAPE numbers will come down a little bit just from that.

Thorough analysis as always, ERN. And thanks for making available parts 1-8 in a pdf, I just downloaded it!

Ideally, my preference is to not have to fluctuate withdrawals much at all in retirement. Sure, if the market goes down 30%, I may choose to cut back on my vacation budget and here and there, but I’d prefer to rid myself of these worries in retirement. No, that doesn’t mean I lean towards the 4% SWR, but instead perhaps I work a couple more years to pad the retirement accounts more. It’s conservative, but I’m leaning towards a 3% SWR or even less. I’ll hopefully have a long retirement and prefer that peace of mind over a few more years on the job.

Thanks! Agree, for folks in the frugal crowd I can see that the withdrawals shouldn’t increase by too much. What are we going to do with all that extra money? Buy a boat? Maybe we should assume a ceiling on the expenses, pocket the extra money and leave a big bequest to a charitable cause.

But I’m still worried about the downside variation.

Big ERN,

Your posts are always a highlight of my day when they appear. Thank you!

Long time reader of ER/FI blogs; one of the oldest that I have read since it first appeared is John P. Greaney’s blog. To deal with the 4% terminal value issue you discuss above, Mr. Greaney put forward what he termed the Pay Out Period Reset (POPR) where he states “[i]f you started your withdrawals in 1997, and your portfolio grew by 20% in 1998, you could decide to use your December 31, 1998 portfolio balance to start a new pay out period. This would result in a higher inflation adjusted annual withdrawal. If your portfolio had lost value during the year, you would base your annual withdrawal on your “all-time high” December 31st portfolio value, plus an inflation adjustment. Adopting this practice greatly reduces the likelihood that you’ll have a large net worth at the end of the pay out period.” (http://www.retireearlyhomepage.com/popr.html)

Assuming you address the shortcomings of a 4% WR by adjusting down to a more reasonable 3.25% – 3.5% WR for a 40+ year retirement, would POPR help mitigate your criticisms of the fixed, inflation-adjusted WR rate? With your programming skills, I am hoping you can run the numbers and add POPR to the mix.

Unless I misunderstood the rule proposed on that page, it seems to suggest you increase the withdrawals in line with market moves when the market is up, but keep the withdrawals at the previous peak plus CPI-adjustment otherwise. So, the max you should withdraw under that rule is the absolute worst-case failsafe withdrawal amount. Definitely way below 4%. 3.25% seems about right.

The advantage is that you have only upside volatility, never downside. The disadvantage is that if a future SWR falls below what we now believe is the fail-safe level, we’re screwed. And the initial WR might be really, really low. I’ll see what’s the best way to implement/simulate that rule.

Big ERN,

Must have re-read this blog entry half a dozen times trying to divine the true depths of the mysteries it explores.

As a result, I have some more tasty vittles for your financial prowess to chew on. Seems like everything old is new again. Turns out Mr. Kitces has “rediscovered” the magic of POPR and, heaven forbid, we can’t use the same name, so he calls POPR the “ratcheting safe withdrawal rate”: https://www.kitces.com/blog/the-ratcheting-safe-withdrawal-rate-a-more-dominant-version-of-the-4-rule/ . Very nice discussion and analysis by Mr. Kitces to take my worries away from the (almost) interminable pressures of a thankless j*b. Let’s shorten the appellation for Mr. Kitces’ “discovery” to RSWR.

Left alone to my own devices, I simply cannot leave well enough alone when it comes to avoiding the terminal value issue. If we can do a RSWR rolling forward in time, why can’t we take the fact that we can roll-back in time using standard discounting equations? Take the case where a retiree quit w*rking in 2009. A 4% SWR would be both ludicrous and (likely needlessly) painful given the (hopefully) inevitable resurgent stock market. If this retiree was following a fixed asset allocation in retirement (i.e., 70/30), why not “roll-back” in time (use known returns of the assets to adjust the value of portfolio additions and any changes to asset allocation) to what the retiree’s “Peak Wealth” effectively was before the precipitous fall in asset prices and determine the SWR (based on the analysis elsewhere in your blog) and use that to calculate a withdrawal amount that can then be “rolled-forward” with CPI adjustments. This would be your “Nominal Distribution”. Put the two pieces together and you have “Peak Wealth Nominal Distribution” or “PWND”. PWND (double entendre is quite deliberate) helps with the terminal value problem and gives the retiree some guidance/reassurance on withdrawal rates after a steep decline in asset prices.

