I thought I had written everything I wanted to write about emergency funds. Especially why I don’t like them! For example:

- Our emergency fund is exactly $0.00

- Top 10 reasons for having an emergency fund – debunked (Part 1)

- Top 10 reasons for having an emergency fund – debunked (Part 2)

But this topic just keeps coming back. Most recently in the ChooseFI podcast episode 66 and the discussion that ensued afterward. One unresolved issue: the pros and cons of investing the emergency fund in the stock market. As I’ve mentioned before, I am not against having an emergency fund. Quite the contrary, if you’re on your path to Financial Independence (FI) you strive to accumulate 25 years (!) (or better 30+ years) of expenses – much more than the 3-6 or even 8 months of living expenses normally recommended to keep in the emergency fund. In other words, I view our entire portfolio as one giant emergency fund invested in productive assets (mostly equity index funds) and I don’t see the need for keeping a separate bucket of money in low-risk assets. One could view this as having an emergency fund that’s invested in stocks! 100%! How crazy and/or how irresponsible is that? That’s the topic for today’s post. Let’s look at the numbers and quantify the tradeoffs…

Pros and cons of investing the Emergency Fund

My critics would normally object “you must invest the emergency fund in something risk-free (or at least significantly less risky than stocks) because the emergency could occur when the stock market is down!” My response is: So what!? I never claimed that investing the emergency fund (EF) in stocks will always outperform. On average it will and I am willing to take risk of some moderate downside. But I still like to know a) how large is that downside and b) how likely is the downside and c) how does that compare to the upside? Then weigh the pros and cons.

Simulation exercise

Let’s look at how investing the emergency fund in different portfolios would have performed. Here are the assumptions for my little numerical example:

- Invest one dollar every month for 36 months to build up an emergency fund.

- The contribution occurs at the beginning of each month.

- Of course, all contributions are adjusted by CPI inflation, to make meaningful comparisons across time.

- At the end of the 36th month, we must fund an expense of $36, which is also in real inflation-adjusted dollars.

- I consider 4 different portfolios:

- 100% stocks (S&P500 total return index)

- 100% bonds (10-year Treasury bonds)

- 60/40, i.e., 60% stocks, 40% bonds

- 100% cash: money-market-like returns calculated as 3-month T-bill returns

- I use monthly returns from January 1871 to December 2017, just like in the Safe Withdrawal Rate Series.

I kept this example intentionally generic. For example, someone could view this as saving $100 a month for 36 months to hedge against a $3,600 home repair. Simply multiply all simulation results by 100. Or a $7,200 repair? Simply multiply everything by 200. Or multiply everything by 500 if you’re saving $500 a month to hedge against a job loss, i.e., the emergency expense would be $18,000, worth 6 months of expenses at $3,000 each. I also wanted to keep the investment horizon short enough to ensure that there will be plenty of examples where the equities will significantly underperform the money market account. But also long enough to account for the fact that an emergency fund is substantial enough that you can’t just be put together in a few months.

