October 18, 2021 – After three posts in a row about safe withdrawal rates, parts 46, 47, and 48 of the series, let’s make sure we have the right level of diversity here. Welcome to a new installment of the option writing series! I wanted to give a brief update on several different fronts:

- A quick YTD performance update.

- How does the option selling strategy fit into my overall portfolio? Is this a 100% fixed income strategy because that’s where I hold the margin cash? Or a 100% equity strategy because I trade puts on margin on top of that? Or maybe even a 200+% equity strategy because I use somewhere around 2x to 2.5x leverage?

- By popular demand: Big ERN’s “super-secret sauce” for accounting for the intra-day adjustments of the Options Greeks. This is a timely topic because the Interactive Brokers values for the SPX Put Options seem to be wildly off the mark, especially for options close to expiration. So, you have to get your hands dirty and calculate your own options Greeks, especially the Delta estimates.

- There’s one slight change in the strategy I recently made: I trade fewer contracts but with a higher Delta thus reducing my leverage and the possibility of extreme tail-risk events.

Let’s dive right in…

1: Performance Update

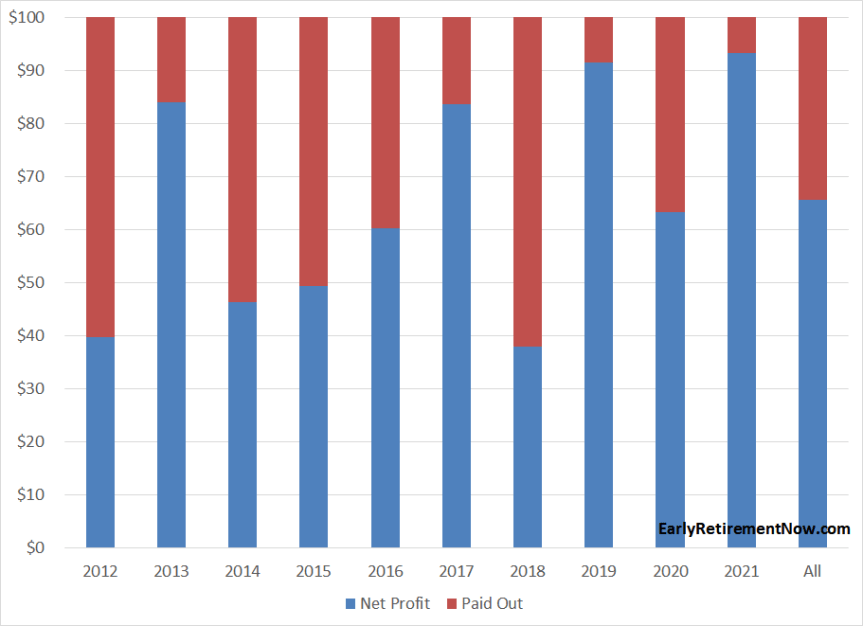

How’s the strategy doing this year? It’s been a pretty awesome year so far. The option-writing portion of the portfolio has done phenomenally well with a premium capture (=net income) of over 93%. In other words, for every $1.00 in option premium I sell, I got to keep $0.93 on average. Pretty sweet because my personal, conservative budget for net income is only 40%, i.e., I budget 60% of the gross option premium as potential losses. Since 2012, the premium capture was about 65%. The record calendar year premium capture was 91% in 2019. I don’t want to jinx anything, but I hope my strikes will hold up until the end of the year and I break another record!

In 2021, year-to-date, the only major loss occurred on May 12, when the S&P closed at 4063.04, lower than most of the strikes I had that day (between 4060 and 4080). But the losses were pretty small, about the equivalent of half a month of put income. I should also mention that I suffered one very minor loss on an intra-day trade, i.e., where at around the market open, I sell puts expiring that same day for a little bit of extra income. That was on September 30 when I sold two extra puts with a 4310 strike when the index stood at 4374 early during the day, only to meltdown toward the market close to cause a net loss of $324.38 after commissions. Not the end of the world!

How about the rest of the portfolio? Under the circumstances, the fixed-income portfolio held up remarkably well! As you may remember from Part 3 of the series, I’ve now shifted more of my margin cash into higher-yielding but also higher-risk instruments, such as (leveraged!) Muni Closed-End Funds and Preferred Shares. And even within the Preferred bucket, I used to have mostly the highest-quality names (Goldman Sachs, Wells Fargo, State Street, etc.) but now I’ve also included some lower-quality/higher-yield names (ATCO, CUBI, SCE, VIASP).

That portfolio of risky fixed-income has worked out really nicely! Not only did I earn substantial interest/dividend income, but I even have a little bit of capital gains YTD. To give you some more concrete numbers, the YTD return so far is 13.39%. 8.40 percentage points came from the put selling, 4.99 percentage points from the rest of the portfolio (i.e., fixed income). Drilling further into the fixed-income returns, 3.76 percentage points are due to dividends and interest, and 1.23 percentage points are due to (paper) capital gains.

Considering the wild ride in interest rates this year – the 10-year Treasury starting at 0.917% on 12/31/2020 and rising to 1.576% by October 15 – you’d think that the fixed-income portfolio would be seriously underwater. The iShares 7-10 Year Treasury Bond ETF (IEF) is down almost 4% YTD and that’s including interest income! So far, the preferred shares and Muni funds have dodged that duration doom. Whew!

13.39% YTD sounds good in absolute terms, but I can already hear the naysayers:

“But, but, but my VTSAX made 18%!”

So, why do I go through the hassle of 3x weekly options trades when I could have leaned back and invested the whole thing “Jack-Bogle-style”? Pretty simple: the IB account does not replace the equity portion of the portfolio. It’s supposed to mimic a small share of the equity portfolio and a large part of the safe-asset portion and thus has a much lower return target. This brings me to the next section…

2: How does the Put Selling Strategy fit into our overall portfolio?

A few weeks ago when I attended the 2021 FinCon meeting in Austin I was chatting about my option-selling strategy with some of the other attendees. Someone wondered if I really practice what I preach in my Safe Withdrawal Rate Series, i.e., keep the equity portion of the portfolio to 75%, maybe a max of 80% to hedge against Sequence Risk. If you were to interpret my IB account as 100% equities (or maybe even leveraged equity) then my overall portfolio would indeed be completely at odds with what I’m preaching on my little blog here. How do I account for the IB account then? Well, let me take stock of our assets first. Our financial portfolio (not counting our primary residence) has the following weights:

- 30.6% options trading at Interactive Brokers,

- 54.1% equities in our 401(k)s, IRAs, and Brokerage accounts,

- 3.4% fixed income in our “cash bucket“,

- 11.9% real estate (private equity multi-family housing investments, excluding our primary residence).

Does this mean that I have essentially 85% equities, 3% bonds, and 12% real estate? Isn’t that a bit risky when I normally preach that we need more diversified portfolios in retirement? Probably not. I would never view the IB account as a 100% equity portfolio equivalent. I’d never recommended a portfolio with 96.6% risky assets and only 3.4% safe assets. I certainly recommend people taking more risk on the path to retirement (see my post on pre-retirement glidepaths) but once retired you should not gamble with your nest egg like that! Since I already have so much of the portfolio locked into risky assets I am looking for a much safer allocation in my IB account.

Then how would I do the “accounting” right? I propose the following methodology. I run a factor model on my portfolio returns since 2014, i.e., I like to see what kind of factor exposures (“betas”) I pick up when I regress my IB account returns on three factors: monthly stock, bond, and cash returns. Doing so, I find that my IB portfolio behaved like a portfolio with Stock/Bond/Cash weights of 31%/38%/31% and an annualized “alpha” (= excess return) of 9.1%. All betas and even the alpha are highly statistically significant with t-stats ranging between 3.4 and 7.5.

If I apply those weights to the 30.6% in the IB portfolio I now get the following overall portfolio weights, see below. Lo and behold, my overall weights are now indeed around 75.5% risky assets (equities plus real estate) and 24.5% safe assets (bonds and short-term instruments). We can also take out the real estate portion and look at the financial assets only, where the split is about 72% stocks, 17% bonds, and 11% short-term safe assets. All right in line with my safe withdrawal rate work, where I’d normally recommend a 75% Stocks/25% Bonds portfolio for most retirees.