Thanks for this very thoughtful comment!

First of all: Kitces lost a bit of credibility by fudging his return numbers to make the SWR higher: In his ratcheting post he uses 1-year T-Bills (because they avoided the bond meltdown in the 1970s) and in his post on the 2000s experience (https://www.kitces.com/blog/how-has-the-4-rule-held-up-since-the-tech-bubble-and-the-2008-financial-crisis/) he uses 10-Year Treasury Bonds because their return was so good during that time. So his 1985 retiree from the ratcheting post holds T-bills during the 2000s and the year 2000 retiree holds 10Y bonds during that same period. Somewhat fishy.

But back to the question at hand: Both the Kitces ratcheting rule and the POPR are special cases of the Guyton-Klinger procedure. Both have a no guardrail as a floor (don’t ever reduce spending,i.e., lower guard rail = -infinity) and they have different rules for upward adjustments. Kitces has a +50% guardrail and a +10% spending adjustment and the POPR has a one-for-one upward adjustment, i.e., a zero guard rail and infinite adjustment.

Both special cases of GK are worse. Substantially worse:

1: In today’s environment with a high CAPE (https://earlyretirementnow.com/2017/03/29/the-ultimate-guide-to-safe-withdrawal-rates-part-12-cash-cushion/) I’m more worried about having to downward adjust my spending. I like to have a systematic way of doing so. CAPE-based rules accomplish that, so does GK, though not all that well. Switching off the one feature in GK that I liked at least somewhat will GK only worse.

2: Kitces’ rule with the +50% guardrail will likely be completely irrelevant for today’s retirees. In other words, if you start with a 60/40 portfolio today, you will have a zero probability of reaching that +50% portfolio level in real inflation-adjusted terms over the next 10 years. We’d need to generate around 8% real return to reach that +50% guardrail.

About your proposed solution: True, nobody would want to withdraw only 4% at the bottom in 2009. Withdraw 4% from a portfolio a few years ago before when we reached peak wealth and apply a very conservative SWR. I guess the historical fail-safe minus another cushion. Another option: Instead of seeking the peak wealth, pick a “normal wealth” period (not too high, not too low) and apply a normal SWR to that one. But that is essentially the CAPE-based rule. Because the “normal wealth” level would be the time when equities are closer to the historical average CAPE.

Cheers!

I tested what I believe to be this “system” on Cfiresim. It seemed to stand well when compared alongside GK, CAPE, and the other strategies.

In my opinion, the best implementation of this method was:

– Spending plan: percentage of portfolio

– Yearly spending: 2.7%

– Floor spending: percentage of previous year

– Never less than: 100%

– Ceiling: no ceiling

It starts with a low withdrawal, but I don’t think that’s so bad. When viable it adjusts upwards to a more comfortable amount, and if it doesn’t then I’d argue it’s for a very good reason.

I understand the apprehension about the fact that it doesn’t adjust downwards. Though if I remember correctly, in the simulation the lowest total reserves were higher than both GK and CAPE, as was the lowest spending. It also had a good median withdrawal and median reserves.

I’d love to see this method compared to the others here. I enjoy how thoroughly you assess these withdrawal methods and would be interested in your opinion on how this method compares.

There are advantages and disadvantages to this system: Withdrawals never go down. Well, they could go to zero if your 2.7% was the wrong estimate of what the fail-safe is. And the disadvantage is that 2.7% seems awfully low as an initial rate. But if the 2.7% generates enough consumption even in year 1 this could be a nice system!

