August 31, 2020 – Recently, there’s been some discussion in the FIRE community about a controversial post written by Sam, a.k.a. “Financial Samurai,” claiming that in light of the current record-low bond yields, specifically, the sub-1% yield on the 10-year Treasury bond, we now all have to scale back our early retirement safe withdrawal rates to… wait for it… only 0.5%! Of course, I’m one of the more cautious and conservative planners in the FIRE community, see my Safe Withdrawal Rate Series, but even I would not push people to less than 3%, even in light of today’s expensive asset valuations.

So, 0.5% seems a bit crazy low to me. What’s going on here? It’s pretty simple; the 0.5% number relies on several mathematical, financial, and just plain logical flaws. Let’s unpack them all…

1: A fundamental misunderstanding of the Trinity Study

According to Sam, the rationale behind the 0.5% safe withdrawal rate is that back in 1998, when the original Trinity Study was released, the 10-year Treasury bond yield was about 5%, and the recommended SWR was 4%. So, the SWR was exactly 0.8x the bond yield. This prompts Sam to propose the following Fundamental Law of Thermodynamics Personal Finance:

“To make things simple, the new safe withdrawal rate equals the 10-year bond yield X 80%. Let’s call this the Financial Samurai Safe Withdrawal Rate.” Source: Financial Samurai

Currently, the bond yield is at about 0.7%, so if we exactly linearly and proportionately scale the SWR as proposed by Sam, we’d arrive at the roughly 0.5% SWR today.

This line of thinking demonstrates that Sam probably hasn’t read the Trinity Study at all or hasn’t read the study carefully enough to grasp what it actually does fully. Very few people have, so I don’t want to be too harsh on him. You see, the study relies on historical simulations between 1926 and 1995 (further extended to include post-1995 data in follow-up studies). The 4% is in no way tied to one single fixed, set-in-stone 5% bond yield in 1998. The 4% Rule is based on the highest withdrawal rate that would have survived a 30-year window post-1926. In absolutely no way is the 4% Rule tied to the window starting in 1998, for which the researchers didn’t even have the necessary 30 years of return data back then. (and neither do we today!)

Most importantly, during those historical simulations, the 10-year bond rate wasn’t always 5%. Quite the opposite, the 10-year yield ranged from 1.95% at the low in 1941 to over 15% in the 1970s. Also, notice that the original Trinity Study published in 1998 uses data until 1995. Therefore, they only looked at cohorts that started retirement between 1926 and 1965. And during those years, you’d have a range of yields between 1.95% and 4.72%, an average of only 3.02%, and a standard deviation of 0.68%, i.e., much lower than the 5% figure that Sam works with!

So, even if the SWR was intricately tied to the 10-year nominal bond rate – it isn’t, more on that later!!! – then you shouldn’t connect the 4% Trinity Study SWR to the final prevailing interest rate in 1998 but the lowest prevailing interest rate throughout the Trinity Study. In 1941 the bond yield was only 1.95%. The 10-year yield is now about 1.25 percentage points lower than in 1941. If we indeed want to adjust the SWR by 0.8% for every 1.0% in the 10-year nominal Treasury yield – we shouldn’t do that either, more on that later!!! – then you should first link the 4% SWR in the Trinity Study to the 1.95% yield, the lowest ever observed between 1926 and 1998, and then reduce the Trinity Study 4% SWR by 1.25%x0.8=1%. So, you’d end up with a 3% safe withdrawal rate, rather than 0.5%. Quite a big difference!

But even this calculation is seriously flawed, which brings us to the next flaw in Sam’s post.

2: Proposing a withdrawal rate rule without running any calculations or simulations

Let’s plot Sam’s Fundamental Law of Thermodynamics Personal Finance in a scatter plot, with the bond yield on the x-axis and the actual realized simulated SWR on the y-axis (assuming a 60/40 portfolio). I also include the naive 4% Rule, i.e., just a horizontal line at 4%. Please see the chart below. A few observations:

- You see very clearly the rationale and the appeal of the 4% Rule: It’s a nice round number that “hugs” the bottom of the historically realized SWRs. Well, not perfectly; there were about 3% of the cohorts that would just about fail. But it’s close enough.

- The realized SWRs have no particular linear relationship with the prevailing bond yield at the start of retirement, in stark contrast to Sam’s claims. True, when you go from a 5% bond yield to a 15% bond yield, there was indeed something of an upward-sloping relationship (though not linear!). But for low yields (between 2% and 5%) you – shockingly – had a negative(!!!) slope between the two variables! Thus, and in direct contradiction to Sam’s claims, low 10-year yields have not been associated with low withdrawal rates in the past 100 years. The failures of the 4% Rule all occurred when the 10-year yield was between 3.5 and about 6%. Never when the yields were exceptionally low. Quite the opposite: when 10-year yields were at their previous historic lows of around 2%, the eventual realized SWR would have been at around 7%. Had you followed Sam’s Rule and retired with a 1.6% initial withdrawal rate (2%x0.8) you would have vastly underestimated the true SWR. And people who follow this insanely low 0.5% recommendation today will likely do too.

- Sam’s Rule would have failed you a whopping 11% of the time in the 1926-2020 simulation period (asset returns 1926-2020, retirement cohorts 1926-1990). So, the recommended SWR=0.8-times-yield rule would have predicted too high a withdrawal rate in 11% of the cohorts. All of the failures would have occurred when yields were in the 5% to 15% range.

Thus, Sam’s Rule is the worst of all worlds: Way too conservative when yields are low and way too aggressive when yields are high.

The big takeaway is that bond yields are simply not that predictive for retirement success of an equity-centric portfolio. And if you know a little bit of economics and finance it makes sense: Low yields are often associated with accommodative monetary policy and low and stable inflation. And that spurs growth and supports the stock market. Very often, the peak of the stock market occurs after a sharp rise in interest rates when my former employer, the Federal Reserve, goes overboard with (short-term) interest rate hikes and sinks the economy and the stock market! Hence the non-monotone relationship between yields and withdrawal rates!

3: Confounding real and nominal returns

I’ve said this on several occasions before, including the Part 1 of the “How to Lie with Personal Finance” series: we have to distinguish between real vs. nominal numbers, especially when studying horizons of 30 years or more. When people mess up nominal vs. real, my BS alarm flashes red, and Sam’s post is way up there. Tying a nominal interest rate to a safe withdrawal rule that adjusts future withdrawals by inflation is just plain wrong. The right thing to do would be to use real, inflation-adjusted interest rates. Either use nominal bond yields adjusted by inflation expectations or just use the TIPS (Treasury Inflation-Protected Securities) rates directly.

But using bond rates to pin down withdrawal rates makes sense only when you have a portfolio that’s mostly (entirely?) invested in bonds. This brings us to the next point…

4: Safe Withdrawal Rates based on 100% bond portfolios and current real bond yields are still likely greater than 0.5%. If you’re OK with at least partial capital depletion!

I want to give Sam’s approach of tying safe withdrawal rates to bond yields at least one honest try. Let’s assume you indeed retire with a 100% bond portfolio. I don’t know anyone who does this, certainly not in the FIRE community, but out of academic curiosity, let’s give it a try.

First, taking item #3 seriously, we’d look at the real, not the nominal bond yield. The real yields of TIPS are currently around -0.26% for the 30-year (and -0.99% for the 10-year TIPS) as of August 27 (Source: Federal Reserve Table H.15). But even with yields in the -1% to 0% range, you’d still be able to pull off a so-so withdrawal rate. In the chart below, I use the Excel PMT function to calculate the sustainable real withdrawal rate as a function of the real interest rate (x-axis) for different time horizons (30 years and 60 years) and also for different final value targets: 0% (capital depletion), 25%, 50% and 100% (capital preservation). It’s essentially an amortization calculation.