3: Calculating Intraday Options Greeks

We had a discussion a while ago about how Interactive Brokers calculates (miscalculates?) their option metrics. People asked me how I do my greek calculations and

Let me outline how I calculate my personal option metrics, specifically, the implied volatility and the option Delta, so I don’t have to rely on the potentially faulty IB figures.

Before we even get into my intraday option pricing model, let me go through how I deal with the accounting of trading days. I have a slightly different approach even for the calendar day accounting in the options pricing formula. I don’t consider a weekend a full 3-day time window. Very clearly, much more can happen between a Tuesday and a Friday close than between a Friday to Monday close. In the former case, we have three full days of economic and financial news released in between while in the latter we have a (mostly) calm weekend and only the Monday news releases. My solution: I assume that a Friday Close to Monday Close is the equivalent of 1.5x of an intra-week trading day. That leaves us with 5.5 “units” every calendar week. Scale that up to 5.5 units times 365.25 average calendar days per year divided by 7 days per week and we arrive at 287. Then subtract the 9 market holidays from that and we end up with 278 effective trading units per calendar year. Not the 250 to 262 trading days floating around you see elsewhere but a little bit more because of the 1.5x scaling over the weekend.

We can now calculate the time input (T) in the option pricing formulas (normally expressed in years). For example, a weekday closing to the next closing is 1/278 years. A Monday closing to Wednesday closing is 2/278 years. A Friday closing to Monday closing is 1.5/278 years. A Thursday closing to Monday Closing is 2.5/278 years. A Friday closing to Tuesday closing when Monday is a holiday and market holiday is still only 1.5/278. You will notice that this kind of accounting for calendar days creates potentially very different inputs for the options pricing formula where we normally have to specify the time to expiration measured in years. For example, a single trading day intra-week is 31.3% longer using my formula than the naive 1/365. In contrast, going from Friday to Monday my T value is 34.4% shorter than using the 3/365 formula.

Next, I go through the intra-day accounting. My assumption here is pretty simple: The time between the open (9:30 a.m. Eastern Time) and the close (1:00 p.m. Eastern Time) accounts for exactly 0.5 units with linear interpolation in between, implying that the close-to-open accounts to the other half of a trading day “unit”. (Side note: If I wanted to be really precise, I’d likely need to raise that value for the open-to-close to a bit above 0.5, because there’s more vol between the open and close than between the previous day’s close and the current day open. This is strange because most economic news comes out before the bell and a lot of earnings announcements come out after the bell. But in any case, 0.5 seems to do the trick all right for now. I will let you know if I ever tweak that number).

So, if I sell a Wednesday option on Monday at 1 hour before close, I account for this as 0.5*1.00/6.50 units for the intraday portion on Monday plus another 2 units for the M->W close. That’s 2.0769 units or 2.0769/278=0.0074709 years to be used in the standard options pricing formulas, e.g., from the options pricing Excel plugin in the awesome Whaley book (paid link).

What to make of those IB Delta figures now? I haven’t done any careful research yet as to why exactly the IB estimates are off by so much. Sometimes I compute a 3 Delta when IB quotes me a 2 Delta. What I found intriguing is that their Implied Volatility (IV) estimate is roughly the same as mine, while the Delta is very different. If they merely used a different T input, say, due to different accounting for the weekend and the intraday trading, we’d actually observe the opposite pattern: the IB estimate for IV would be very different but the Delta would be not that far off. So, there has to be another reason to account for the whacky IB Delta estimates. If anyone has any insights, please let me know!

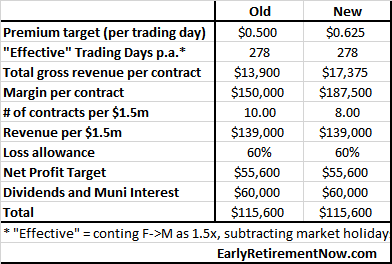

4: Less leverage, more Delta per option

Over the last few weeks and months, I’ve applied one more tweak to my options trading. I’m trading fewer puts but at a slightly higher risk level (Delta) than before. The overall option income and Delta should stay about the same but I’m just using fewer contracts and thus less leverage. The idea behind this is that I like to scale down the risk a little bit. Because the S&P has staged such an impressive run – up more than 100% since the pandemic low! – I like to reduce the risk per contract a bit. For example, previously I had budgeted around $150k in margin per contract. lowering the number of contracts by 20% and raising the margin per contract by 25% ($150k*1.25=$187,500) will leave the expected revenue the same, but with significantly lower tail risk. For example, if you assume a strike at 4,400 then your notional exposure of a short put is $440k (using the CBOE SPX index options with a 100x multiplier). With only $150k in margin cash that’s 2.93x leverage. I routinely ran that kind of leverage, even a bit more while still working. But now that the IB account is 30+% of our portfolio and I’m (for the most part) out of the workforce, I like to have less leverage.

What does that all mean for the strategy? Instead of targeting a $0.50 premium per day, i.e., $1.00 for the M->W and W->F trade and $0.75 for a trade over the weekend, I simply up that all by 25% in exchange for a 20% reduction of the number of contracts.

Of course, you don’t get to lower your risk for free. The fact that I’m still generating the same gross revenue with less leverage merely means that I am increasing my put strikes and thus I would get a higher probability of moderate losses in exchange for less severe tail risk. Seems like a good trade considering that I have to pay the bills from this account.

So much for today! Please leave your comments and suggestions below!

Please check out the Options Trading Landing Page for other parts of this series.

Title Picture credit: pixabay.com

Sorry for the newbie question, but when you say “margin cash” what do you mean exactly? Is it what IB calls “excess liquidity”? If not, how do you keep track of it? Thank you.

Good question. The total account value is what I post as margin. Most of that is held in securities (Preferreds, mutual funds, ETFs/CEFs). Some of it (<10%) I leave as just cash as a cushion.

Assuming an account with already some amount of leverage, would that be tantamount to Net Liquidation Value ?

Taking an example: with a total account value of 1.2M of which 400k are borrowed (box trade), would you consider 800k (NLV=1200-400) as the margin?

Thanks a lot

It sounds like in this example you have $800,000 and borrow another $400,000. You still have a net liquidation value of only $800,000 in that case. So, only $800,000 is marginable for your options trades.

Thanks a lot, that is exactly that.

To be 100% sure, is that 800k the same thing as what you call the margin per contract in the article (switching from 150k to 187.5k)?

No. $800k is the total account value. If you short 4 contracts, then you have $200k of equity per short put.

Probably a dumb question, but in your final chart, is that 10/8 contracts @ 100, or the same number of the mini’s @ 50 per?

Good question. This all refers to 100x contracts. If you use the ES 50x futures options you’d need 2x the contract numbers.

Having no idea how to put this into action, would you have any courses or tutorials on how to start doing that?

It would interest me a lot, since I’m taking a very conservative approach with my investments because I really think that the good days of the USA empire are behind us now.

Tutorial: My series! 🙂

There are some other sources out there but it’s hard to find the honest providers and avoid the scam artists.

is there a good resource to use in lieu of IBKR delta calculations?

MS Excel. Using the add-in from the Whaley book. 🙂

Hi Karsten – My success is little higher rate, this mostly because of luck. At random, I choose lower delta from time to time besides that your strategy works perfectly fine for me. I also want to thank you for exposing me to this strategy. I also paid a lot of bills out of this strategy and probably will for many years to come.

Nice! Market timing the level of risk you take in put selling is the Holy Grail. If you were smart (lucky?) in Feb 2020 and May 2021 you would have done spectacularly well with this strategy!

In May of 2021, I did very well.

Thank you again.

Karsten – thanks for posting your performance record for this year. I was wondering if this year was normal as I haven’t had many losses since I started trading your method in Dec 2020.

It’s abnormal because the market has been holding up so well. There were no major meltdowns like in Feb 2018. Don’t get too confident! 🙂

Thanks Karsten agreed!

Keep the masses happy with the safe withdrawal series when we all know the real gold is this series! Thanks for posting and updating us on how the put writing is going. You inspired me to do it myself and although I’m using a different strategy (tastytrade: -.2 delta, 45-30 DTE, on SPY/SPX), because I don’t understand yours fully, its going very well indeed.

Thanks John! I never understood the 45-30 DTE, but I’m glad that’s working out well for you. 🙂

Thanks for this post, I was the one who asked regarding the IB calculation of delta in one of the previous post.