I agree about positives and negatives. Perhaps there could be an emergency failsafe installed? Something like: if your current spending is over x% of the portfolio, do y. Maybe have over x% for a few years to reduce volatility and have an absolute ceiling of z%? Though I agree, it definitely has the potential to fail.

I agree it’s a low initial rate, but I do see an additional issue. If you’re already getting the most income you’ll receive from other sources, and if 2.7% is initially too low, how will you manage if your other strategies go below 2.7% in a downturn?

It seems that in most of the starting years that after about 5-10 years the 2.7% strategy was matching the income of the “fixed 4%”. If it didn’t do that, it was because you began in a downturn, so the lack of an increase was protective (other adjustable systems would have gone even lower, think GK from the previous post).

I don’t think it does too bad in this 1957-2016 test case. I believe it’s rises from 2.7% to just over 4% in 1966, where it remains until 1996 where it rises to about 6%.

Many of them adjustable systems here go below (!) 2.7% in this test case, which I think is the core issue. If it’s necessary to save the portfolio then I’d understand, but in this case it isn’t. Though such a thing would be difficult to predict.

I may be wrong, but the 2.7% seems to adjust itself upwards well to match the correct drawdown. It seems to be more conservative than even a fixed 3.25% if necessary, but more generous than a fixed 5% if viable.

True. But I still prefer the 3.5% initial or the CAPE-based rule. Remember, if the portfolio really goes up much more than expected you adjust them upwards as well. Either through the CAPE or through some form of Guyton-Klinger method.

I’ve really enjoyed the series, thanks for putting this all together!

I do wonder about the predictive validity of this particular study. It covers a single 50 year period, and may or may not project well into the future. The CAPE rules do seem really promising, but given that CAPE10 explains about 40% of market returns how solid will that be? Dunno. Guess we’ll see, and ultimately being flexible in ones spending and having a cushion seems key…

For myself, I’m unscientifically planning a 3% initial withdrawal rate. Adjusted periodically based on how I’m doing (i.e. not a constant mechanical 3%). And that 3% includes fluff (nice vacations, eating out, etc). And it doesn’t include social security (I’m 50) or a very small pension. Mind you, I could retire now at the 3% rate so it is being padded as I type this…

Thanks! I’m sure I will use a similar rule to yours. It won’t be 100% deterministic and scientific. But for the simulation I had to use something that can be modeled as a formula.

At age 50, a 3% SWR seems pretty conservative. That will last for a long time, especially considering Social Security.

I’m less worried about how representative the 60-year window is. The dynamic rules will never completely run out of money (unless you use some crazy aggressive parameters). For studying how the dynamic rules respond to the market ups and downs it doesn’t really matter what 60-year window you use. Very different from the fixed 4% rule!

I’m missing something really simple; what are “a” and “b” in the approach you described here:

“A rule based on the Shiller CAPE: Calculate the Cyclically-Adjusted Earnings Yield (=1/CAPE) and use this as a proxy for expected equity returns. Then set the withdrawal rate to W = a + b*CAEY with the appropriate parameters for a and b.”

I think I get that a CAPE of ~30 gives you a Cyclically Adjusted Earnings Yield of ~.033, but what am I plugging in to a and b to generate the withdrawal rate (W)?

Thanks!

CAPE=30 would imply a CAEY of 3.33%. So with parameters a=1%, b=0.50 the SWR = 1%+0.5*3.33% = 1%+1.67% = 2.67%.

Sometimes people play a little bit fast and loose with the parameters: a=1 or a=1%. I think I’m guilty of that, too. 🙂 Sorry about the confusion!

Thanks for that. I’m trying to get my head around the mechanics….is there an explanation for what the 1% and .5 represent in the most conservative CAPE-based scenario? Why does the model knock half of the expected yield off, and then add a percent to it?

Yup, there is definitely another post dealing with a CAPE deep-dive coming up at the ERN blog.

My personal theory for the parameter choice a>0 and b<1.0 is this: The expected return of equities is roughly equal to the 1.0*CAEY plus a small intercept. The intercept is a little bit above zero (recall you take 10 years worth of real earnings but earnings grow faster than only inflation).