Let’s take a look at the results:

- First of all, if you insist on full real capital preservation, then the safe withdrawal rate calculation becomes trivial: You withdraw exactly the real interest income. And with today’s negative yields it implies that you will never be able to retire on a U.S. Treasury portfolio alone. It’s because even with zero withdrawals, the bond interest income is insufficient to guarantee that the principal keeps up with inflation. Bummer! That’s even direr than Sam’s 0.5% rate!

- But if you’re OK with full depletion or at least partial depletion of your assets you can go much higher than 0.5%: If we use the roughly -0.25% real rate on the 30-year TIPS, you get 3.2%, 2.3% and 1.4% safe withdrawal rates for a 30-year horizon and 0%/25%/50% final asset target, respectively. If you face a -0.25% real return over a 60-year window, you can still withdraw 1.5% p.a. and only slowly deplete your capital over 60 years. Though, I hope that real rates will go positive eventually.

- Also notice that in the late 1990s, TIPS yields were north of 3%. Over a 30-year horizon, you could have easily pulled off a 4% safe withdrawal rate and still have 50% of the capital left after 30 years. Or even a 5% withdrawal rate with capital depletion. Pretty impressive!

So, for a 100% bond portfolios, Sam’s claim that you have to reduce your SWR relative to 1998 is certainly true. But it doesn’t mean you have to go all the way down to 0.5%!

Side note for the finance geeks: The mathematically cleaner way would have been to look at a bond ladder to exactly match the desired cash flows over the retirement horizon. I have a toolkit for that: A Bond/CD Ladder Toolkit if you want to try.

5: Ignoring equity valuation

As we saw in item #2 above, bond yields have pretty much zero explanatory power in accounting for the variations of safe withdrawal rates over time. But what about that big gorilla in the room: equities! If you have a 60/40 portfolio – 60% equities and 40% bonds – then my natural tendency would be to look at equity valuations first. Which, by the way, I’ve done extensively in my Safe Withdrawal Rate Series. I’ve shown that the risk of running out of money in retirement is closely linked to expensive equity valuations at the start of your retirement. Nobody ever worried about the 4% Rule when they retired in 2003 or 2009 at the bottom of the respective bear markets.

A different story emerges for the retirement cohorts in 1929, 1968, 1973, 2000 or 2007 at the peak of the respective bull markets when equity multiples (PE or Shiller CAPE or any other multiple you prefer) were dangerously elevated; those were the times when folks indeed worried about their retirement safety. Though never enough to reduce the withdrawal rate to below 3%, not even in 1929, not even over a 60-year horizon starting in 1929!

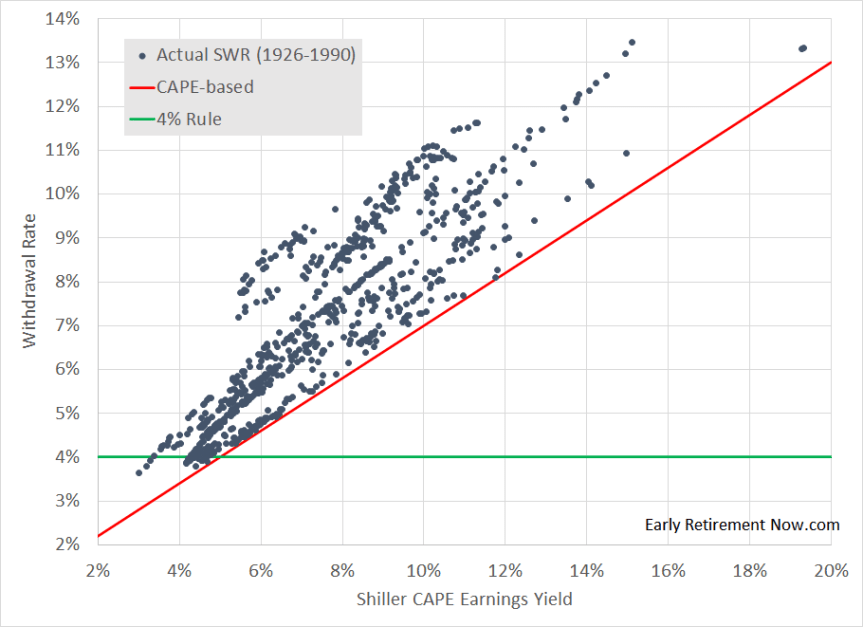

So, let’s create the same scatter plot as above but use the equity valuations as measured by the inverse of the CAPE ratio, also known as the CAEY (where the EY stands for earnings yield) on the x-axis and compute how actual safe withdrawal rates would have lined up with that earnings yield between 1926 and 1990. And again, I have to stop in 1990 because July 1990 is the last retirement cohort for which I have a complete 30-year return window for my simulations. But I do use all return data until 2020!

Let’s look at the chart below:

Aha! Now we’re getting somewhere! That’s a much better correlation than with the bond yield. And it makes sense: The CAPE is very correlated with the forward 10-year equity return, and the first ten years of returns during any retirement window are extremely predictive for retirement success and hence the safe withdrawal rate. Moreover, even though equities may have a share of “only” 60% in the portfolio, a slight majority, equities still account for the overwhelming majority of the portfolio volatility. This is the point I made in a post a long time ago.

Notice, in the chart, I also added a straight red line but not in the way you’d normally see it – a uni-variate OLS-fitted regression line that tries to optimize the fit through the scatter plot of dots. You don’t want to that to determine your fail-safe historical withdrawal rate because that would have failed roughly 50% of the time. As a cautious financial planner, you want to fit a lower envelope line that hugs the dots in the scatter plot from below. I fitted that with an intercept of 0.01 (1%) and a slope of 0.6. Since the current CAPE is around 30, that would translate into a fail-safe withdrawal rate of 0.01+0.6/30=0.03=3%. Lower than 4% but much higher than the 0.5% recommended with his model.

Also, notice that the chart above is a nice way to showcase everything that’s wrong with the Trinity Study and the traditional naive 4% Rule! The 4% Rule is unsafe when equities are very expensive, i.e., today! All the failures occur when the earnings yield is below 4.5% (barely above 3% today!). Likewise, the 4% Rule is too conservative for retirees who find themselves not at the peak of the stock market bubble. You’d be crazy to retire with a 4% Rule if and when the CAPE ever goes back below 20.

Conclusion

Why did I even write this post and provide publicity and a link and SEO assistance to a pretty transparent troll/click-bait post? Well, first of all, I could have certainly written a blog post without linking to the original post on Sam’s blog. But that’s bad style. I started my career in academia and the courteous thing to do is to reference other people’s work properly, even the work you don’t agree with. Not doing so would mostly hurt my own reputation. I’ve seen people attack my work without referencing and/or properly linking to it. I’ve even seen other bloggers remove comments linking to my blog. I don’t want to copy such punk and antisocial behavior, so the respectful thing to do is to properly link to the Financial Samurai blog. Even if that means that his troll post will get more traffic out of it. Even if I suspect that Sam will not link to my post if he ever decides to write a follow-up to defend his work.

I also think that it was a fun exercise to look at this preposterous 0.5% claim and to see where the logic went awry. We learn just as much (or even more) from mistakes. So, I think Sam/Financial Samurai has done us all a favor; he made us think! I learned a thing or two in the process. For example, I’ve played around with dynamic, valuation-based withdrawal rates before, most prominently the CAPE-based rule (see Part 18 of the SWR Series). I’ve always thought that one has to factor in bond yields as well, not just the Shiller earnings yields. But adding the bond yields didn’t ever get me much. I understand why; bond yields are not predictive of retirement success if you have a 60+% equity weight. Low bond yields can be bad because 40% of your portfolio has low expected returns. But low yields can also be a blessing when we have an accommodative monetary policy, and your equity portfolio will go through the roof! In other words, it’s possible that for every $1 you lose due to lower bond income, you also gain more than $1 in extra equity returns! That certainly appears to be the case historically.