I really think you should reconsider this strategy if this is part of your investment strategy for retirement.

I ran the backtest using CBOE SPX options data all the way from 2005 to present and this 2-3 DTE short put premium strategy has significant SKEW and Kurtosis risk, this is essentially the infamous Taleb’s distribution on display.

Especially at delta above 4, you suffer significantly because of the heavy Kurtosis because of your leverage.

This can work for a long long time, but you will eventually be wiped out.

e.g. I can pinpoint exactly where you / this strategy suffered significant losses.

January 22nd, 2010

August 5th, 8th, and 19th of 2011

August 21st 2015

March 23rd, 2018

December 7th, 2018

February 28th, 2020

June 12th, 2020

May 12th, 2021

You are playing with fire with this 2-3 DTE leveraged short premium play.

Hi John – Thanks well intentioned comment but I have been trading this strategy and from time to time go to lower delta’s (just because), but I know that I didn’t suffer any losses on June 12th 2020 or May 12th, 2021.

Isn’t any option strategy “playing with fire”? I think, the answer is obvious: yes – no matter how one slices a pie. That’s said aren’t we just providing potential liquidity for the market?

Just a thought and didn’t want to be rude or anything like that. Don’t eventually all options strategy fail? I think, the answer is also yes but timing differences could be few decades.

You might have not suffered losses, but I’m sure you ran pretty close to hitting your strikes on June 12th 2020 and May 12th, 2021. I assume I was correct in the other dates.

I don’t think it’s correct to say that all options strategy fail.

SPY collar is very effective for generating good risk-adjusted returns without significant Skew / Kurtosis risk.

Using this strategy for retirement is a setting up yourself for disaster, please at least disclose the Kurtosis risk to your readers.

This strategy has heavy heavy Kurtosis.

John – You are correct I did came close. I definitely read more to get educated.

Disclosure – I was not aware of Kurtosis risk.

It is nice to have. A blog where we can have friendly discussion.

I’m actually surprised you didn’t run into losses, but my guess is that you probably sold super super deep OTM puts, e.g. 1-2 delta. Especially June 12th 2020 since we were still in the COVID panic phase of the market.

Anything above 4 delta is setting up for significant losses (possibly ruin) with this strategy.

Whew, I used Deltas between 2 and 4 (according my calculation, not IB). 🙂

John learned a new term in stats class and now warns everybody about kurtosis. I have a more relaxed attitude toward kurtosis, see my replies. 🙂

Yeah, all good points.

Though, I don’t think that “all options strategies fail”

In fact, the insurance business is one of the oldest and most profitable businesses ever.

And I had a 20% IRR running my strategy since 2011, despite the (limited) losses on those days and a few more.

Maybe you were just looking at higher delta puts but on Aug 3rd vix was elevated 23 so you could’ve likely sold 2-4 delta puts for 50+ points away and only lost a little bit of premium on 8/5/11, Vix remained 30+ in Aug so you wouldn’t have lost any premium on 8/8/11 and 8/19/11.

Also, I’ve been running this strategy similar to this since 2018 and only lost a little bit of premium in 2018 (but still beat S&P 500). I only lost 1 month of premium in Feb/Mar 2020 and only lost a couple of weeks of premium in the last 19 months.

I think a key point is that the strategy is not a fixed delta. The losses will occur with rapid drops from low volatility, but generally the VIX goes up prior to big drops, which allows for lowering delta (i.e., risk).

John – You might be right, but I’m willing to put my faith in Big ERN with his background.

I’m certainly being lulled into thinking this approach is too good, since only given back 18% of premiums in the last 16 months. Some of that was greed and pushing too high on delta.

Well, even with a fixed Delta. spintwig has run (reliable!) simulations with a fixed Delta and showed that this is legit.

All in all, I know you already posted about the negative skewness of this strategy, but I think it’s a disservice to your readers to not disclose the Kurtosis risk.

This strategy has no effective hedge, since you are already selling the cheapest insurance possible. You are essentially at maximum Kurtosis risk.

This 2-3 DTE short premium has the illusion of high Sharpe and good returns, but you are guaranteed ruin running this for a long time (e.g. for retirement)

I found no effective strategy to beat the market in my backtests without significant Skew / Kurtosis, so I really think buy-and-hold is still the best strategy for retirement.

At least you should go out further in DTE and use VIX calls to hedge, but might as well just buy and hold and save yourself the time (and risk of ruin!).

For retirement, the best risk-adjusted returns (Sharpe) with lowest Skew / Kurtosis is long SPY with a collar (short OTM calls, buy OTM puts), which happens to be the strategy many Wall Street funds already run (probably for a good reason!)

All short-vol options strategies have kurtosis risk.

The skewness and excess kurtosis of my monthly returns is actually only slightly worse S&P500. My quarterly Skew and kurt are better than the S&P.

But I’m glad you can put you Statstics 101 knowledge to good use. Maybe one day you’ll know enough statistics and math to grasp the Central Limit Theorem. 😉

My last post on this. In my backtest, I ran many simulations of this strategy from 2005-present and here are the actual risk numbers:

For general low delta (e.g. 4-8):

Number of samples (n): 2130

Skew: -0.600274

Excess Kurtosis: 1.459394

Don’t try this strategy with anything above 8 delta, you will definitely get blown up for sure.

Better yet, don’t use this strategy at all, good old buy-and-hold has better returns and lower risk of ruin.

Excess kurtosis of 1.45 is nothing. It’s trivial. Skewness of -0.60 is trivial. What’s your point then?

This is a red herring. I ran my own little backtests to include the 2008 crisis and this strategy would have done really well. That’s because the build-up in IV was gradual enough and around the big market moves you had already sold at strikes way out of the money. Also worked spectacularly well in March 2020, with not a single loss, despite 10% market moves.

In fact, people with the 45 DTE strategies should be more concerned about skewness and kurtosis.

What people don’t understand is that skewness and kurtosis go away when you average over enough independent trials (Central Limit Theorem). All you need to do is to make sure that one single 2-3 DTE trade cannot wipe you out. In my case, I limit the max loss to 15%, when measured by historical worst-case scenarios.

Options newbie here with a basic question – why not roll the options down and out a few days (or even week) to avoid the loss?

Bad idea. See part 4 https://earlyretirementnow.com/2020/06/10/passive-income-through-option-writing-part-4/

Section “Why not just keep selling puts at the last strike at which you lost money?”

So, if your puts end up in the money, do you just let them cash-settle and sell new 3.5 delta, 2-day puts? Essentially rolling down, but not necessarily cost-neutral at the time of roll?

I suffer a loss, cash-settle and issue a new put with a much lower strike.

You NEVER want to double down on your past losses and keep writing puts at the last loss!

Got it! In these scenarios where you take a loss, do you ever sell new puts at a higher delta or for a higher premium than usual (to try to make some of the loss back!)? Or, do you stick to $1.25 or so in premium regardless of the situation?

Usually when you take a loss with this strategy, IV is jumping. So even if you sold at the same delta for the next expiration date you would receive elevated premia. I believe BigERN has said he sticks to the same premium at a lower delta when this happens because he is optimizing for income in retirement. I stick to the same delta and a higher premium since I am optimizing for portfolio growth in accumulation.

I found early on using this strategy in mid 2020 I wanted to go higher delta when VIX was low or when I took a loss because I have a bit of a gambler mentality. Other people who are more risk-averse have mentioned closing contracts early when the market moves sharply or pulling back in the aftermath of a loss. For an active strategy like this, it was helpful to me to write out your rules to modulate suboptimal behavior.

Question to you and BigERN: why not sell put credit spreads instead of naked puts? Margin requirements are a lot lower, max loss is much lower and you can afford to sell at higher deltas? You can still get same/higher premium too.

I do credit spreads also but I think naked puts is the way to go over long term.

Premium is lower for spreads at the same delta (unless your spread is so wide that it’s effectively naked). So to compensate, have to go to higher delta. Which means there’s higher likelihood that you have a loss. I’ve found that typically the expected return on spreads is negative. Meaning (win probability * premium) – (loss probability * spread width) is negative.

On the other hand, credit spreads are great for getting started (like me). Can start trading with just $500 and loses will be limited to the spread. I would recommend starting with spreads on SPX instead of naked puts on XSP.