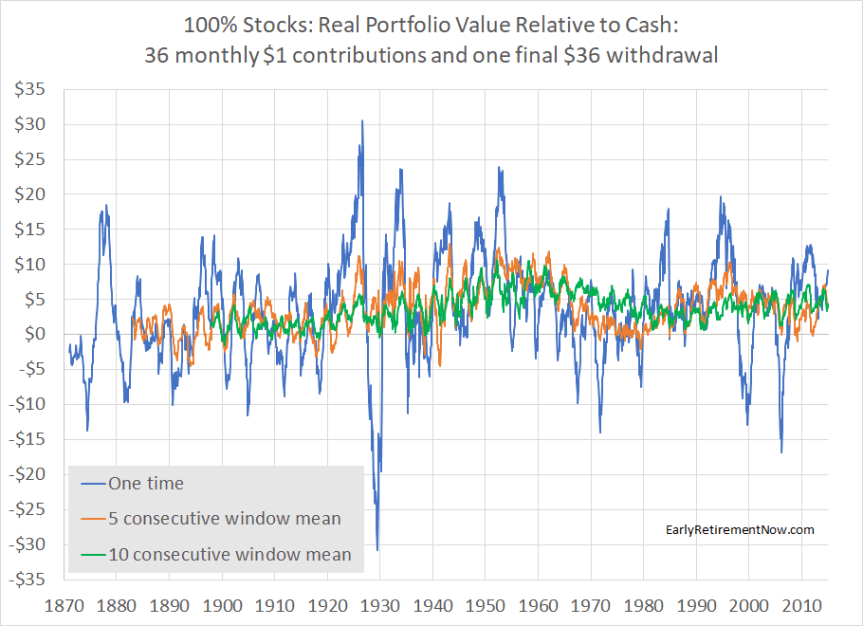

In any case, let’s look at the portfolio value for different cohorts after withdrawing the $36 emergency expense, see plot below. Thus, a value of, say, $3.50 in that plot (and all calculations below) would mean that the emergency fund would have grown to $39.50, so we’d have $3.50 left over after withdrawing the money for the emergency. Likewise, a value of -$5.00 would mean there was a shortfall of $5.00 because the portfolio only grew to $31.00, insufficient to fund the $36 emergency expense. Some observations:

- The equity investment creates a lot of uncertainty about whether you can actually fund the desired expense. Your shortfall could be as bad as $23. But you could also end up with over $30 more than you needed!

- Investing the EF in cash (earning money market interest) creates much less volatility. But make no mistake! In real, inflation-adjusted terms, even the ostensibly “safe” EF invested in the money market has occasionally been eroded by inflation to generate a shortfall of $5 and more!

We can also plot the whole chart as the difference between the risky portfolios and the “safe” EF invested in cash, see below. This difference is what I’m mostly interested in because I like to get a sense of how frequently and how severely I underperform the safe EF if ignore the advice from the (so-called) financial experts and I invest in equities instead. Now the spike on the downside during the Great Depression becomes even more pronounced. But the spikes for the bear markets in the 2000s didn’t change much, mainly because money market interest rates were so close to zero in real terms:

And finally, I can also provide a table with some stats of the above time series. And again I report numbers for both the absolute values of the four different portfolios (left) as well as the final portfolio values over and above the Cash EF (right). Some more observations:

- Stocks outperform the cash-only EF by about $3.54 of monthly investment. That’s $354 for a $3,600 emergency fund!

- But due to the much higher volatility, there is a significant probability (31%) of underperforming the money market fund!

- What is a serial correlation? Glad you ask, I will get to that in a just a few paragraphs. Hold that thought and stay tuned!!!

- I also include in the table the percentile distribution of the different returns. How concerned would I have to be about investing the EF in stocks? Sure, there were cases where the stock investment underperformed. As a cautious investor, I realize that the $3,600 EF target might fall short by between $795 and $1,555 in 5% and 1% of the cohorts. But that’s not a life-altering loss. Neither in absolute terms nor compared to the median advantage of $351.

Summary so far: I don’t think people can make a clear and convincing case that you should never invest an EF in stocks. It all boils down to risk aversion: I am not that risk-averse, thus, I should be comfortable keeping my EF in risky assets. Others have different risk preferences and might want to keep their fund in cash. Though, I can already hear one objection:

“Objection, objection, Big Ern! In your Safe Withdrawal Series (see Part 1 here), you always make the case that we should look at the scary tail events. Why not here? Aren’t you logically inconsistent?”

I am so glad you asked! The two reasons why I use a different kind of risk management in my Safe Withdrawal Rate Series are:

1) Magnitude: Running out of money in retirement is a catastrophic and life-altering event. Running short a few hundred dollars in the EF example is a nuisance. In the former exercise, I like to be much more cautious and study the extreme tail events. In the latter exercise, I am much more willing to trade off a small probability of a small loss with a small probability of a moderate gain.

2) Sample Size: The safe withdrawal exercise is a one-shot game. I will retire in June 2018, which makes me a member of one and only one retirement cohort in my simulation exercise. I can’t split myself into ten little Big Erns that retire at ten different times and are then able to shift money from, say, cohorts 3 to 10 who had better luck with their retirement timing to cohorts 1 to 2 who might risk running out of money. I can’t perform any diversification between ten little Big Ern cohorts! It’s a very different story for the emergency fund. Over my lifetime, I have faced multiple spending shocks. Some occurred when the market was up, some occurred when the market was down. The timing of those shocks and the market level at those times are mostly uncorrelated. So, I get a lot less concerned about tail events and look a lot more at means and medians because, in the end, I will average over multiple different events.

This last point got me thinking: What’s the distribution of not one single 36-month EF window but multiple consecutive windows in this simple numerical example? Think of this as saving for not just one single emergency but the five to ten emergencies we may face over our lifetime.