You want to set the slope to less than 1. That's because if you're under-water with your portfolio you want it grow out of the hole. So, spend only half the expected return. That way you get a mean reversion back to the real starting value.

Cheers!

That’s what I needed, thanks! Really looking forward to the CAPE deep dive.

I love all the research that you have done!!! I have to admit that I hadn’t looked at the safe withdrawal rates in awhile but this definitely is eye opening. I am definitely going to download your pdf and pour through it this weekend. Thanks for sharing!!!

Thanks for stopping by! Yes, withdrawal rates should be on everybody’s mind. Lots of things to write about! Hope you enjoy our working paper!

Cheers!

Great insight and Well thought arguments for your grading criteria and points! This creates a lot of context for us.

For me a conservative cape might be ideal as i intend to keep a form of income post FI. In fact, i might be FI and keep working. Downside is that i need a lot of time before reaching FI

When we meet, icecream and beers are on me!

Thanks ATL! Can’t wait to meet in person later this summer!!!

Cheers,

ERN

For the variable CAPE withdrawal method, what CAPE do you suggest using when the portfolio contains a mixture of international and U.S. equity?

Great question!

For this exercise I used the U.S. CAPE only. If you have non-US stocks and you have access to the non-US CAPE numbers, I would simply calculate the CAEY (=1/CAPE) and take the weighted mean of the CAEY. Example: In the 80% equity portion you have 50% U.S and 30% non-US. Then calculate CAEY = 50/80*USCAEY+30/80*nonUSCAEY.

It’s essential that the weighting happens on the CAEY level not on the CAPE level (difference between arithmetic and harmonic mean).

Hope this helps!!!

Cheers,

ERN

While I agree that it’s better to take the mean on the CAEY level, it will still be 100% accurate only if your geographical distribution matches the price distribution. Remember, that “PE” in CAPE is “price to earnings” and price is different for different chunks of the world economy.

Ok, making some progress here… The problem with CAPE rules like a+bx is that this is usually an exercise in back-fitting past events. So it’s no mystery this looks better than G-K or VPW when backtesting. Would it stay the case in the future isn’t a given at all. Also, there is ZERO evidence that CAPE has a fixed mean to return to (actually plenty of counter evidence). Now your focus on CAPEY and your laments about G-K not giving much of an advice of the initial withdrawal rate (same is true for VPW, it’s just hidden a little more under the hood) should give you the answer… Yes, 1/PE (or derivatives) can be shown as being a decent model for mid-term (real) expected returns, and I am not only speaking of empirical ‘proof’, but something reasoned. In the same way, bond yields are pretty good (albeit nominal) predictors. Just combine the ideas and you’ll get somewhere… 😉

Thanks!

I can live with calibrating the GK rule to a CAPE-based value, but then why not go all the way and use CAPE all the way

Also: using the CAPE would, in no way at all, require the CAPE displaying mean reversion to the same value for 145 years. Quite the opposite, I would be the first to argue that there are different regimes for mean CAEY and today’s economy sustains a lower CAEY (=higher CAPE). I created some charts that show there is mean-reversion to a time-varying mean. Subject of a future post. 🙂

Cheers!

ERN

Sorry, my comment about mean reversion was a reference to many withdrawal methods proposals I’ve heard, but didn’t apply to your write-up, you’re right. For whatever reason, you focused on some (perceived) negatives of G-K, and didn’t acknowledge the good stuff (it is simple, adaptive, and it does provide a nearly perfect protection against short-term portfolio volatility while not damaging the long term – and no, there is NO need to react quickly to point drops). A simple CAPE equation remains too volatile, 2009 being proof, those earnings can go truly berserk at times. There is a need to be a tad more subtle to combine the strengths of the various methods. And by the way, I didn’t word my previous suggestion precisely enough, I didn’t mean to set the G-K IWR (or the VPW ‘rate’) once and forget it. I meant to adjust it every year based on current expected returns. Give it a try…

I like the performance of the CAPE rules during 2008/9 the best. See the chart. Remember, just because the CAEY moves a lot doesn’t mean that the withdrawal amount moves a lot.