Good point. Credit spreads are easier to handle with smaller margin amount. Also, IB allows you to trade the spreads in one single transaction. No change in the commission, but you might have a lower combined B/A spread.

Yeah I agree with Jsand below. naked SPX puts > SPX put credit spreads > naked XSP puts. The static margin requirement is great though and allows safer use of higher notional leverage than the same amount of notional leverage using naked puts. But you are paying for it.

Thank you JSAND and SCHMELJONES! I agree with you on trade-offs. Selling naked <5 delta puts gives you so little in premium compared to the notional value. In order to make the premium meaningful, you have to sell more SPX contracts, which increases notional value even higher! Yes, your short strike could be more than 1% away from SPX, but a bad day can go past that easily. Higher strikes in spreads do increase the probability of them finishing ITM, but your max potential loss is limited as well.

Do you know of any studies comparing selling 2DTE naked puts vs put verticals?

Depends. In early 2020 I was recovering form a medium-size loss (Feb 24) and the premiums got so rich in March that I took a bit of extra risk. Seemed like a worthwhile risk to take at the time. Could have also backfired but if I can sell at a really rich premium 20% OTM vs. my “normal” premium at 30% OTM, I’d still go for the extra $$$. 🙂

ERN,

Unlike in the SWR series, where I feel I’ve gotten close to expert status thanks to reading your posts, I’m a total neophyte on options trading, and in fact do none of it.

You mention tail risk repeatedly, and like probably most of your readers I’ve read and mostly understand The Black Swan and tail-risk.

Can you explain as simply as possibly how your option strategy is not in fact just another “picking up pennies in front of a steamroller” strategy, albeit with lower risk of being flattened than most other such strategies?

In the absolute worst case, how much of your 30.6% options trading bucket could you lose? More than 100% of it? And then same question for the near-worst case you can conceive of.

Thx

This strategy is literally just picking up pennies in front of a steamroller, nothing more.

From my backtests, this 2-3 DTE leveraged short premium would have thrived during the 2008 recession with an initial drawdown, but there are many pockets of instances between 2005-present where relatively modest market pullback caused significant losses to the portfolio. No weeklies before 2010, but you can interpolate / fit a model to what the 2-3 DTE implied volatility (therefore the options / strike prices) would have been.

It’s a different risk profile giving the illusion of high Sharpe and good returns, but you run very high Skewness / Kurtosis risk, exacerbated by the leverage required to get any kind of returns.

And worst of all, there is no effective hedging possible with this strategy. You already sold the cheapest insurance possible, there is nothing else you can do to protect your downside (e.g. no cheaper re-insurance to buy).

Many other options strategy have hedges available. None of that is possible here (cheaply anyways).

This is the cousin of wallstreetbets’ approach to investment. WSB loves bets that consistently lose, but pays out significantly once in a blue moon. This 2-3 DTE leveraged short premium strategy loves bets that consistently win, but will blow up once in a blue moon.

Both are not good investment strategies.

Buy and hold will beat both in the long run with better risk adjusted returns + lower Skewness / Kurtosis.

John: Comparing my strategy to Wallstreetbets shows that you have no clue.

You should just stop making a fool out of yourself. Sounds like the “old man yelling at clouds” meme, throwing around big words like kurtosis and hedging.

Your other comments, where you breathlessly announce an excess kurtosis of, gasp, 1.45 (not really high at all!!), show that you should just let the adults talk here.

John, it’s not correct to say that there are no hedges available after you sold the puts. There are always choices. For example, if SPX falls a certain amount, you could buy VIX futures or VIX calls. Or, have a conditional stop sell order on ES. Or a low-cost unbalanced put butterfly. There are always choices!!

I calibrate my strategy so that in a repeat of the historical worst-case scenario I’d lose no more than 15%. And that’s 15% of the IB portfolio, so around 5% overall. Not a 15%/30%=50% loss!

But you’re right: it’s a picking up pennies in front of the steamroller.

But ask yourself: why do you get an equity risk premium? To take on the upside or downside risk? It’s the downside that earns you the premium. Selling puts captures that in a purer form.

Thx for the explanation. I’d be curious if the historical worst case included the flash crash and Black Monday 1987. Seems to me if the loss is as low as you say even in those two cases, then you’ve for all essential purposes eliminated the risk of ruin, which would be pretty impressive.

The loss of ruin is an issue when you run this with too much leverage. Black Monday would not have been too much of an issue because you would have likely sold puts far OTM for that Monday already (implied vol was already very high the Friday before Black Monday).

If you had limited yourself to only 2.0-2.5x leverage you might have lost less than the S&P on Black Monday.

Again, thanks for the reg update and deep analysis. As I get closer to a retirement, one thing I am looking for are 1) cost effective leverage 2) low operation overheard 3) low fee.

I am planning to hold 75/25 eq/fixed income mix. Recently I started reading about NTSX ( Wisdom Tree ETF).

I would love you hear you view on this ETF (or similar strategy of holding 90% equity with 50% leverage via Fututure)

also wouldn’t this be more tax efficient? Since Futures has better LTCG tax treatment (for 60%) vs. straight bond etf?

I like the idea. I have written about the general concept in this post:

https://earlyretirementnow.com/2016/07/20/lower-risk-through-leverage/

Thanks Big Ern for feeding my options writing addiction! I have been using your SPX short selling strategy for 2 1/2 years now and it is my favorite part of investing. I also have about 30% of my entire net worth in my options trading account, so this is not just a hobby. I retired about four years ago at 49 and have found this to be a very tax efficient method of generating income in retirement.

I think it is very interesting that you have chosen to reduce the number of options you sell from 10 to 8. I had used similar reasoning when I reduced my options from 8 to 6, and I felt a slight amount of satisfaction to see that my brain could come up with a similar idea as your brain. That was a first for me!

Wow, good timing! It’s reassuring that two smart people come to the same conclusion independently! 🙂

Are you now selecting your strikes strictly based on premium collected instead of delta? I thought you used to do 5 delta regardless of how much premium that would get you?

What delta have you been averaging with this new change in strategy? 7 delta?

I’m using a combination of multiple criteria. See Part 4: https://earlyretirementnow.com/2020/06/10/passive-income-through-option-writing-part-4/

Section “What strikes do I target?”

Currently I’m at around 3.5 Delta, About $1.25 premium for a 2-day window.

Given that option writing has only slightly trailed the SP500 (but with less volatility), would the recommendation for people early in their accumulation stage still be to just bypass option writing and stick with equities?

That is a great question! I love Put writing, but in accumulation phase the taxes are a bit of a hit.

Gains in 22% bracket end up being reduced by 17.8% (60%*15% + 40%*22%).

In retirement and stay in 15% bracket, gains are only reduced by 4.8%(60%*0% + 40%*12%).

Am I missing something?

Well, the tax drag can be overcome with more leverage (to a degree). But I still think it’s easier to just stick with equities. Volatility is not that dangerous when you’re still accumulating.

Why not both? Buy and hold equity index funds with monthly contributions and sell SPX puts on margin? I actually am doing this early in accumulation with 4-5D put spreads to achieve fairly high notional leverage while still being protected from wipeout against >30% drops.

There are some hidden tax benefits to this approach during accumulation:

1.) you can tax loss harvest your equities to offset ordinary income

2.) Another tax possibility is to use SPX box spreads for short-term borrowing as it is considered a Section 1256 loss. I’m still experimenting with this – I had a 0% APR credit card balance of 5K coming due a few months ago. Rather than paying it off with cash I put the cash in my IBKR account I sold a 180DTE 5K box spread for $4,968.99 for a nominal interest rate of 1.29% but an effective rate of 0.94%. I think you can get better rates if you increase the DTE, spread width, and are more patient for fills. Of course when it comes “due” you either need to have cash on hand, run a negative margin cash balance, or “roll” the spread out making this a floating rate loan. I’ll be testing this out with buying a 2nd car for my family in a couple months and targeting a Dec 23 spread.

Just saw your comment on selling put spreads. What deltas do you usually do on the short/long sides? How many days in advance do you typically sell them? Do you manage the positions or let them expire?

4-5D on the short side, never more than 2 DTE and the long side is determined by my margin requirement to always have >25% of your account value in excess liquidity after opening up a credit spread. Since the put credit spreads are defined risk trades that contribute statically to margin requirements you really only have to manage that excess liquidity number as a function of your margin assets – I have half equities/half fixed incomes and a decent cash cushion so this approach should be robust to 25% (or more?) drops over 2 days in the SPX.