Think of this as diversification, but not within the portfolio but across different 36-month windows. And here’s where the serial correlation comes in, remember the item in the return stats table above? That is the correlation between two excess returns over cash of two (non-overlapping) consecutive 36-month windows. For stocks, we had a correlation of -0.10, so not only are the returns not correlated, but they are even very slightly negatively correlated.

Let’s look at the chart below: Smoothing out the very crazy volatile blue line (EF invested in 100% stocks excess return over cash) over 5 and 10 consecutive (non-overlapping) windows, you do a pretty good job of averaging out the large spikes. It looks like the excess return of the 100% equity EF is now much more consistently positive!

And here’s the table of not just the stock but also bond and 60/40 portfolios (relative to the cash EF), see below:

- Averaging over 5 and especially 10 consecutive windows it becomes more and more likely that we outperform the cash/money market EF! Over ten consecutive windows there was only a 2.4% chance of falling behind when investing in equities! And even then, the shortfall is tiny! That’s not surprising! You average over 10 individual EF calculations, they are not just uncorrelated but even very slightly negatively correlated, so some of the bad luck when withdrawing from the EF at the stock market bottom is bound to average out over time.

- It’s really intriguing that a portfolio with lower short-term risk, i.e., bonds or 60/40 performs significantly worse than the 100% equity portfolio. Bonds had a 43.7% chance of performing worse than the cash EF in the one-shot version. In the 5 and 10 consecutive windows that probability actually goes up (!!!) which shows again that an ostensibly low-risk investment over short horizons creates a higher risk of falling short of expectations over longer horizons! See a post in a similar vein from a long time ago: “When bonds are riskier than stocks“

And I won’t buy extended warranties either!

Until I put this post together I always thought that the preference for a cash-only emergency fund can be rationalized with risk-aversion. But that’s a very myopic way of looking at the problem. It reminds me a bit of the issue of whether or not to buy an overpriced extended warranty on cars, appliances, electronics items, etc. Looking at the one problem in isolation, a very risk-averse person could rationalize buying the warranty. But it would be so much cheaper to self-insure, i.e., save the money one would spend on each warranty and pay for the replacement or repair of the 1-2 items that break down eventually. So, in that sense, the warning “what if you need the emergency fund when stocks are down?” reminds me a lot of the sales pitch for the extended warranty: “what if your TV breaks down 3 days after the manufacturer’s warranty expires?” My reply: I don’t care! I take this small gamble because I will average this over at least 5-10 such risks over my lifetime and I like to pocket the positive expected value of the ostensibly riskier option!

Thanks for stopping by today! Please leave your feedback below!

Picture Credit: Pixabay.com

I agree with this during the accumulation phase. One aspect you haven’t looked at for the FIRE community is building cash so your taxable income stays below the cut off for ACA subsidies. I have calculated I will save over 100 grand in after tax premiums by having about 80,000$ in cash for the 5 years before I’m eligible for Medicare. I never thought I’d become obsessed with minimizing my income but that about sums up how I think of these things these days.

True, I was writing this mostly from the perspective of a person accumulating assets. I can see how derisking the portfolio around the retirement date and then using an equity glidepath back into equities is a pretty good idea (see SWR series parts 19-20).

Maybe now that you are almost FIREd you should start writing some posts from that point of view! This particular issue is one I stumbled on in my pre retirement budgeting. Had I not done a detailed budget I would have missed it. Most blogs are written from the point of view of the accumulation phase and don’t touch on the issue of income minimization. One of the results of my discovering this is that I am going to continue working as a contractor 30-40 days a year (60-80k then in income) and eliminate all that by above the line deductions. That way I will replace the cash spent with stocks in tax advantaged accounts (solo 401k, employer and employee contributions, IRA, HSA) keeping my taxable income below the threshold for subsidies. Essentially I won’t be spending anything from my portfolio other than dividends and a small amount from a 457b and the cash spent will ‘turn into’ stocks. Had I realized this after retiring the necessary steps to work in my profession and get credentialed would have been very difficult and taken months.

If you have additional cash flow there is no need to worry much about having cash sitting around to cover bills! Even more reason to go 100% equities. Or maybe 80% stocks, 20% bonds.

Another possibility would be to consider a 50% crash in stocks, such as 2008 for example, and then invest 2x the emergency fund. Thus even in a severe bear market, you will have 50% of the invested money (that will cover your expenses).