Also, as wrong as Sam’s calculations may have been, he was on the right track. Asset valuations matter for withdrawal rates. Ignoring this is one of my main pet peeves with the Trinity Study and some of the FIRE blogging scene. But you gotta use the valuation of the relevant asset: equities!

So, to wrap up, would I think that the entire FIRE community is now breathing a sigh of relief in light of my rebuttal? Certainly not! The 0.5% withdrawal rate, thankfully, was just so outrageous and so transparently false and asinine that I can’t imagine anyone would have taken his post very seriously. Though, never say never. Apparently, Marketwatch picked it up. But maybe they ran out of things to write about during the slow summer months. And I wouldn’t be surprised if Suze Orman endorses the claim that you need $8m to retire. But people serious about finance and math will probably use a baseline, bare-bones Safe Withdrawal Rate in the 3.00-3.50% range if they are young and have a long horizon. And you can use significantly higher rates if you expect generous company pensions and Social Security later during retirement or if the CAPE ratio were to go back to more normal levels! Check out my Safe Withdrawal Rate Series (nominated again for a Plutus Award in 2020), including my free Simulation Tool to find out more!

Thanks for stopping by today! Looking forward to a lively discussion again!

Title picture source: pixabay.com

Thanks Big ERN. I think Sam is perfectly well aware of the flaws in his analysis, and his article is about being provocative and generating traffic to his website, which it has done very well. I think most people reading it will be well aware that it was designed to provoke and used some extreme / unjustifiable premises. I just hope nobody has cancelled their retirement on the basis of the 0.5% SWR!

Yeah, the original post as well as the Marketwatch article were pretty much shot down in the FIRE community right away. Had he been a bit more cautious, and twisted the number to maybe 2-2.5% people might have taken it more seriously. 🙂

There’s a meta-point here, and it extends beyond the FIRE community – it is in everyone’s best interest to really think about the information that flashes by their eyes.

Of course, you can’t be an ‘everything’ expert – no one can. What you can do is 1) Dive into things you do know and verify. 2) Find people / places that do the deep dive _and_ show their work – this allows you to find others that can peer review (and you at least can attempt to follow the work). Use the good ones (like ERN!) 3) Find multiple sources – ’cause no one is perfect and we all benefit from multiple _reasoned_ viewpoints.

This is amazingly droll for the news services – they want clickbait; basically they want the people who only say “ooh, look, there’s something shiny!” – it’s a very normal human reaction. Unfortunately, if you don’t go beyond the ‘ooh shiny’ you will _always_ be manipulated for someone else’s benefit.

Thanks Roy! Very good summary of the desirable thought process! But that’s too much to ask from some journalists. 🙂

Thanks very much for the post.

I’m a new reader, so sorry for the long post.

I accidentally run into your blog searching in bewilderment as to why nobody had yet debunked the obviously flawed, sensationalistic click bait post at FS. I tried to infuse some reasoning into FS’s comments section but likely only fed the trolls oven more.

And thanks for adding some quantitative analysis behind what is slowly becoming the 3% rule (subject to further personalization based on circumstances as you wisely and analytically point out).

I’m exited about having found your very analytical articles because I started intuitively using 3% instead of 4% back around 2012 when I realized that below 0% returns on risk free investments were not a temporary thing but a more permanent and now implementable long term strategy of financial repression on behalf of central banks worldwide. Looks like central banks — pushed to the limits by a voting supermajority that treats the ballot box as an ATM — have finally mastered all the tricks to squeezing the balloon on all sides and forcing investors to take zero real returns for delayed gratification, so that public debt originating at the polls through the political process may be financed. The risk component of the reward (as opposed to the delayed gratification side ie return on safe investments) seems to still be active for now, I guess central banks have not been able to squeeze that side of the balloon. However the ultimate fate of those who took refuge in the equity risk bet may not have been written yet, as implied by the perilously high CAPE ratios. CAPE ratios may continue their bubble for years but even so, high CAPE ratios mean low future returns even without a market correction.

To give just 1% of slack to FS over his nonsensical rule (just 1% i.e. from 4% down to 3%) I do want to say that in some ways this time in human history may be different, somewhat. As I eluded to above there has never been a time in human history when central banks have been successful in closing all exits and forcing investors to accept lower returns (in order to finance debt instigated by voters at the polls) so we may indeed be living in a uniquely different era in at least some aspects, hence I fully agree with you in trimming a whole 1% from the crude 4% rule.

I also see the probability of some tail end black swans increasing. Seems like we are following Japan. The entire world seems to be Japanificating. No retirement plan can survive the essentially zero Japan-like stock market returns of the last 30 years. That is no longer a remote possibility for the US as our monetary policy seems to be Japanifying in many aspects.

Worse, talking about other political risks, I see most Americans poised to take a big step towards converting the US towards a European welfare state, with the endemic 1-2% European long term growth rates that inevitably accompany such transformation, surrounded by a world that is growing two to three times faster. I cannot possibly see a future of sustained high returns in that. After all, in the long term, economic growth is the wellspring of almost all equity returns. To me, a CAPE ratio of 30 (32 lately) would require the dynamism of unfettered capitalism in the best of circumstances, yet most American voters seem to be excited at the prospect of becoming a European welfare state. Something does not jive here for me and I think we might be in for long term structural surprises when it comes to expected equity returns in America. I’m particularly aware of this because, like you, I’m a European immigrant to America, I have lived and worked in both environments and believe American market participants are woefully ignorant about this political risk and the reality of such trajectory. That is where I see the biggest risks. Other than that I would be less skeptical of simulations and analyses that predict the future by extrapolating the past, which is what I have done so far myself but I’m now starting to have more doubts.

Well, this is already a long comment so I’ll leave it at that for now.

I have heard that once you take a couple of stocks (FAANGM?) out of the market, then the CAPE goes down to more reasonable levels. I cannot find the original article, but it does seem that if the FAANG make up 14% of the SP500 it may influence the CAPE.

Any thoughts?

It makes sense that average CAPE ratio of SP500 without FAANGS would be lower but that may not be something new. The most successful high growth companies in an index have typically had high CAPE ratios. So I imagine that if you exclude them from the index the average CAPE ratio of that index will inevitably drop. The issue is whether this effect is particularly intense today or has more or less been that way for a long time.

I imagine that pockets of low CAPE ratios have always existed, even in overall overvalued markets. For example, it would be interesting to examine how the CAPE ratio of a value fund, say VVIAX, has evolved over time. Does anyone know how to get that information?

Very well said. I replied a minute ago, but you put it more eloquently than I! 🙂

Not sure how to get non-index CAPEs, unfortunately. star capital has the CAPEs for different countries: https://www.starcapital.de/en/research/stock-market-valuation/

But I don’t think there’s good coverage for ETF CAPEs

Ha! Such funny coincidence! Star Capital has also been my main source for the CAPE ratios and something that prompted me to see my entire investment strategy in a new light a couple of years ago…

Oh, yes, the big tech companies make up an insanely large portion of the S&P. If we took them out, you’d have a lower CAPE. But you also have less growth potential. 🙂

These are all very valid points. I have some of the same concerns about the European politics making inroads here. How ironic that I tried to escape that nonsense, and now it’s coming here.

Overall, I’m hopeful though that we will prevail. Japan was in a very different situation in 1990 (much higher CAPE). So, I still hope that we can grow out of the problems we face. And as a hedge, your 3% WR should be safe.

“How ironic that I tried to escape that nonsense, and now it’s coming here”. You don’t know how many times I have spoken those very same words! I am happy to discover that someone like you who has made a similar shift, seen and operated in both worlds, but with far superior quantitative skills to mine, has arrived at the same conclusion.

Haha, thanks! Glad this resonates with you! 🙂

Thank you for another well written post! It’s interesting that we still have such little data on historical SWR for such low Shiller CAPE earnings yields, I’m sure it’s difficult for today’s retiree to know if 3 or 3.5 percent is preferable looking at the sample size on your chart.