The >25% number is handy for efficient use of margin for small, single contract RegT accounts because you can double up and open a new contract a few minutes before the end of the trading day if you know your other contract will expire safely.

I always let them expire whether ITM or OTM – commission drag for spreads is 2x higher than naked puts and you don’t want to make that 4x. You are already getting hammered paying for the downside protection. I’m planning to move away from put spreads for those reasons once I’m up to 2 contracts and/or off RegT to Portfolio Margin.

I certainly do both, but works better in ER with lower tax rates.

Love the box spread loan concept, and I sold a few on SPX in July for 98.0 on December 2023. I calculate about 0.85% loan rate. Interest just comes off my 1256 gains.

@Schmeljones – do you use equity index funds for margin? Doesn’t that add more risk? BigERN specifically uses muni and preferred shares because they are not that closely correlated against SP500.

Also on tax loss harvesting, does put writing help in any way? Or are you saying you have the option to do tax loss harvesting since you have index funds.

Yes it does add more risk! I’m not saying this approach isn’t volatile but it works for me as a superior alternative to generating early career leverage for “Lifecycle Investing” vs other options e.g. LEAP calls, ES futures, the so called “Hedgefundie” portfolio…

Put writing doesn’t help with TLH. I just couldn’t decide whether to do buy/hold/TLH or sell puts a lá BigERN with the currently small fraction of my portfolio in non tax-deferred accounts. So I did both.

OK, more power to you. The advantage of your strategy is that you’ll start FIRE with a large pot of money in a taxable account with a high cost basis. Not a bad retirement strategy!

You’ll actually get better rates on lower DTEs (i.e. short term loan vs long term loan). You did pretty well, but check out https://www.boxtrades.com/ if you’re interested in the best current rates others are getting for their box spreads

Yes, especially early in the accumulation phase you’d be better off with equities.

Can it be argued that this strategy exposes you to a different risk premium than equities (cf. your computation of alpha)

Hence it would be desirable from a diversification perspective to be exposed to both? (with leverage as an overlay to achieve the targeted level of risk)

The premium is called the volatility premium. The two are correlated, of course.

Thanks

How would you qualify the level of correlation?

When you perform the regression analysis on SPX and other factor levels, it seems that the Beta is super low (though statistically significant). Is that tantamount to saying that the level of correlation between the two premiums is low?

The beta is related to the correlation:

beta = rho x sigma_strategy / sigma_SPX

The beta is low because the rho (correlation) and the strategy volatility are low.

Thanks a lot

Spintwigs backtest in part 5 (https://earlyretirementnow.com/2020/06/17/passive-income-through-option-writing-part-5/) shows you can beat buy and hold at 2x leverage and higher. Although I remember he commented on his blog more recently that he is stopping options trading in favor of buy and hold since newer backtests show that’s better. Not sure how to reconcile that.

My plan is to allocate a fixed percentage of portfolio to this. Then quarterly, rebalance the excess (if any) into index funds. This way, I “lock in” some of the profits.

In retirement I care more about the risk-adjusted return not just the average return.

I got back into it around Feb/Mar this year and have been selling same-day (0 DTE) SPX puts from time to time.

Thoughts on 2/3 delta short calls using same expirations ?

My understanding: the premium on calls are lower compared to the puts for the same delta. So better off just doing the puts. I looked into iron condors – basically calls and puts using the same margin. But that increases your overall risk. And one side of the option legs is in danger whether the market goes up or down. But if you do put only, can rest easy once you see that the market is trending upwards.

Agree!

It is my understanding that iron condors are great play for brokers, not investors. Placing an iron condor generates generous fees while also causing the investor to buy the most expensive part of the vol smile.

Yeah, agree. The commissions and B/A spreads and then potentially closing trades are very costly. Not an attractive long-term strategy!

This is precisely the case. It’s a coupon business. Brokers don’t want their clients going broke. They want them to stay trading as long and as frequently as possible. Short of ridiculous position sizing, ICs yield some of the lest volatile P/L.

https://spintwig.com/retail-broker-business-model/

Nice link. All good points!

Totally agree. I sold exactly one 0DTE iron condor this past summer to experiment and of course we had one of these late day rallies right before market close. Nothing worse than watching the SPX Friday at 12:57 knowing each point it ticks UP you’re out a hundred bucks!

Ouch! That’s why I don’t like selling the upside. And I know, I make a lot more money on my index funds than I’d lose on the call legs of the Iron Condor, but still a very unpleasant thought.

Very lean premiums. And I don’t like to bet against the US stock market. I’d feel unpatriotic. 🙂

Thanks for yet another great update.

I am curious about your same day trades, are there any parameters you use to decide to enter or not enter? Gamma seems so high with the shortest possible expiration that I am curious how you weigh the risk to reward. Thanks!

Mostly by feeling. I check if I can sell contracts at $0.50 to $0.75 premium far enough out of the money.

I’ve been using a covered call version of this strategy and it has worked quite well. Obviously this departs from the goals of the specific strategy detailed here but with the far OTM calls I’m pretty confident it will add a couple of CAGR to the bottom line. Thus far I’ve been called 2x with minimal damage. Generally the market doesn’t melt up, but as noted the premium isn’t as rich either.

I AM a bit disappointed I can’t use my IB phone app while skiing now…seriously BigERN, that was some bummer news. 😉

OK, good for you. I’ve been dabbling with covered calls on individual stocks with a very underwhelming success. So, I’ll likely stick with my short put strategy.

Oh, really? Well, I use the IB app in the lift only. Not while skiing. But I might try it on a green slope sometime. 😉

I think that’s a wise choice to cut the # of puts in retirement. It might lead to a little more volatility but you’ll likely have smaller max draw-downs which is what’s more important to control for in retirement.

Right. It’s more frequent but less severe drawdowns. A better fit in retirement! 🙂

While I love this kind strategy while working, I do think I’m going to cut back on my option selling portfolio in retirement since I don’t think I can stomach a 1987 scenario personally.

I think I’m going to use most of my option selling portfolio for a final mortgage payoff just before retirement since nearly all the gains are already realized, it wouldn’t trigger the tax hit that selling my equities would.

Also, it would probably be better for me to cut back on options selling to reduce my AGI for some big tax credits like ACA subsidies.

That’s roughly what I did. I started with 5x leverage. Then scaled down to 3x and now I’m at 2.2-2.5x.

But I also agree with the slight tax-inefficiency. It’s something to consider when in retirement. We don’t have an ACA plan, so this doesn’t matter to us.

ERN, what deltas and premium levels are you targeting now?

Premium target about $1.10 to $1.25 for a 2DTE option (e.g. Mon-Wed). Right now that’s a Delta of about 4.

To answer your question about IB’s wacky quotes: IB is fairly transparent about how they expect you to pay for up-to-the-minute quotes & data before each trade, or else take a chance with stale information (maybe in some fields more than others). It is their business model for making money without charging commission and while charging only 1.58% for margin loans.

The arbitrage opportunity for cheapskates like me is to do my analysis in one brokerage and my trades in the other.

I’m not sure this is actually the issue at hand – I have real-time quotes for options and US securities though IBKR and still see deltas lower than what I’d expect especially for 1

Incidentally, IBKR offers fee waivers for each month you generate commision revenue more than $20 (for options) or $30 (for US security bundle). I run this strategy on a 1 contract size account but I pay my fees out of a IBKR Friends and Family account where I manage the put selling account and 3 other accounts for family members. All accounts count towards the commission revenue.

https://www.interactivebrokers.com/en/index.php?f=14193

Meant to say “especially for 1 DTE or less options”

Agree. The quotes aren’t the problem. The Delta computation is whacky.

Hi there, what would be the best way to get around this? check the delta on a separate platform/website?

Yes, that works. I calculate the Delta myself in my own spreadsheet.

The quotes aren’t whacky. Only the Delta calculations are.

For the options trading, you do need to use the IB real-time data (for a very nominal monthly fee). Don’t trade puts on stale quotes!!!

I’ve had IB for 10 years and another brokerage with real-time options quotes for 20 years. I haven’t made a trade in that other account ever since I opened IB, but I login everyday. It’s annoying to switch apps when making a trade but it saves money!