Well, on the path to FI you’re accumulating not just 2x the EF but 50-60x (i.e., 25-30 years of expenses compared to 6 months in the EF).

Yes of course, but if you have 60x EF, even if you have to sustain a bear market of 50% (like 2008 did to S&P500), you would still have 30x your EF. Plenty of money to hold on. On the positive side, you will be exposed to an expected return of stocks far better than the cash (based on the 6,8% historical return of stocks vs 0,5% for cash) – http://monevator.com/us-historical-asset-class-returns/

Well said! The returns after the trough are normally better than average, hence, the negative serial correlation in the stock portfolio relative to cash EF!

Thanks for quantifying this, Unsurprisingly we are on the same page 🙂

We definitely are! Thanks for stopping by! 🙂

I can read your emergency fund articles all day. When you have a large investment account to fall back on, keeping a huge cash emergency fund site seems like a mistake. Now I need to get over my own fears and actually pull the trigger. This may be the one area where my opinion (in line with yours) and my actions are not the same.

I won’t put words in ERNs mouth, but I bet he would argue (I would, anyway) that when you don’t have a large portfolio to fall back on (i.e a low net worth individual), there is even MORE of an argument for eschewing a cash EF. The farther you are from your goal, the less you can afford to forego growth.

I disagree a bit Trent. Let me provide a brief example.

The biggest risk in my mind is a 50% market drop while at the same time losing one’s income. Job’s do tend to disappear when the market goes down after all.

Person A) Has $200K in a taxable brokerage account $50K in living expenses. After the decline, he would have $100K left. Leaving him two years of living the current lifestyle to get a new job before going broke.

Person B) Has $25K in a taxable brokerage account and the same $50K in living expenses. After the decline, he would have $12.5K left. Leaving him three months of living the current lifestyle to get a new job before going broke.

I think person A could comfortably take ERN’s advice and roll the dice to earn higher returns. Even in a very bad scenario with a 50% market decline and losing a job, person A should be able to bounce back.

If I was person B and don’t have an option to live for free (with friends/family) as a safety net, I’d keep the emergency fund in cash. I’d never want to risk only having a three-month buffer before going broke. I say this knowing that investing is more likely to put me in a better position than keeping the cash in a savings account.

Jason, I certainly see this argument; I guess my reply would be: an emergency fund is basically a form of insurance, and as an insurance instrument, it is horrible. As I commented lower down, it only pays out once, and at a low ceiling; in the worst case scenario, it would only given an extra buffer for a relatively short period of time. The odds of all these things lining up for it to be optimal is low; in the meantime, real growth opportunity is lost. The average unemployment period is 3 months. I mean, in the example you laid out, it’s just as likely you use up your EF and STILL run out of net. That’s a double whammy, given you’ve lost the opportunity cost.

Thanks for the reply.

Very well put! I mentioned that briefly in this post: https://earlyretirementnow.com/2016/09/07/debunking-emergency-funds-part1/

See item 2. 🙂

It takes some guts to pull the trigger and forego the money market account. Maybe use Dollar Cost Averaging? And tax loss harvesting if the market goes down?

I had a question about what to do with my EF, but realized you’ve already answered it! https://earlyretirementnow.com/2017/05/10/lump-sum-vs-dollar-cost-averaging/

Ha! Great idea! If you already have a cash EF and don’t like to invest the lump-sum, absolutely, use DCA! 🙂

Qualified and quantified articles, well done once again BigERN. Added to the decision to reduce the cash account held for costs of daily living only, versus covering an emergency fund as well. The emergency fund now sits across 3 large cap stocks and emergencies are covered by a 30 day free loan on a credit card – just to be paid in full from the stock market. If the tail on a market down turn whips me to a loss, well then, the emergency just became a little more important to solve.

Prior Proper Planning Prevents Poor Performance, Period! Or some version of the Ps….

Nice summary with the 7P! And I agree that the EF invested in stocks makes it a little bit harder to abuse the EF for an emergency HD-TV!

You only look at a 60/40 split. And I am guessing pulling expenses from all parts of your pot in proportion to the size of each. What about a scenario where there is a smaller low volatility pot which would be used to drawdown expenses from during a stock market downturn, leaving teh higher volatility parts alone to recoever. So assuming your portfolio was designed to have a maximum downturn of 6 years. Then you would need a low volatility pot for expenses x 6 years approx 15-20% of the total pot. You could ofcourse scale this back to less than 6 years depending upon your appetite for risk?