Well, we have the data on 1929 (CAPE>30) and 1960s (also high but still below 30) and 2000 (CAPE above 40), though for the 2000 cohort we don’t have the 30-year return data yet. But the error bands are wide, for sure. But 0.5% is definitely too high.

“people who are serious about finance and math will probably use a baseline, bare-bones Safe Withdrawal Rate in the 3.00-3.50% range if they are young and have a long horizon.”

I thought 3.5% worked for even 50-year retirements?

The SAFEMAX for a 60/40 and 50-year horizon dropped below the 3.50% mark a few times in the 1960s.

“Let’s assume you indeed retire with a 100% bond portfolio. I don’t know anyone who does this, certainly not in the FIRE community,”

Isn’t that what Joe Dominguez advised in Your Money or Your Life?

Yes, back then the government paid Joe 23% a year interest and came by to give him his quarterly back rubs. They aren’t as charitable these days.

If anything, YMOYL was a good example of how one size does not fit all and that it’s a lot better to understand why you’re doing what you doing.

Yeah, these were the good old times for bond investors! 🙂

Good point! Long time ago, that was certainly a good enough strategy. In fact, as I wrote in the post: 1998 was still a time when you could simply do a TIPS bond ladder and forget about all market risks for the next 30 years.

But subsequent editions of the your money or your life book have deemphasized the bond approach, in light of much lower yields.

Don’t feed the troll, Big ERN. Sam’s articles are all clickbait at this point.

Yeah, I’m monitoring how many people click the link back to Sam’s blog. Not that many! Less than 4% of the visitors! 🙂

I did see and read his article first and so no need to go back to it from your post. I support the use of citations! Great post. I was pretty confused by his article, but it makes sense if it was just for exposure. I’m going to keep that in mind if I ever read one of his articles again.

Thanks! Yeah, I heard that same feedback from several people: The FS article didn’t make sense 100% but people couldn’t put their finger on it, where exactly the flaw was. Hence, my post. 🙂

Not sure how you can live on anything less then 8m, We are all going to look back and wish we had listened to Suzy so we can avoid all these plagues on our private islands.

I know: you need boats, private planes, etc. With only $8m you’ll end up “island poor”, eating rice and beans every day!

3-3.5% is still low. I beginning to think that the best is the WARM strategy portrait on Jlcollins blog where you forget to craziness of the market and just invest in tips and burn everything down until you reach 100 yrs old which I know for sure I’ll never reach.

I don’t like that approach. I commented on JL’s post back then and I just copy my reply here:

“WARM = worst advice regarding money

I need an $80,000 p.a. withdrawal plus an inflation adjustment, most likely 2% p.a. Over a 60-year horizon, I’d need $4,8000,000 if I were to ignore inflation or $9,124,123 if I were to add up $80k plus 2% inflation annually. I don’t have that kind of cash. I have “only” 3 million dollars. With $3m initial capital and annual $80k withdrawals, I can likely make the money last due to the low withdrawal rate.

Your WARM method allows me to withdraw only $50k per year ($3m/60). I’d rather start with my $80k and in the highly unlikely event of a 1929-repeat I might just reduce my withdrawals to $50k and still do no worse than the WARM method”

So glad you wrote this — hopefully it can walk back some of the damage the original article may have caused. FS’s initial article was so frustrating because some people likely believed what he wrote. It is disappointing that someone so big in financial blogging would write such a flawed recommendation. It either displays gross ignorance with regards to finances or negligence with regards to his readers. Either way it is a strong suggestion to not trust what he writes.

Thank you for doing the right thing through and through. It is a testament to your leadership and hopefully encourages others to do the same.

Thanks, AZ! Again, I don’t think that too many folks in the FIRE community took this seriously. But I still saw the need to write one deep article to showcase the logical flaws.

Very informative analysis. Thanks for spending the time to research Sam’s false claims. You are a class act and I’m glad you have Feberal Reserve experiences to draw upon! Stay safe!

Brian Carlisi

Awesome! Thanks for the compliment! 🙂

Thankyou for explaining so extreme well much appreciated

You bet! Thanks for the feedback! 🙂

Yes, a catch-22 in drawing more undeserved attention to what is clearly a severely flawed and minimally researched piece. But kudos to you Ern for not idly sitting by and allowing such a lazy and ill conceived piece to exist without a thorough dismantling and deserved rebuttal. Thank you.

Yeah, it’s a catch-22. So far, not many readers have clicked the link to the troll post, though. 🙂

ERN,

I suspect you will have a lot of comments to this post and you’ve nicely laid out why tying the SWR to a single fixed asset is flawed. To my larger point, we seem to be living in era of simple black and white statements and missing the analysis and nuance needed for a deeper understanding. A 4% SWR “suggestion” more than a “rule” would be one place to start. But, you have a whole series on this. As you point out, understanding real vs nominal returns is fundamentally important and running a simulation is part of the critical analysis we need. I expect nothing less from you as an economist! Keep up the good work. I’m just waiting for Suze to leave a comment on this one.

Good point: I’ve always pushed the point that there are no rules, only guidelines/rules of thumb.

And since Sam and Suze likely consider me a troll now they will likely not comment on this, haha!

Appreciate the analysis Big ERN, you put out by far the most detailed work in the community.

0.5% is no doubt a bit of click bait, or at least it read as click bait to me and it sounds like you as well. Sam does put out some good content on life and financial thinking in general. I’m willing to assume he was just looking to throw cold water on all of us about the validity of the 4% rule in today’s environment, and in that respect, mission accomplished.

For me, this was similar to reading your work the first time, it made me reevaluate some of my previous assumptions. Thats always a good thing, even if the underlying math is not as well thought out as yours is.

Yeah, good points. Thanks for the feedback! 🙂

I started to laugh when I began reading your post. I had unsubscribed to FS’s blog because so much seemed like sheer click bait. As always, your thorough and critical thinking has raised this roast off to new heights. I couldn’t imagine a better way to handle this. Hats off… or should I say spreadsheets off to you!

Thanks, Rachel! We have a lot in common! 🙂

Great post Big ERN!

Especially your charts comparing Withdrawal Rates to the 10Yr. Treasury, and your chart showing CAPE Earnings Yields to Withdrawal rates. The CAPE earnings yield chart really makes the case for more conservative SWR’s in this environment. As you point out equity valuations matter a lot for determining SWR’s, something lost on many in the FIRE community.

Thanks!

Though, the CAEY vs. SWR chart is a bit overly conservative. Some folks have pointed out that today’s CAPEs need to be treated with a haircut: So, a CAPE=30 today is probably more in line with a 50-year-ago CAPE of 25.

Why is a cape of 30 equivalent to a cape of 25 50 years ago?

Due to stricter accounting laws and more profit retention and thus more internal profit growth, the CAPE today may seem higher than decades ago.

The y-intercept at 1% and the slope at 0.6 in the CAPE earning chart are nearly identical to the a=1.0 and b=0.5 values given in traditional CAPE-based withdrawal rules, as mentioned in part 18 of the SWR series. Would these “lower envelope” values be expected to change much for a retirement of 40, 50 or 60 years?

Very true. This was calculated for a 30y horizon. Strictly speaking, the 40+ year horizon would have a lower intercept and/or slope.

But keep in mind that a CAPE-based SWR will never run out of money if you regularly adjust it. You’d only potentially suffer a decline in your purchasing power. I think you can do a=1.75% and b=0.5 and do pretty well.

Hi ERN, a related question: so in your equity-valuation SWR chart above, for the CAPE-based SWR line that would have been fail-safe, how did you determine that the line should have an intercept of 1% and a slope of 0.60 (instead of, for example, 1.5% and 0.50 as an alternative). Was 1% and 0.60 the best fit for the scatter plots? Is using a 0.60 slope related to having 60% portfolio equity allocation (60/40 portfolio)?