I don’t RT quotes only for the SPX options not for the preferreds, ETFs, CEFs. So, I piggy-bank off of the Fidelity account. Cumbersome, but I don’t that stuff very much. 🙂

I’ve been experimenting with your approach for the past two months. September meant an opportunity to see immediately how the relevant strikes “magically” drop away from the underlying during volatility!

I couldn’t resist making my own version of one of your graphs: https://ibb.co/XyLVy7Y. (Not sure if the link will be allowed.)

Nice! That’s a great chart, thanks for sharing . (up to 2 external links are allowed here, by the way).

But always keep in mind that the last few months were extremely calm. Don’t extrapolate and don’t take too much risk There will be another Spring 2020 in our future. 😉

I was wondering about your “weekend = 1.5 trading days” rule, and did the following calculation which seems to exactly support it.

Looking at SPX closes back to 1978, the variance of log returns for closes separated by 24 hours (e.g Monday-Tuesday) is 0.000111962, while the variance of log returns for Friday-Monday closes is 0.000175086. These are variances, not volatilities, but it’s exactly the variance that tells you the clock speed for Wiener processes (i.e. what we want as the input for Black-Scholes pricing). The ratio of these variances is 1.5638, very close to your rule!

Interesting finding TQFT!

Did you happen to look at the ratios of weekdays to another and/or holidays?

I’d guess Tu-Wed close to close has the most variance due to mid week events like elections and Fed meetings.

Here are the somewhat curious results (this time using the SPX since the beginning of 2008), normalized so the overall variance in daily (open-to-close) returns is 1.0.

Monday trading hours: 1.22667

Monday overnight: 0.102223

Tuesday trading hours: 1.03037

Tuesday overnight: 0.0886995

Wednesday trading hours: 0.950552

Wednesday overnight: 0.0800372

Thursday trading hours: 1.08869

Thursday overnight: 0.0976724

Friday trading hours: 0.718897

Weekend (Friday close to Monday open): 0.198465

In summary: Monday is 20% “faster” than average, while Friday is 30% “slower” than average. Tuesdays and Thursdays are slightly fast, Wednesday is slightly slow. Overnight is about 10% of the “time” of a trading day, and the weekend is about 20%.

It would be fun to see how this holds up on other indices / stocks.

I’m amazed by how slow the overnights are, especially given a lot of news is available before the open.

DJIA is rather similar: 1.22, 1.01, 0.93, 1.07, 0.77 for the weekdays, 0.11, 0.09, 0.08, 0.08 for the overnights, and 0.25 for the weekend.

However when you look at individual stocks it’s all over the place:

GM: 0.79, 1.01, 1.18, 1.14, 0.84 for the weekdays, 0.53, 0.74, 0.65, 0.48 overnights, 0.81 for the weekend.

MSFT: 1.04, 1.02, 0.99, 0.90, 1.03 weekdays, 0.41, 0.36, 0.42, 0.99(!) overnights, 0.62 weekend.

The 1.5 rule for Friday-Monday close is remarkably robust, however!

Individual stock variance likely has to do with earnings. GM usually has theirs on Tuesday or Wednesday after the close whereas MSFT releases on Monday or Tuesday as of recently.

Agree.

Earnings dates clearly make this strategy harder for individual stocks. You’d probably have to factor in a 2x or 3x or whatever x when you have an earnings nnouncement.

See some Tuesday SPX options on Ameritrade for next two weeks. Interesting.

Nice!

Tuesday options are online. Thursday options start in May, earlier than initially anticipated!

https://ir.cboe.com/news-and-events/2022/04-13-2022/cboe-add-tuesday-and-thursday-expirations-spx-weeklys-options

Exactly! Thanks for confirming roughly the same calculation I did a while ago. 🙂

One crazy thing that I see more and more FIREs doing and recommending is to invest 100% in the JEPI ETF. It follows the S&P500 so you get appreciation while also using the options write strategy you explained above to generate a juicy 7% yield paid monthly. You have income and cap gains = total return, all that for only 0.35% ER

I’d need only 600k invested in it to get 3k+ a month (more than enough for me) …what do you think of this strategy? is it sound?

Also, don’t forget that a lot of this “yield” is in the form of liquidating capital. It’s not as good as it seems!

That fund seems like a lot of the buy write call funds. They can do well in “sideways” markets but can underperform in bull markets or volatile markets which can often be the case.

Since that fund just started after the covid stock market crash we don’t know how it would’ve performed but some of those strategies have similar downside risk as index funds but didn’t bounce back as quickly after crashes since they are selling upside calls giving up gains as stocks bounced back.

A 0.35% ER isn’t trivial either, for someone on a 3.5% SWR that could mean they must have a 10% larger portfolio to cover that investment expense each year

Yup! 0.35% expense ratio seems expensive for a relatively low-maintenance fund!

I really like the JEPI strategy. Especially if you have no idea what big ERN wrote above in his post like me, and have no intention of learning and wants to be as far away as possible of this insane derivative market

0.35% in a million dollar portfolio is a lot of money. Enough money to for most people to DIY. 🙂

Also if you don’t understand the strategy, you probably shouldn’t invest in it either or you could risk ending up in something like UVXY that blows up someday. Just stick to boring simple index funds instead.

Good point! 🙂

Hi Karsten, I just read that SPX option trading times will be expanded close to 24 hours on 21th of november. Do you think the strategy will still work after that?

Cheers!

I would trade SPX options only during NYSE market hours: 9:30am to 4:00pm Eastern Time. Beyond that there is very little liquidity.

The expansion of trading hours will have no impact on the attractiveness of the short-vol risk factor.

Thanks for the continued series, BigERN! I’ve been following the fixed 5-delta strategy since March 2020 and have around an 8% annualized return on capital so far. I took bigger losses than you on May 12 (around 3 months of premium income) and a smaller loss after this was published, on Nov 26 (half a month of income). I have a couple questions about your mechanics:

1) Do you literally let your positions expire and then open new ones first thing in the morning, or do you close your positions near the end of the day? I’ve found that at the end of the day my open positions are often closable for $0.05-$0.1 plus commissions, but waiting until the next morning results in greater than a 5 cent drop in 5-delta premiums. I’ve been setting 5 cent GTC closing orders as soon as I open a position, and opening the next expiration whenever they fill. This can result in ~2.5 DTE positions sometimes, if the market jumps a lot during the first few hours of the day. On the other hand, when my options expire at a loss I often cannot enter the market until the next morning, because the cash settlement and return of my committed margin doesn’t occur until overnight. At the end of the day on Nov 26, Nov 29 5 delta expirations were selling for ~$2.50 in premium. However, since I had to wait for my losing positions to expire, I couldn’t open these new positions, and at market open on Nov 29 5-delta was only worth $1.00. I’m curious how you handle these situations.

2) In comments above you mention “calibrating” for a 15% loss in the event of a worst-case historical event. Do you actually set a stop loss? It seems to me like the most well-known worst-case scenario is a 20% drop in SPX. A 3 delta 2 DTE put at 15% IV is currently about $100 OTM. With SPX at 4700, this would mean a worst-case day would leave you with a loss of $84,000 per contract. Are you saying that loss (multiplied by your number of contracts) is 15% of your put-writing strategy assets (=$5.6M in assets for 10 contracts), or do you have an earlier stop loss set?

One other question – it seems like you base your number of contracts on “notional exposure” instead of actual margin requirements. I know you’ve mentioned in the past you are on portfolio margin, but normal RegT margin for these contracts is typically the “20% of underlying minus OTM amount”. During quiet times, this is currently about $80k in margin requirements per contract. At more volatile times the margin requirements actually _decrease_, because the OTM amount grows. For example if IV tripled, current margin requirements for 5 delta contracts would decrease to around $70k, suggesting you could sell more contracts in high IV times for the same amount of margin usage. Do you care about your real margin usage at all, or are you simply looking at your “notional exposure” (underlying at $0) and making sure that equals 2-3x your available assets?

I don’t really care about the margin usage. Never came even close to the constraint.

As I stated before, I calibrate my # of contracts using the notional only, not the margin requirement.