This exercise is independent of the rest of the portfolio. I just wondered how you’d do accumulating the 36x monthly savings. And then take the entire sum out all at once, so the issue of what to withdraw when doesn’t really apply here.

I love your analogy to extended warranties. It makes it seems sort of sleazy to put the EF in cash!

Also, Dave’s first comment is worth a look. We also keep our income low for ACA subsidies, but are able to do that via real estate and a small pension. Originally we thought we would need a bucket of cash for the years prior to age 59.5. We have not needed it. So many times, it’s fear that convinces us to put something in cash, but we don’t give the same fear to the lost opportunity. Thanks for another great analysis showing counter-intuitive results. Love it!

Thanks!

One can keep taxable income low by withdrawing from taxable accounts with high cost basis first. But the “bond tent” approach, i.e., raising bond/cash holdings before retirement and then walking them down to shift to equities in retirement is worth a look for hedging against sequence risk! 🙂

Can you expand on what a “window” is in the 5- 10-window part? Or is that found in your other articles?

The 5-window calculation would be to save $1 for 180 months, withdraw $36 after months 36, 72, 108, 144, and 180. Then look at the excess/shortfall in months 36, 72, 108, 144, 180.

Yeah, I’m on the same page with this, I don’t keep a cash emergency fund – when you earn enough to easily cover 99.9% of expenses that ever come up, it doesn’t make sense. A big emergency = I invest less that month.

Exactly my thinking during our accumulation phase! Use the credit card float and future savings to deal with emergencies!!! 🙂

what if you don’t have a credit card or hloc?

I never did a poll but I assume almost 100% of my readers have a credit card.

Well, maybe yes for your direct readers, but your blogposts are translated and published/re-told in other countries where lots of people are not as privileged. And for them your pieces of advice sound moronic. Please note that it’s not what I personally think, I find your blog interesting and thought-provoking, but I thought you might be interested to learn this info.

Great stuff. And this before accounting for the fact that a cash EF is like an insurance policy that is capped with a low ceiling, and only pays once. That’s a crappy policy, and for that you have to forego growth on the funds basically forever. No thanks.

My question: What would you do with funds to pay for large predicted (i.e. non-emergency) expenses. For example, I pay hefty quarterly estimated tax payments via credit card, which gives me an extra 6 weeks (on top of the buildup of cash over the quarter) of runway before I have to pay it off. What would big ERN do with the cash in that scenario?

Thanks!

Technically, the same logic should extend to other non-EF applications, i.e., saving for estimated tax payments, etc. Provided that these are repeated expenses that you have regularly and where you average out and time-diversify over many occasions. Maybe not for a once-in-a-lifetime large expense, like a house down payment.

I also just used the credit card for federal tax bill and estimated tax. Get 3.3% cash rewards (less 1.87% fees) and the float!!!

Wow, where do you get 3.3% cash rewards?

Old grandfathered Priceline Visa card. You get 2 points per dollar spent. But you can redeem 2-for-3 points for travel expenses (i.e., 3% cashback equivalent) and for certain expenses (Priceline name your own price) you get another 10% bonus when you redeem points, which makes this a 3.333333% effective cash-back rate.

It’s our daily go-to card for everything! 🙂

Is it safe to say that often overlooked is the psychological benefit of having a fully funded emergency fund in cold hard cash? I know many people who make more sound and responsible financial choices knowing they have a stash of cash put away in a mmkt or hysa earning 1.5%-2%. Obviously losing to inflation, but they don’t care, because they know the value of those accounts will never go down. It isn’t a big portion of their portfolio, but it always is a steady one.

This argument really boils down to psychology. How comfortable are you with volatility? That ultimately answers where you keep your “emergency fund” and how much you keep in there.

If psychology refers to making suboptimal decisions because they feel better, I can refer to an old post of mine: https://earlyretirementnow.com/2017/06/14/good-advice-vs-feel-good-advice/

It’s our job as bloggers to educate people about their psychological biases. We shouldn’t reinforce behavioral biases. Wouldn’t it be great if more people did the mathematically right thing and also felt good and confident about it?

I’m afraid this articles is also based on a bias of yours – survivorship bias. You based your calculations on sp500, while Ben Felix from Common Sense Investing YouTube channel showed that it’s not entirely correct – we didn’t know in the past that sp500 would survive that long and we should also see how we would do with investing in other country indices.