Pick a line that hugs the dots from below. I could have done something more scientific, but this was just trial and error. 🙂

And yes, the line depends on the 60/40 and the horizon. With different asset allocation, you’ll get different parameters. With different horizons you get mostly a different intercept (but also slightly different slope).

I appreciate you spending the time to throughly debunk a troll with math and research even though I knew as soon as you mentioned FS that whatever he claimed was likely bunk. Keep up the good fight!

Thanks Carrie! Glad you were one of the many folks in the FIRE community who knew to take FS’s post with a grain of salt! 🙂

He decided he wants to go back to work.

He does not like work

He needs to rationalize his decision.

There is your rationale.

Yup, that’s the rationale! Excellent point! 🙂

Fair analysis. However, Sam’s point about the risk free rate and risk asset returns being intertwined is true. Valuations are very expensive for stocks and bonds now. To assume historical returns now seem aggressive, especially if one had already retired.

One thing to mention. Your use of name calling cheapens your post. You say you were an academic researcher, but I’ve never seen academic researchers use your type of language to refute an argument.

May I ask if you’ve been withdrawing at 4% since you retired? If not, what has been your withdrawal rate?

When the shoe fits…FS put out some rubbish analysis and Big ERN called him out on it. I unsubscribed from FS due to his very casual / offhand and anecdotal, less data-driven approach to analysis [As someone with a graduate STEM degree and a Finance employment background I can attest to this. :)]. While FS, Mr. Money Mustache, and Go Curry Cracker were first in the space, and should be appreciated / given their due, newer, more thoughtful FIRE bloggers like Big ERN and White Coat Investor have dramatically improved the analytical quality, objectivity, and work product in the space and so have seized thought leadership for those willing to dig into their content. I count myself fortunate to have access to the content at these sites, including FS, for a price dramatically lower than a paid advisor and have put it to good personal use. Big ERN is the most analytical and thorough gem in the personal finance space, and If you read his safe withdrawal rate series you would know the answer to your own question.

Wow! What a great description of Big Ern’s role in the Fire community. I could not agree more. He truly is a gem!

Thanks! Made me blush! 🙂

Wow, thanks for those kind words! You made my day! 🙂

I like all viewpoints. But here’s the reality. Although ERN’s safe withdrawal rate is thorough, how many people are actually reading it compared to the other sites? Much less.

If you cannot get your message across, is it really effective? This is the problem with some writers. It’s just not interesting enough to understand or read so people don’t.

Yeah, let’s listen to the loudest voices even though they are wrong. That always works really well.

To your claim that nobody reads my series: thanks to all the faithful readers that have nominated my blog for the Plutus Awards. I’ve made into the finalists list two years in a row in two categories.

Providing punchy bullet points based on shoddy analysis and erroneous conclusions is worse than providing no information at all, in my humble opinion. Being controversial merely to stimulate a conversation without presenting a proper argument is an insufficient rationale for self-publishing.

Well said! Thanks! 🙂

You’re preaching to the choir. My whole point of much of the SWR series is that high valuations call for lower SWRs. But not 0.5%. 3-3.5%.

Maybe you can point me to the part of the post where I’m name calling. The post was click-bait. It was a troll post. I’m calling it the name it deserves. I could have given it much harsher names but we want to keep things family-friendly.

Also, if you ever spent some time in academia you’ll notice that the climate is much rougher than anything I’ve ever written on my blog. Mind you, not in book publications or journal peer reviewed articles, but in all other communications, people in economics would have used much less family-friendly language. At least back when I was active, before 2008.

I’ve not been withdrawing 4%. Closer to 3%. I practice that I preach.

Nice job of debunking, intuitively I knew his results were off but now I know why. I do like Sam’s posts often, he gets a lot of reads because he does throw things out there that are counterintuitive, but like you said, I do think he serves a purpose by making us think about the status quo and consensus opinions. It never made sense to me to link safe withdrawal to bonds when equity growth was what kept portfolios growing faster than inflation. Also in the past when bonds paid high rates most people tend to forget that inflation was also sky high so that they weren’t all that great an investment then either. Thanks for putting so much sweat equity in this, I think a lot of people were unnerved by the .5% post and you’ve reduced stress a great deal.

Yeah, that’s point #2 and #3: when bond yields were double-digit, you also had double-digit inflation. Especially during high-interest rate periods would the 0.8*10Yyield rule fail. It’s because the real yield was not high enough to sustain such a high WR over the long term.

Whew, I guess I can pull my resume back from all those headhunters I’ve been fishing it out to since reading Sam’s post. Thanks for helping me avoid going back to work, I’m rather enjoying this life of retirement. Wink.

Haha! We all dodged a bullet there. No need to tell the tell the wife to switch to rice and beans after all! 🙂

Thanks for stopping by, Fritz. Safe travel on your epic road trip!

Kinda sad, I used to think FS put out great content until a few years ago he decided to go back to work and seemed to decide that if he’s no longer retired then no body else should be either.

Another great article big ERN!

Hah, that’s a good point. I think he not only wants to rationalize his own decision but also make everyone else in FIRE feel bad. Yeah, makes sense! 🙂

Great article, backed by math and sound logic. Thanks for the contribution!

You bet! 🙂

I think Sam was just having fun with that post. He seems to enjoy creating some controversy and discussion! But your wonderful mathematical analysis of his 0.5% proposal was awesome to read, as is all your content. It’s good to know that a 3% withdrawal rate is a fairly safe number to use, even when analyzed by a financial expert with rigorous mathematical and historical data. Great job Big ERN!

Thanks Heather! Glad you found my logic more convincing than Sam’s! 🙂

Thanks for this great article. Could you maybe do an article on CAPE and why it might not be so relevant anymore? As far as I know there are at least 3 important factors why current CAPE levels are so high:

– 10+years of record central bank interest rate, effectively 0%.

– Corporate stock buy backs, are at record levels

– Foreign investment in the US equity markets is at record levels, from ~11% in 2000 to 24% in 2019

– etc.

I’ve replied to enough questions in the comments section that I actually should do another post on the CAPE. It’s on my to-do list.

The CAPE is still relevant but you have to do an adjustment to account for stricter accounting methods (will lower earnings, raise the CAPE compared to historical measures).

+1 on your CAPE article!

I second that motion! You’re our CAPE-Crusader. 🙂

Great Post – when Sam put out his original post, I commented that the post was elitist, ridiculous and didn’t account for many of the areas that ERN covered in his SWR series. I specifically recommended people check out ERN’s SWR series. My comment was magically never approved / posted in Sam’s original post. Definite clickbait with no basis in any real analysis!

Yeah, I heard that before. Sam’s behavior, screening out voices he disagrees with, does not really give him a lot credibility. I know that he knows he’s wrong! 🙂

Thanks for the post. I was secretly hoping you’d challenge that one!

FS had some good articles before where he even talks about not freaking out about inflation due to stock returns, not relying on the “safety” of bonds, and typically recommends a high percentage of stocks. However, I’m not an academic and I’m lazy so I won’t find all of those posts I read a few years ago.

Ultimately though, he’s big on stocks and real estate so I’m not exactly sure why (I could speculate but I won’t) he’s going with 100% bonds in his example right now and his DIRE stuff and all that.

Well, I’m still confused where he’s coming from. He’s doing the math like he’s 100% in bonds (but even that’s flawed, see point #4) but he has mostly stocks and real estate in his portfolio. Very strange.

I’m not enough of a Maths head to comment on the bulk of this post, but I wanted to say I thought your explantation of why you linked to Sam’s post was courteous and very refreshing to read. I’m getting very sick of people on my Twitter feed telling me to unfollow someone just because they wrote something (or linked to something) that the Twitter pack disagrees with.

When you’re my age, you reserve the right to make up your own damned mind!!!