I’ve been doing the same with a $0.05 – $0.10 GTC order right after I open a position. Most trades since May closed way before expiration. Usually has to be $0.10 to get the fill. Looking back through my trades since May the early close never prevented any losses. However the 5D strike for close on Nov 29 for Dec 1 expiration was 4510, and SPX closed at 4513, so crazy close but no loss. I could have closed the trade earlier in the day for $0.10. I took losses on May 12 and Nov 26 also. What was your strike expiring on Nov 26? I was at 4630 which was the 5D strike 5 mins to close on Nov 24. 35% loss.

On Nov 26 I was at 4605. ~2 min before close this was at scratch and it wound up closing for a huge loss. This is really annoying because then your margin is not released until the next morning.

Another nail-biter day was Sep 20. I had. 4330 strike. This didn’t close until less than a half hour before market close. Luckily with the 5-10c GTC such things can close a minute or two before the bell and you can still trade for the next expiration in the next 15 minutes. It’s only when you need to cash settle for a loss that things become annoying, particularly if SPX gaps up overnight and vol (and premiums) decrease.

I was pretty safe:

8 puts:

4250

4250

4275

4275

4300

4300

4225

4225

Low was 4,305.91, close at 4,357.73. Whew! A nail biter indeed! 🙂

What’s making you have different strikes at all? Do you purposefully spread out your sales throughout the day, or purposefully spread out your strikes, or maybe only sell one contract at a time? My methodology is to put in a sell order for N contracts immediately after my others close/expire. Do you sell yours all at once, or what else is going on here?

Different times and different SPX levels at those times.

Are you intentionally spreading the contracts out over time for some kind of diversity or is there some other reason you sell then at different times?

Both. If over the course of the day the same strike yields my revenue target I will sell puts at the strike. 😉

My strikes:

4560

4560

4575

4575

4565

4565

4570

4570

4610

4610

The last two were actually extras that I sold “just for fun” after I had already written my target 8 puts. But since the earlier ones on Wednesday had already lost most of their value I thought I write two more. Never expected such a meltdown on the normally quiet trading day after Thanksgiving.

What time did you write these on Wednesday? Yeah I almost wrote more contracts than usual since the day after Thanksgiving has always been mild.

8:13:08

8:13:08

8:33:24

8:33:24

11:12:41

11:12:41

11:12:45

11:12:45

12:30:35pm

12:30:35pm

All times are PST.

1: I never faced any margin constraints like that. Are you using portfolio margin?

2: That calibration is just that. My personal calibration, no stop-loss order.

The 15% loss “target” refers to my account value

I’m unclear on how the math for this calibration adds up with your leverage ratio. A single contract has notional exposure of ~$430,000 currently. The historical worst case performance is at least a ~20% drop. This would cause losses of around $70,000 per contract. To calibrate $70k to a 15% portfolio loss, you’d need to dedicate $466,666 per contract, right around 1x leverage. But you say you are using at least 2x leverage, meaning you have less than ~$215k per contract. A $70k per-contract loss seems like it will hit your portfolio by 30%+. What am I missing here? Are you considering that the worst-case historical performance is not -20% on SPX? If you are calibrating for a worst-case 10-12% drop in SPX then the numbers make a bit more sense.

Uhm, have you read this series? I’m not selling puts at the money. I write my puts out of the money. Sometimes way out of the money.

As a rule of thumb, if I’m using a 15% worst-case scenario, 2.5x leverage, that means I can suffer a loss of 15%/2.5=6% beyond my strike. Right now, I have most of my strikes at around 4000-4150. Make it 4100, weighted average. Another 6% below that is 3854. With the SPX at 4600 that’s a big drop. With today’s implied volatility that’s an unprecedented drop.

Now, granted, there have been times when the market dropped by 12% in one day (e.g. March 2020). But the VIX was also much higher than today’s.

Your strikes are further OTM than I expected since you are targeting a fixed premium instead of a fixed delta. It makes sense that your strikes are so far OTM right now since IV is spiking, but even just a month ago I would have expected them to be closer to the money. For example on Nov 3 I had 4485 for only $1.45 premium. Nov 5 I had 4500 also for $1.45. Nov 8 was 4610 and 4640, around $1 weighted average premium. All the way up through Nov 24 the rest looks similar, and SPX was from 4600-4700 the whole time. So those strikes are only $100-200 OTM.

Put another way, if we just look at Black Scholes numbers:

SPX at 4600

2 DTE (T = 2/365)

Risk-free rate=0

2.5x margin

IV at 15%: $1.30 premium @ strike ~4520. Margin = $180,800. 20% drop in SPX = $84k loss = 46% of margin.

IV at 30%: $1.30 premium @ strike ~4415. Margin = $176,600. 20% drop in SPX = $76.5k loss = 43% of margin

IV at 50%: $1.30 premium @ strike ~4270. Margin = $170,800. 20% drop in SPX = $59k loss = 34% of margin

Even with IV at 50%, if you want a worst-case drop to be 15% of margin, you can only withstand a ~$26k loss, which corresponds to a ~13% drop in SPX. I agree this is a big number, but it’s not “the historical worst case”.

More troubling is that when IV is low, it’s not unusual for a $1.30 premium to be only $100-200 out of the money, and then a 13% drop ($600 drop in our example) represents a $40k-$50k loss per contract. With IV at 30% you could only withstand a 10% drop in SPX for this 15% portfolio loss calibration, and IV is often lower than that.

I agree with your posts here that most of the time, IV is rising when these big losses occur. This means that the strikes are going further and further OTM and a big drop still results in only a small overall percentage portfolio loss. But I think that the point is there is still a significant tail risk. In the event of a black swan that is not preceded by a rise in VIX, you can much more than a 15% loss in your portfolio. Maybe you are just saying that this kind of unforetold black swan event doesn’t concern you?

Look, if you don’t feel comfortable, don’t trade this strategy.

But to calm everybody’s nerves, let’s consider this:

I’ve routinely sold put with an IV>100%. Your calculations with IV going to only 50% are laughable. Don’t confuse the VIX with the IV of an extreme OTM put. If the VIX is at 50% your IVs are at 100%+. I’ve had examples where the VIX was at 55% and I sold puts with IV>150%.

The most extreme example: On 3/16/2020, I traded the 3/18/2020 expiration. VIX was 82%. My short put had an IV of 176%. The strike was 29% OTM. If the market goes down by 20% I lose exactly zero.

With 2.5x leverage, I would have lost 15% if the market had dropped 29%+6%=35%. Over two days. Very unlikely.

And conversely, 20% drops don’t ever happen out of the blue. Even past black swan events: Lehman failure, 2020 pandemic come about very fast, but slow enough that the VIX and IV will build up slowly enough that we can react and by the time a 20% drop happens our IV is already high enough that we hopefully sell puts far enough OTM.

Dear sir,

If I am not wrong, you open a trade near the close of the day.

e.g. open on Late Monday for Wed expiry.

I come from half a world away (+8 GMT) so not quite possible to be up every 3 days (my 3-4am early morning) to open a trade. If I missed opening the trade on late Monday, does it still make sense to open on early Tues for Wed expiry?

Or do you have some solutions for traders from very different geographical locations.

Regards

Good point. I traded this strategy while residing in different time zones:

Europe: nice timing because the close is at around 10pm at night

Manila: brutal! Had to get up at 4am or or 5am or so to trade the close

Sydney and South Pacific (Vanuatu and New Caledonia): Nice! Closing time at around 8am.

Auckland: Nice! Closing time at around 10am

Another option would be to trade well before the close if you have the confidence that the current contracts will expire out of the money. So, you have another 6.5 hours before the close. That’s what I did most of the time in Manila

thanks for your kind answer 🙂

I’m very near Manila (Singapore to be exact)

Nice! Good tax climate there! I almost moved there once. 🙂

Hi again,

Say you open a trade on Monday for Wed expiry. Do you take profit if it hit 90% premium on Tuesday?

If yes, do you

(a) open another trade on Tues for Wed expiry?

(b) wait it out and continue to open a new one on Wed for Friday expiry?

I normally don’t close my trades even if they already made 90% of the profit already. But sometimes I would do another trade on Tuesday with the Wed expiration if the existing puts have really low deltas. 🙂

Hi BigERN, Any thoughts to share on this strategy in light of rising inflation? Do you expect risk/return profile to change? Does it become less appealing since real returns are lower? Or does it become more appealing because returns are still higher than alternative fixed income allocations? Curious on your wisdom here!