With that said, I still like your articles, at least they are very argumented and thought-provoking.

There is no survivorship bias in the S&P500 TR index for the live coverage. Companies come into the index and fall out of the index, and the losers very well impact the index o the way down (e.g. Enron, Lehman, etc.). Anybody who claims there’s survivorship bias in the S&P doesn’t have a clue what they are talking about.

That also extends to the Composite index prior to the S&P 500.

There is a potential for survivorship bias in the very early period when the index needed to be recreated/extended based on historical data. But I trust the economic historians that did this exercise to know what they were doing.

PS: I finally googled “Ben Felix” and “survivorship bias” and he apparently talks about the country survivorship bias, i.e., the fact that the USA just got lucky that we were never invaded and/o destroyed and/or defeated in WW2 like Netherlands, Belgium, France, Poland, Germany. etc. That narrative is idiotic because the USA will never suffer the same fate.

I’m not sure I understand why you say that Ben Felix, a very respected professional, has an idiotic narrative. To me it sounds very reasonable, that the US did get very lucky for a number of reasons, and it’s not obvious that it will always last this way.

The US will not be invaded like much of Europe.

End of discussion for me.

If you like Ben’s story more, then good luck to you.

I’m not for anyone’s story, I’m for the truth. You seemed to be for the truth as well, because you debunked lots of your fellow financial advisors with math at hand. However, right now, when someones shows you a bias in your own calculations, you are not ready to admit it. So sorry to see that. But anyways, no hard feelings from me, good luck to you as well.

Admittedly this may be more psychological than financial reality, but I keep a lot of cash in a money market fund, checking account, and I have a HELOC. I would hate to have to sell stocks after a 70% market crash just to cover living expense. Paranoid? Maybe. Possible, yes.

And I would have hated to watch the MM account go nowhere when equities grew by 30+% in 2013. Hence, the consideration about time-diversification and smoothing out over multiple different EF accumulation and spending periods.

I think psychology is the determinant here. If you had a 200k portfolio that dropped by 50 percent liquidity is still not an issue.

But if that drop drives you to sell everything and sit out then you needed the ef fund.

This is the first time I ever hear that argument. Why would someone who has $200k in equities suddenly sell all holdings because they held $3,600 in an emergency fund in stocks? And why would that same person not get cold feet if they had $3,600 in an EF in a money market account?

I wish I could say it was a contraption of my own mind. But I witnessed more then 1 person do so in 2008. Real people that are close family friends no less.

One thing to add, 3500 to you and me is peanuts. In a world where the avg American can’t afford 400 dollars for an emergency it can be a lot.

Oh, no! I think they would have been better off doing 60/40 in their retirement savings (even though I find that too conservative).

As I said on you older thread, I think we still have a problem with defining a true “emergency”. I don’t think the emergency is created by an additional 36, 360,3,600, or 36,000 dollars of unplanned expenses. These are variances in your actual expenses compared to forecast. To someone with a lot of assets and a good independent income from their assets, I think these are, in the macro sense, blips on the radar. Thus, holding the funds to cover them in cash because they are “emergencies”, just seems to me a failure to define the problem correctly. I wouldn’t hold money in cash on the possibility that my annual retirement expenses might be 5K more than I am planning/hoping.

ERN, in your net worth update you showed 7-8% of your holdings in cash/cash equivalents. If you take the macro view of your portfolio as one portfolio, doesn’t this cut against your argument some? In other words, you do display some risk aversion or some prioritization of the benefits of cash over stocks. I don’t know if you characterize this differently than how someone would describe holding a cash EF, but it feels a bit of a misnomer to say you don’t have a “cash EF” when you do hold 7-8% cash.

I think we’re on the same page with the EF.

I have to keep a certain % of cash as margin for options trading. Currently about 20%. But I run the options strategy with a little bit more than 2x leverage so the fact that I have some “useless” cash lying around doesn’t create the same opportunity cost as in the scenario created by Ramsey/Orman where folks forego the equity beta by trying to accumulate a money market fund before any productive assets.

I hadn’t thought about some of your cash being tied to the options strategy. Makes sense.

Thanks! 🙂

Great article and analysis. This has me thinking a lot about my current situation and cash on hand. One thing that comes to my mind though is the difference between an “emergency fund” and an “opportunity fund”. For me, having a somewhat significant amount of money available in a highly liquid account is more about being posed to take advantage of market downturns or other opportunities that might come along, rather than emergencies. Maybe it is splitting hairs?