Withdrawal = Portfolio Value * CAEY (or some variation).

CAEY moves up a lot, portfolio value moves down a lot in 2009. Net effect is muted. All the other withdrawal rules get hammered in 2009, see the chart.

This is actually my main complaint with Guyton-Klinger. They bark at the wrong tree. The WR isn’t the problem. We don’t need a guardrail around it. CAPE-based rules work perfectly well to give you smooth withdrawal paths (because the 10-year rolling earnings are so smooth), despite varying withdrawal rate paths.

As a side note, the proper way to parametrize VPW to extend the portfolio past the planned retirement period isn’t to cap withdrawals, it’s simply to use retirement period + 10 years (or whatever ‘grace period’ of your choosing) as the duration provided to the algorithm. Which really should be common sense anyway, a retiree on his last few ‘planned’ years may want to plan for a slightly longer expected lifetime!

Good idea. Why didn’t I think of that? Qualitatively, he same results, though. VPW is essentially just as volatility as the constant % rule.

Yes, that’s true. The VPW author essentially believes that if one seeks less volatility, one should adopt a more bonds-heavy portfolio. This never made any sense to me to very directly link withdrawal volatility with portfolio volatility. What I suggested to you in the previous comment mostly addresses the issue of both short-term volatility and long-term volatility, which are two very different things. This isn’t perfect, but much, much better.

Agree! With more bonds you get less short-term vol but more risk of running out of money in the long-term.

Cheers!

Doesn’t the VPW protect you from running out of money? Granted, it may do so by dictating a lower withdrawal rate (as bonds may not track unexpected inflation). Would be interesting to see how the methods hold up against more conservative portfolios

Yes. You will never get to $0.00. But you could still slowly shrink your portfolio and lose purchasing power. Normally though, the VPW rates are picked so that the VPW withdrawal rates are in line with the expected portfolio returns and a significant erosion of purchasing power should not persist. You could suffer some short-term losses (look at the volatility in the table above!!!), but longer-term you should always recover your initial purchasing power.

Cheers!

Very interesting.

I have a couple of questions on the practicalities of maintaining a CAPE based dynamic SWR.

1. If we want to utilise international stocks there doesn’t seem to be a real time CAPE metric available like the one that exists on multiple.com. Is there one?

2. You have mentioned several times that you intend to withdraw funds monthly and hence make the percentage withdrawal calculation monthly. I assume that means you are comfortable doing so with a CPI that is 3 months old as that is the publication lag? And further, that combining current CAPE with 3 month old CPI is also OK.

Maybe these are trivial issues but I’m always thinking about how to actually implement these sorts of SWR methodologies.

Very good questions.

For international comparisons, I use this link: http://www.starcapital.de/research/stockmarketvaluation

The CPI is no more than 1 month old. The CPI for the previous month comes out around the middle of the month (e.g., Oct 13 for the September CPI). Shiller on his page simply extrapolates the one additional month of CPI if the most recent number is not available.

More worrisome is the fact that Shiller uses up to 6-months outdated earnings numbers. See my post:

https://earlyretirementnow.com/2017/03/22/cape-fear/ It details how to properly fill in more recent earnings numbers using earnings estimates from the index provider S&P Dow Jones: http://us.spindices.com/indices/equity/sp-500

Dear ERN,

That about adding joint life probability factor to CAPE based rule ?

I mean the withdrawal rate will be something like SWR=(1/(years to death))*factor*(CAPE formula)

It will allow to raise withdrawal in case of serious disease , death of the partner or some other unexpected but reasonable circumstances

Hi Mike! Great point! The SWR in the CAPE-rule is calibrated to preserve your wealth. One could make an adjustment through the PMT function. So, calculate the CAPESWR and then plug into this formula:

PMT(CAPESWR,years,-1,0,1)