🙂

Haha, that made my day. Yes, I think I’m old enough, too, to decide what I want to read and link to. That’s a very eloquent way to rationalize linking to the original post. Excellent point! 🙂

FS website has always been full of hyperbolic clickbait to put it kindly. He’s the Suze Orman of FIRE bloggers. Impossible goalposts and unrealistic numbers even for the most frugal and well paid 6 figure minions. I’m happy to say I missed his 0.5 article but I am enjoying an academician debunking it with this thing called math. Cheers!

I think Sam is secretly hoping for getting a shout-out from Suze. Maybe he can become Suze’s assistant on the show, reading the emails?

That guy has been in the business of clickbaiting and generating traffic to his blog forever now. You’re helping him even by debunking his obvious crap.

Terrible to think such a person is one of the most prominent “financial” bloggers out there

Agree. I thought his stuff was good in the beginning (wayyyy, long time ago). But then I started noticing sloppy math and also that clickbait stuff.

While reading through comments, this WARM method by JCollins caught my eye. I don’t have time or interest to google his blog post, but I am curious now: Was it a click type article on Jim’s blog? If so, I’m very surprised because he was always for a heavy equity portfolio and generally much more relaxed with his advice (based on his book “Simple Path to Wealth”?). Has his advice style suddenly changed to conservative? I’m guessing one has to be very careful what they read even on the blogs that they respected before. I never got ‘hooked on’ FS, but I used to read JCollins blog, but now I wonder if I should put this blog in a ‘dog house’ too.

PS. Thanks for this article. I have a question about this quote towards its end.

“I understand why; bond yields are just not that predictive for retirement success if you have a 60+% equity weight. Low bond yields can be bad because 40% of your portfolio has low expected returns.”

But didn’t your article written after the market drop in March say that one should be very careful if retiring with an equity heavy portfolio and that it would be more advisable to have at least 30%-40% in bonds to make it safer? Can you shed some light on your contradictory notes (at least that’s how I interpreted)? Unless all ‘average investors’ like myself learn to trade options, it’s hard to see the middle ground of AA even when reading your blog which I like BTW ;-).

Thanks.

The WARM portfolio was a guest post, not JL’s opinion:

https://jlcollinsnh.com/2017/09/09/sleeping-soundly-thru-a-market-crash-the-wasting-asset-retirement-model/

Again, I’m no friend of this because it’s way too conservative. Essentially you withdraw 1/n, where n is your horizon. So, only 2% with a 50-year horizon.

In regards to Financial Samurai… he is more like like a Financial Donkey. He intentionally writes controversial blog posts to generate traffic to his blog. While reading just few of his blog posts, you get a feeling that this guy is just doom and gloom. I mean, there is nothing educational on his blog. Just speculation and negativity. The message he tries to convey is that no matter how hard you work and save, it will be not enough… work until you are dead.

On one end of the spectrum there are AWESOME blogs like BIG ERN’s and then there are garbage ones like Financial Donkeys.

Please keep up the great work of educating the world. Thank you, BIG ERN, for all you do.

Thanks, Jacob, for your kind words!

Good to know that even though I’m just a little bit doom-and-gloom sometimes, people still take me seriously. 🙂

Even if it was “obvious” you taking your time to do the actual math was great and reassuring. Thank you

Thanks! Glad you found this helpful! 🙂

Thanks for your post and all the readers’ comments about Sam’s post/blog. I didn’t realize that his post was click-bait even though I knew that his numbers were hyperbolic. If all his numbers were true, then 99.5% of people would need to work until they’re dead.

Yeah, not many people can retire if they target 200x instead of 25x.

Hi Karsten,

You stated “You’d be crazy to retire with a 4% Rule if and when the CAPE ever goes back below 20.”

Do I understand you clearly that even 6% or more % would work let’s say that CAPE would be at some crazy number like 6.

Also,

You stated “I’ve shown that the risk of running out of money in retirement is closely linked to expensive equity valuations at the start of your retirement” – so simple answer would be get portfolio more conservative for a while aka limit contract/make smaller standard deviation until you can glide back up again?

Lastly, I read Sam’s blog and I am pretty sure he will take your constructive criticism and make it right. No one is perfect. You guys might just become friends because of it. Life has it ways of bring people together.

I have to write my own reply. After reading all these comments, I feel that I was last to get out of the “naive reader” party at FS. Sam from FS if you read this comment unfortunately, I am not coming back to your site.

BTW – I don’t think you a troll at all Karsten, you are just really smart and make very valid points and provide very actionable analysis that is hard to prove wrong. For me your blog is almost like an academic paper written little bit as entertainment,.just a little bit.

Thanks Karl! That made my day! 🙂

Yes, definitely. The SWR were really high when the CAPE went that low.

Definitely, you’d want to start with a higher exposure to low-risk assets initially. Then shift back to stocks again. See parts 19, 20 of the SWR series: Glidepaths

Oh, that would be marvelous if Sam could take this as constructive criticism.

I enjoy and religiously follow both Big Ern and Financial Samurai. I find both add much more value to my life than detract from it. Thank you both!

Big Ern – I LOVE your approach to these complex challenges. Just amazing work as always. I find your work to be the best of any I see on the web. Thank you for your logical approach and for saving me for doing A LOT of math. 🙂

Thanks, Crusher! I’m glad you found this post helpful and it saved you the time to do a lot of math. Hey, someone has to do it, it might as well be a guy who’s retired now! 🙂

Thanks for the very informative article. In my opinion Financial Samurai has turned into the equivalent of the Financial Enquirer making money out of click and bait traffic from naive lakeys. His articles and comments are inconsistent at best and if you seriously challenge him in the comments he just deletes them.

I want to question the universality of the typical 40/60 bond/stock allocation and perhaps provide thought for a future article.

I am at 50X expenses, so I’m presumably on the very safe side of retirements at a 2% SWR and thus very high chance of capital preservation. Therefore I look at my stock/bond allocation primarily in terms of my young children’s time horizons and lifespans not mine. In that context I’m almost entirely stocks with only 5% bonds. Is that unreasonable?

Haha, I got a good laugh out of the “Enquirer”. I always see that at the checkout at Walmart but never made the connection that this applies to blogger sometimes. 🙂

And yes, with a 2% WR you should be ultra-safe!

“I think Sam/Financial Samurai has done us all a favor; he made us think! “. Don’t let a good controversy go to waste even if it’s generated by hyperbole. Rationale minds will prevail but only if folks start to think about it. Sadly, IMO a lot of folks don’t (well maybe not readers of this site).

Yeah, well said. Thanks! 🙂

I’m confused by this line “The 4% Rule is based on the lowest withdrawal rate that would have survived a 30-year window post-1926.” Do you to say the HIGHEST withdrawal rate? Certainly a SWR of 0.000001% would have beaten a 4% SWR.

Ooops, you’re correct. How could I miss that? I corrected that sentence. Thanks!

Ok! Just wanted to make sure I wasn’t missing something. Great stuff!

Ern FYI

Bill Bengen revisits the 4% rule wrt CAPE.

https://www.fa-mag.com/news/choosing-the-highest–safe–withdrawal-rate-at-retirement-57731.html

Your comments on the his analysis would be interesting.

DP

Please see the discussion on Triwtter with Michael Kitces and me (after the Fervent Finance reply):

https://twitter.com/ferventfinance/status/1301148020185202690

It’s mostly equity valuations. And that there’s probably some data-snooping/overfitting n the Bengen analysis. Bengen seems to claim that 5% is safe today, which seems completely insane given the CAPE above 30.

You would think if Bengen had some kind of revolutionary insight that everyone else was missing that he would share in detail how arrived at his numbers instead of being opaque.

Yeah, very well said! There are a bunch of us (Kitces, Pfau, myself) who would have pointed this out already.

I never read Sam’s post but glad that you took the time out of retirement to clarify it–especially as you WERE a practicing economist, unlike him. It’s always nice to see another perspective from a professional. I often take note of your ideas to tinker with for when FH and I take the plunge into early retirement in a few years!