Still – something I’ll be thinking about more in the next few days. Thanks for this thoughtful and well articulated post.

I think you’re making the Warren Buffett argument: Keep cash to buy distressed businesses during the next recession. A very different approach to Dave Ramsey and Suze Orman. But if you really have the guts to do that all the power to you. But a warning: I know people who had cash for years and missed out on the bull run. When the market had the desired pullback in early 2016 (S&P dropped to just above 1800), they still didn’t buy stocks. They were way too back then…

Thanks for your timely input on Emergency funds. You mention somewhere that your savings rate is 60% – I’d really like to know how you calculate it. Some use Net Income, some Gross, some net (but account for tax advantaged savings) – do you have a preference? A one line formula would be perfect.

I wrote a post on that:

https://earlyretirementnow.com/2017/04/05/savings-rate/

I’d prefer methods 3 or 4 in the post.

This is so much like the debt snowball, debt avalanche debate. One wins on behavior and the other one on math. This audience is math leaning so would agree with you but for many others not investing the EF will make them feel much better because there is no timing risk.

Math rules, steveark, math rules! I can only lay out the arguments here. People will have to make the investment decisions themselves. 🙂

Big ERN,

Good stuff again today. When I read the title of today’s post, I was a bit surprised as I thought you had already put this EF silliness to bed months ago. However, once again the ERN delivers!

On a separate but related note, I finally overcame OMY syndrome and submitted my resignation. A good portion of the credit for the cure to my severe OMY is all of your freakin’ awesome blog posts. Yep, another person FIRE’d that lays part of the credit at your feet. Less than a month to go! Danke schön.

Haha, as you said, I also thought that this topic was done. But it comes back from the dead with great regularity! Next time I have to invoke some zombie movie references!

And great to hear about your FIRE decision! That’s the best news all day today! Congrats and best of luck!

One aspect to consider – in one article you pointed out that retirees don’t retire across an even distribution of years but rather when the market is high and you (in genious fashion) calculated RMDs with cohorts spaced accordingly. Since a common reason for an emergency fund is job loss, and job loss would seem to correlate to market crashes, wouldn’t it be interesting to do a similar study where instead of evenly spacing the timing of needs for an emergency fund, the needs were closer grouped to market crashes or job losses? This would be a functional approach to analyze the situation as purposed for job loss. What do you think?

Good point. I haven’t done that yet. But I did point out that in my other post that job losses (as measured by unemployment claims) occur in recessions with only 17% probability. Slightly higher than the unconditional recession probability of 13%, but not hugely more likely.

Also, the other purposes for the EF: car repairs, home repairs, etc. don’t correlate with the business cycle.

Terrific post! I have to admit I am usually on the other side of this argument for young people with low incomes – having a cash position often gives the a psychological springboard into equity “risk” that is real, although not mathematically optimal.

I am curious about long term accumulation for a known expense (college savings). We are fortunate enough that I could “self-insure” against market risk so I kept all the kids’ college funds in equities up until needed (as opposed to the common advice to move to less volatile funds in the XX years before needed). I thought that since our three kids’ college years were spread over 10 calendar years that I was better off with “pseudo DCA” of my tuition payments over that time. It worked great so far (8years in). Was I just lucky?

Again, it depends on how big the expense is and how flexible you are. If not having enough money would mean your kid has to drop out of college, then maybe insure against an equity market drop with a glidepath to a higher bond share right around the time you need the money. I still plan to keep all the college savings in equities and if there’s a shortfall then, sorry Junior, you’ll have to get a loan! 🙂

Man, you have really whipped people into a frenzy on this topic! I had no idea this would be such a hot button issue.

I wrote an article recently on short term investing and looked at the optimal strategy to meet an obligation of $10k in three years time. Great minds coincidentally think alike on the same investment horizon of three years!

https://www.actuaryonfire.com/how-should-you-invest-short-term/

I think we essentially did the same analysis, but coming at it from different angles.

I found the same results as you, but I put more emphasis on the constraint that the investor needed 95% certainty to meet the goal after three years with no recourse to additional funds. If you impose that constraint then cash seemed optimal to me.

I think you are saying the same thing; if you have no tolerance to underperform cash over three years then you better invest in cash! But if you have some risk tolerance then other investment strategies might be more optimal.

Ciao!

Thanks AoF! Nice link! And I’m glad we found similar results! And I concede that the larger the expense and the less flexibility you have to fund this with extra savings and to diversify this across time the more likely you’ll have to hold cash!

Cheers!

Thank you for this link! I’ve been looking for some data-driven guidance on what to do with short-term savings (like replacing our car) vs. savings for unscheduled but inevitable expenses (major home maintenance) vs. true emergency savings (like a perfect storm of job loss, medical bills, etc.). Between the ERN post and your short-term savings post, I feel like I have a strategy.

What percent real return would cash have to provide to be better than stocks?

Of course putting your cash at 1.6% rate now is a loser proposition. However, is it still a loser proposition to put some in 5% account? What about 3% account?

Historically, there have been times when you got 2+% real for cash. Average equity real return almost 7%. I think if the Federal Reserve goes over-board with rate hikes (I’m sure it won’t), and we end up with 5% yields (nominal) in money market accounts and we all suspect the next recession is around the corner, then sign me up: I’d keep a significant chuck in cash at that time.

But in today’s environment, I’d still take my chance with equities, even if I can get a 3% promotion on a CD/MM somewhere. 🙂

very risky, you must havd good stock picking strategy

No. Index funds do just OK. All calculations are done with S&P500 index returns.

For Canadian readers landing here; I would recommend you keep your emergency savings in cash in a HISA. It’s pretty easy/painless to get set up for 2-2.3% interest rates in online-only banks (tangerine, motive, eq bank) that are CDIC insured up to 100k with no fees and instant access. No need to hop around for promotions. You’ll probably still win out in equities but there is little downside risk here. The current Covid-19 situation shows why you probably don’t want your emergency savings in equities. At a time when millions are suddenly out of work, the stock market is down a huge amount and now you suddenly need that money.

Nice! It’s still quite low and the opportunity cost of the lost expected equity return is substantial, but at least it’s better than the sub-1% rates you see in most other places!

Thanks for sharing!

Hi Ern, sorry, I’m late to the party, but hope you will still check my comments 🙂 First of all, thanks for your education materials, they are really interesting.

Regarding the EF, I never see you including infrastructure risks in the model. For example, when the current Ukraine-Russia war broke out, governments shut down the exchanges and stopped currency withdrawals out of the country. If one has their EF 100% in equity, where would they be? My friend had some $ in cash bills, and that was the only thing that allowed him to flee the country before the borders were closed.

Also, how come you never were on rational reminder podcast by Ben Felix? I’d love you visit it, I think you might have interesting discussions.

thanks again!

I hear ya. I live in a country where I’m spoiled with a safety net of financial infrastructure. In the USA we also don’t expect to be invaded by a nasty neighbor anytime soon, though we should watch that Trudeau character really carefully.

Either way, as a result of an invasion, all hell will break lose and the accessibility of equity mutual funds might be just as bad as that of your money market fund. So, even that issue wouldn’t entice me to move from equities to short-term fixed income.

I don’t invite myself on podcasts. Either they invite me, or they ignore my work.

Thanks for your reply! I’m not sure I fully agree with you here, but that’s fine. Let me rather ask the question some other way. In your real life simulations, do you completely ignore the infrastructure risks (not like a war, but simper ones, like your broker goes down and your government stops paying the insurance, or something like this) or do you do anything to mitigate/prevent them?

Thanks!

Broker going under is not an issue because the broker assets and yours are separated.

Government poses a risk. For this reason I suggest applying a haircut to your expected benefits payments.

And when I thought I knew everything, I heard this idea from the Choose FI podcast. I’ve had a pretty good size EF for the past 5 years I’ve been an adult and have been throwing in $500 a month for “sinking funds” for house repairs, car repairs, etc. but I have still ended up just using cashflow since the most expensive thing was replacing my tires and brake pads/rotors. And in the past 5 years since graduating college, I haven’t had one true emergency where I needed the $10k+ sitting in my Ally account earning 4.5%.

Just so I have this right, say I am going on vacation in a few months or there is some other expenditure I would just pause contributing any cash to investments and use that cash? I’m also a little uneasy at the prospect of using HELOC’s especially now that interest rates are higher. Like if I needed to replace my car and didn’t have the cash saved up, you would just use the HELOC and then pause your investments to pay that off ASAP?

With today’s interest rates so high and the path for equities so clouded, I don’t blame folks for building an EF now. But back when this was written, I always thought it was a no-brainer keep the EF in stocks.