Great point. There is a very large difference between different “Finance” practitioners. I believe Sam was in Equities, which is glorified sales. The folks like Big ERN running the detailed quant analyses on both the sellside or buyside are in a completely different analytical league on average. That is why people should focus on Big ERN and leave the banal sloganeering to FS.

Haha, Very true! I will show this comment to some of my finance buddies and former colleagues in equities/sales! 🙂

Thanks George! Glad you found this helpful! 🙂

Actually, “practicing economist” is a misnomer. And economists in finance are the butt of all jokes because they never get their forecasts right. No skin in the game.

You want to investment with people who are producers, not cost centers. If you are a not a producer, you get pushed out because you are a cost center. Big ERN knows this.

I’m PhD economist (but also CFA charter holder) who worked on the investment side (the buy-side, not the sell-side). I find that blanket statements like that are not very helpful. The typical “chief economist” office is indeed a cost center that doesn’t contribute much to the investment side in terms of asset allocation insights. But they are useful nevertheless because the economist crew are there to “advertise” the firm, go on TV shows, travel around to visit clients, etc. They are sometimes the “butt of all jokes” but they serve a purpose.

In many areas in finance, there is very little room for economics: stock picking, high-frequency trading, etc. But in GTAA Global Tactical Asset Allocation there is. People who don’t understand macro trends will do very poorly in that space. From my personal experience, though, the economics/statistics/econometrics tools applied there have to be more specialized than the “fluff econ stuff” that the chief economist puts out every day.

So if your comment was intended as an insult in my direction, I just have to smile. Economists and their skills are highly sought after everywhere in finance, not just the sell-side.

I am a big fan of your blog and I generally agree that Financial Samurai’s posts seem to be a bit sensationalist these days. Thanks for taking the time to replay the arguments for the SWR. I shall resist the temptation to click through to read it!

I did see a more serious blog post here: https://www.finumus.com/blog/low-interest-rates-and-the-safe-withdrawal-rate-swr

The argument is that market forces should link the annuity rate and the safe withdrawal rate. In the UK, the annuity rate is around 1.7% for an inflation linked annuity for a 55 year old. So the author (Finumus) argues that must be the SWR – even an upper bound on the SWR. It generated a bit of a comment storm and points were made about the additional margin that the annuity provider needs to take, the fact that not may people actually buy annuities, but there were several people agreeing with the point.

I commented at the time that it all comes down the stability of the equity risk premium.

“The 7% real discrepancy between equity and government bond returns over the long term was pointed out in a 1985 paper by Mehra and Prescott and is known as the equity premium puzzle (EPP). The best explanation I have heard for why the EPP exists is from the paper by Schlomo Benartzi and Richard Thaler in 1995 “MYOPIC LOSS AVERSION AND THE EQUITY PREMIUM PUZZLE”. https://www.nber.org/papers/w4369. This impressive paper quantitatively explains the EPP using empirical levels of loss aversion (3 to 1) and the assumption that people (including insurance company managers) feel losses every year as though it has crystallised even if they do not sell the shares or bonds.”

Finumus is also implying that back testing of SWRs over a long period of time does not take into account a long term trend of reduced interest rates and hence the next 30 or 60 years may well be statistically different from the last 30 or 60 years.

I would love to hear your thoughts on this.

Absolutely: IF you run a 100% bond portfolio, then link your SWR to the bond yields. I did a quick calculation and find that with a -0.5% real rate and 40-year horizon, you’d be able to get to about 2.26%. And this doesn’t even take into account people passing away earlier, so annuity yields (for CPI-adjusted annuities) should be even higher. Still an impressive number. Not sure where the 1.7% came from. Is it so low because of fees?

But if you accept a bit of equity risk you can go higher, to about 3.25%.

Thanks for the link about the EPP. Intuitive and good explanation!

I studied economics under Ed Prescott and he was my PhD co-advisor, so I appreciate all work that follows up on all the important issues that man has raised in his career. He won the 2004 Nobel (not for EPP, but for other, equally important work) and very much deserves the prize.

Back-testing the way Trinity does it is indeed problematic if you don’t condition your SWR on market valuations. But I do that. So, that objection is not only not valid. It’s one of the main points I’ve been making myself on my blog since 2016.

Interesting link to Ed Prescott! Was that at Carnegie Mellon University? On the Benartzi paper, since my financial independence depends on it, I find it really reassuring to get some more of a theoretical basis for for the EPP – perhaps a topic for a future ERN post one day :-).

University of Minnesota. Went there for the Econ PhD 1996-2000.

Hah, I might do a post in honor of Ed and the EPP. I’ll think about that! 🙂

Thanks ERN for the analysis, I agree with your assertion that 0.5% is very conservative.

However I noticed most of your analysis is based on the US stock market return during the last two hundred years. I noticed rather low safe withdraw rate base on other countries which are even lower than 0.5% in based on historical return in Other countries for example Germany 1914 retiree faced 1.01% return, Japan 1937 retiree faced 0.27% SWR.

https://retirementresearcher.com/4-rule-work-around-world/

So taking statistics on one country investment return may mis-lead on the result. I wish if we expand the analysis to be the median of countries returns rather than the US, considering the investor is likely to diversify or the US may have lower return than the rest of the World based on equity valuation.. also it is likely to fix the country bias on the analysis ..

Based on the above article the median SWR is likely to fall around 2.5-2.8% for the Whole World Stock Market.

The US will not suffer the same fate as much of Europe during 2 world wars, i.e., bombed to pieces, occupied, etc.

Or who is going to invade the U.S.? Canada?

Thanks for your reply.

Without converting the discussion to be a political debate, many countries/Empires had suffered from Wars or Geo-political situation which degraded the future returns of the equity and impacted the SWR. that why taking one country as source of data is quite mis-leading IMHO.

The US had a Civil War back in 1861-65 ..Which happened to be 5 years before the data used in your analysis. (I am not sure if this a matter of luck or coincident).

Will the US suffer the same situation as Europe back in 1910-1940s. It is very unlikely but it is still remotely possible.

My point again using one country as a source of data is mis-leading particularly if the country’s market has drastically over achieved during the window of the study.

http://www3.grips.ac.jp/~pinc/data/10-12.pdf

Thanks for your detailed analysis and your open minded discussion.

Oh, if we have an actual hot war here in the country again, we may see some worse asset return headaches, too. But I don’t see the analogy of bombing entire cities to smitherines as during WW2 in Continental Europe.

To me one of the central parameters is to what extent can simulation of the past predict the future? More specifically, in what ways is the future likely to uniquely diverge from the past?

For example, the Fed has indicated that its future policy will be changing to accept higher inflation (even promote it) so long as average inflation over several years can rise at the 2%+ long desired rate.

So what happens if inflation is pushed to 4% and the 10y treasury is kept repressed to 0.7%? How do you simulate that? How does simulation based on past data contain enough of such a scenario; Such financial repression, now a serious possibility, becomes an unprecedented element of our era, a situation which is difficult to simulate and extrapolate from past data.

There is almost always something unique that makes a new era, the future, different than the past, especially in our fast evolving world. I think that central banks finally having mastered the art of financial repression by gaining the devious competence to close all the exits is this new unique element we will face in our retirement future.

More generally, central banks primarily all over the western world, pushed to the limits by voters who treat the ballot box as an ATM, have finally mastered the art of complete and thus inescapable financial repression, in a last desperate effort to support voter benefits generating at the polls with debt. The result is either debt or higher taxes, both leading to secular permanently low 1-2% growth rates as Japan and Europe attest. It is difficult for me to imagine equity returns matching past average returns built upon western economies whose growth rate has shrunk to a permanently anemic 1-2% annually surrounded by a world that is growing two to three times faster. That is what seems to me different in our era looking forward.

I’d be happy with 4% inflation for a few years to compensate for all the sub-2% years post-2008. I’m more worried about a Japan scenario of sclerotic growth.

But back to your question: if inflation spikes then bonds get hammered. But that’s what happened in the 1970s/80s. So this is something we’ve already observed before (though most FIRE folks are too young to remember), And since it’s part of my sims, I believe the SWR with my toolkit will be robust to a spike in interest rates.

Thanks for your reply.

I do see the negative correlation between bond prices and inflation. While that increases retirement timing risk, I also see such variations as a wash over long time periods since bond prices also rise when inflation drops. On the other hand, negative real yields on safe bonds are not a wash but long term permanent weight, long term permanent destroyers of wealth.

So, regarding the bond yield part, I do see the historical correlation between gov bond yields and inflation and I see how even in the 70s and 80s the 10y treasury yield was (on average) higher than inflation, resulting in essentially positive real interest rates for the period. But now we seem to have entered an era of permanent negative real yields on gov bonds — as intentional and likely PERMANENT central bank policy.

In other words, real, protracted (if not permanent) central bank engineered negative interest rates are a new unprecedented phenomenon of our era. In the past, including the 70s and early 80s, the FED either had no desire, no mandate, or had not yet mastered the skill of such successful financial repression. I think that is the protracted new and unprecedented reality emerging in our era. Europe like indeed more than Japan, which BTW matches our political trajectory and likely eventual permanently below world average economic growth.

What does this mean in practical terms to me as an investor? I do pay great attention to past simulations — and I’m immensely grateful for all the great work you have done and presented, indeed more valuable to me than any other financial advice I have found — however I do in the end modulate the final statistical simulation verdict by what I think is unique in our era, namely permanently negative real interest rates on safe bonds. I see -1% to -1.5% real interest rates on safe investments as intentional permanent policy so I instinctively lower my SWR from the 3.4% I would use based on your very valuable research down to the upper 2.x% range, say around 2.8%. However, other than intuition I have no real quantitative method to justify the magnitude of this decrease. At the same time, I hope that the story of those who took the wager to escape from negative interest rates into inherently high risk equities (the FED does not seem to have been able or willing to close that escape door yet) does not end too badly over a long term horizon, like it has in Japan for the last 30 years. I think that no returns over a 30 year period in a major advanced economy like Japan should give every retiree, especially early retiree, jitters — especially when our central bank starts mimicking BOJ methods.

AQR and Antti Ilmanen expect an even lower return of only 2% p.a. for the traditional 60/40 stock/bond portfolio at least over the next decade. And the target scenario of many CBs is indeed a Japanese scenario ww. for decades to come. This may have quite a high probability thanks to CB’s rising power and changing tasks of ensuring employment instead of low inflation.

Anything between 0…4% p.a. returns for a 60/40 portfolio seems possible for at least a decade, probably many more, including structural changes of the market. I am afraid that the past and its proven metrics based on this and on skyrocketing market valuations are of much less help for determining SWR than before. The expected deep disruption or secular change will act as a reset of the whole market and most of its proven metrics have to be built up again.

Thus, a much better SWR estimate than one based on valuations and CAPE is needed to keep insecurity bounded. Therefore, I believe in cash flow based approaches. They are easier and more intuitive to apply and eliminate most problems of estimating the SWR with respect to the SoRR and zero interest rate, see my contributions in the other thread:

https://earlyretirementnow.com/2020/07/15/when-can-we-stop-worrying-about-sequence-risk-swr-series-part-38/comment-page-1/#comment-21059

A 0% real return (2% nominal minus 2% inflation) over the first 10 years of retirement is still better than during some of the pervious worst case scenarios (Great Depression, 1970s).

I doubt that the U.S. Fed wants permanent negative gov bond yields. Before COVID we are at ~zero yields. 3+% nominal in 2018.

I suspect that in 2-5 years, when the COVID situation has blown over, the Fed will again move toward a 2+% short-term target and 10Y bonds will yield close to 3% again.

I hope, at least. We will see! 🙂

Thanks for breaking the Trinity Study down for us Big ERN. I stopped visiting FS after replying to an article about investing in real estate vs the stock market. FS refused to address any of my points and instead made a bunch of incorrect assumptions about me personally which were totally untrue. I believe just wanted me to keep me coming back (more clicks) to refute his lies about me. His links are clickbait and his commentary is inflammatory and provocative. So glad I’m not the only one who recognizes this troll.

Yeah, I heard that too about the personal attacks from other people. Not a good style. That’s what trolls do. They troll. 🙂

ERN, I really appreciate your formulas for modulating the SWR based on CAPE. I’m just doing some catch up reading on your site since I just recently discovered your work. FS’s article was good for something after all since it prompted me to look in bewilderment how come nobody had debunked his sensationalist bait and click post…

In any case…

As I said in my previous comments I had instinctively used a 3% safe long term equities return for my personal finance calculations since about 2012. That was when I realized that the FED instigated financial repression of negative real interest rates was not just a temporary Keynesian tactic but was essentially poised to become permanent policy, since voters treating the ballot box as an ATM left governments and central banks with no other option but to continue borrowing, thus making the suppression of interest rates a necessity of survival to avoid truly catastrophic sovereign bankruptcy in the developed world (Have they succeeded? Sometimes my sleep is delayed thinking about it, the financial system seems to be under a lot of distortion and tension and I’m afraid something is going to give in a big way one of these days in a way we have never seen before, some scenario with different characteristics than all previous data…). Anyway…

Do you think there is a case for also modulating the SWR with an additional factor that embodies the overall economic growth rate of a country? After all even Warren Buffet has seriously said on a few occasions that long term stock returns are tethered to the country’s economic growth rate plus dividends. I personally agree with him about the country’s economic growth rate being the ultimate wellsprings of long term equity returns (I’m thinking 10-20 year periods).

In practical terms, if there were such a formula modulating SWR not only on the CAPE but also on expected economic growth rate (or simulated trailing growth rate) I could make use of it by linking SWR to the political fortunes of the country. After all there are 28 European welfare state data points firmly linking that political fate to permanently very low growth rates. I think that American equity market participants largely ignore this fact, and when I have information that the market at large is ignoring then there’s great opportunity for arbitrage.

So how do we start enriching the already great SWR – CAPE formulas with an additional country economic growth modulation factor? Is that possible? Do you think there are any quantitative methods that would help or do I have to rely purely on intuition again? It is something that goes a lot around my mind these days…

If we start with basic reasoning we could use economic growth rate + dividends as a starting point. For the world average growing at 4% that would translate to about 6.5% assuming 2.5% dividends on a global scale. For a European welfare state (something the US may also become sooner rather than later) we would get baseline growth 1% plus 2% dividends for a long term equities return of around 3%. These would all be real returns net of inflation. We would of course somehow retain the strong impact of the CAPE modulation in our formulas in some form.

Any ideas how to proceed along this thought process, or does it seem like a dead end?

Equity and bond valuation models will already factor in the return expectations for years 1-10. Going beyond that, I can see that lower growth will obviously lower your expected returns for years 11-60 (or whatever your horizon). With the uncertainty over everything so far into the future I ouldn’t want to venture into pinning down GDP growth, though. Could be lower. Could be higher if we find a new productivity breakthrough (AI, cold fusion, etc.). The economy has been called “dead” before. And scientists will always find a way to invent the next productivity booster proving the naysayers wrong.

Hi,

I like reading your article. I like the way you have explained everything. thanks for sharing, keep sharing.

technology news india

Thanks for the well though out article. I’ve always struggled with FS’s personal attacks in the comment section. I remember reading one comment that seemed to challenge whether someone’s kids were smart enough and had succeeded as well as his because they didn’t goto private school? I popped over there and noticed that the latest articles were all sponsored too. It does seem like he is struggling with money and needing to sell out (if he had integrity before).

Oh, wow, that seems out of line. I didn’t know that. Trolls will always troll, I guess! 🙂