Yeah, good question. My hope is still that inflation will come down again before too long. 10-year CPI estimate from TIPS is 2.5%.

But if you’re making “only” 5% from the margin cash and maybe 5-10% from the put selling, that’s a bit lean when inflation is 7%.

I’m still hanging in.

Also: I’m using a lot of floating-rate preferreds, so if long-term inflation stays high and rates go up substantially, I’d capture some of the rate rise.

Hi BigERN, Can you tell us some about the preferred shares you’ve chosen? I looked at a few of them and they seemed to be fixed-to-floating and still in the fixed period. Won’t the bank buy them back at the call date rather than letting them go to floating? I’m not all that familiar with preferred shares so maybe I am missing something?

Due to that call options risk it’s wise to perform a “yield to worst” calculation, i.e., what;s the IRR if the share is called and you get $25 at the call date.

The call is not a foregone conclusion. I have/had several preferreds that were past the first call and paid the floating rate (BAC PRE, BML PRL, C PRN). Paying LIBOR+4% is actually cheap for most financial corporation. Cheaper than issuing actual equity. Obviously more expensive than issuing bonds, but preferreds give more flexibility.

For more info on these, check out this site: https://www.quantumonline.com/search.cfm?tickersymbol=WFC-R&sopt=symbol

When determining your overall portfolio asset allocation, should you not weight the options strategy factor results by 2.5x-3.0x? If it is 30.6% of your portfolio based on the IB account value, and this strategy is leveraged while other elements of your portfolio are not, doesn’t this strategy make up more like 52.4% of your portfolio’s risk exposure? Perhaps this is already taken into account because you are using levered returns as the dependent variable when finding the factors.

It’s 2.2x but with a delta of only 0.03. So, that would count as 6.6%. Multiply that by 0.306 and you got basically zero equity exposure.

But I don’t like that approach. Just because the initial Delta is so low, you do get much higher statistical betas because every once in a while your delta goes to 1.00=100% when the puts go in the money. I prefer my method.

Thanks. Good point. I hadn’t thought about incorporating the delta (makes sense but not easy to summarize because it is always changing, so your asset exposure is always changing).

On the low-risk bound, as your options are expiring OTM, I guess you have exposure of 30.6% bond/preferred mix, 54.1% stocks, 3.4% cash 11.9% real estate.

On the high-risk bound, as your options go in the money and approach 1 delta, you have exposure of 30.6% bond/preferred mix, 121.42% stocks, 3.4% cash 11.9% real estate. Sums to 167% so at that moment you are 1.67 levered across all your investments.

I appreciate the factor analysis as a way to summarize the typical exposure in a complex options world where portfolio exposure is shifting minute to minute.

I have really enjoyed reading this series. Thanks for writing it up.

I sold my first XSP 450 Put Monday afternoon expiring tomorrow @ 0.22 premium. I kept the leverage low b/c my margin cash is invested in intl/us equities rather than bonds. I only did 0.79 leverage by selling a single contract. I’m in the accumulation phase, so interested in this to a little leverage with less volatility than just buying more equities on margin (and w/o the borrowing cost). Also like the sideways potential. If I repeated for the year and got the same premium, I would boost my returns 1.97% at a 40% capture rate. Pretty cool and the learning has been fun. Next I need to figure out how to calculate my own deltas since you said the ones in IB are inaccurate and I don’t have that CD-Rom.

Yes, all good points. The high delta when everything is in the money comes up only very, very rarely. That’s why it doesn’t show up much in the factor model.

Also note that frequently after a large loss, the subsequent days are exceptionally profitable (I made a ton of money in March and April 2020).

Good luck on your put selling adventure!

Hi BigERN, Question about the calculation of calendar time section. You write “A Friday closing to Tuesday closing when Monday is a holiday and market holiday is still only 1.5/278.” but in the table below that paragraph it says Friday -> Tues Monday holiday 2.5/278. Is the 2.5 in the table a typo?

Good catch. Fixed the typo. Can’t imagine nobody else noticed that until now! 😉

Thanks a lot, AC!

Hi Karsten, thank your for your post and it is very helpful. I want to ask one question about my case.

I am doing a Phd program and it seems selling put every week is still is not good for me because it takes time. I wonder how about the 1.5X leverage for VTI under IBKR margin loan once every month. Is it a good option as well? I don’t expect to get better performance than selling put but higher return than the 1X index performance is enough for me.

I never spend much time on this. But I understand your concern. It takes away from your focus. 1.5x leverage on a simple stock fund seems like an easier way.

SPX options selling is better for old geezers like me in early retirement. 😉

Wow, this week was a real pain in the neck! I got pinched for the first time! Had to pay out about a month of premium, but it could have been much, much worse. I now have strikes at 4050 for Monday.

Got pinched on Friday little bit. Now got strikes at 4100-4250 for Monday. Very rich premium landscape now. Don’t despair, you’ll make the money back!

Of course! The house is on fire, and we’re selling fire insurance (:

After some bad luck earlier this month, this was my lucky day on Monday. I was out in the mountains without mobile phone reception in the morning. So, I missed the brief dip to under my 4250 and 4225 strikes. And made all the money I planned. Phew!

Hahaha you were ITM today as some point! The market gods are merciful.

Keep Calm and make the option premium! 🙂

T-shirt?

Would gladly buy and wear

Haha, I see a new line of business! 🙂

Yes! But in all seriousness now, this week demonstrated the power and versatility of this strategy-

Although I lost a month of premium in one day, I was able to regain everything and then some in a matter of a week. And all of this with writing sub 4000 strikes which had like 1 delta or less. This just goes to show that, as much as the backtests are nice, they fail to capture the adjustment in delta and strikes that the investor makes once volatility has spiked.

I had a loss in the first week of January. But the rest of January was very profitable!

I’m new to ERN but run a similar system. Does anybody else use long-dated calendar spreads to hedge their tail risk? As long as I’m opening the calendar spreads with normal/lowish VIX, they pay for themselves pretty quickly and cash out nicely when the VIX pops a couple times per year.

Can confirm that a long put circa 90 DTE at 30% OTM is effective for sharp, sudden declines similar to Mar 2020. Less effective for slow grinds down like 2008-9

https://spintwig.com/spy-long-put-90-dte-10-and-30-otm-tail-hedging/

Great article! Thanks for sharing. Naked short option strategies like ERN’s feel a bit scary (even at low deltas)…but at the same time I feel like selling those low-delta options leaves way too much money on the table. Any ideas what the most profitable delta is to sell in the long-run? After a couple years doing this, my strategy is producing much higher returns selling strangles around a 25 delta…but those are really diagonals that are well risk-defined.

Since I prefer selling strangles to just puts, my only problem has been those quick moves upward after a big drop. My hedges work and those big juicy premiums after a drop make back losses very quickly. But when SPX moves up relatively quickly after a pullback and the VIX drops, I find myself losing on my short calls and not being well-enough hedged with my long calls because it was too expensive to buy long calls after the VIX pop. Make sense?

I’m just curious if others have had this problem and what you all do to fix it. My current thinking is to run a ton of calendars and take profit when the VIX pops to that 25-30 range. Then to invest those profits in more calls to protect against a fast rebound. But it’s so hard for my cheap-ass to invest those profits into long calls that will do nothing for me 80% of the time.

Is this why so many of you only work on the put side? It makes sense. But at the same time I think strategies like these should be yielding 30-40% annually and I hate leaving too much profit on the table.

Total P/L of all the studies is available at https://spintwig.com/all-backtests/

This should answer the question about profitability at various delta targets.

The latest short call study (half of your strangle strat) is available at https://spintwig.com/spx-short-call-7-dte-s1-signal-options-backtest/

At best, returns are less than 3mo treasuries. At worst, the strat has a negative P/L.

If you feel you need to hedge, reduce position size. It has the most certainty (guaranteed to lower exposure), greatest degree (1:1 reduction in exposure), and lowest cost (FREE). Haven’t found a hedge that outperforms. Added bonus, park those extra dollars/margin not used due to smaller position size in a HYSA / HYCA that pays 1.1% and the “smaller position size” hedge will have a positive value. Win win win.

I love your 7DTE delta comparison. That’s what my gut tells me, and thanks so much for doing that work. So glad I found this conversation. I feel like a lone weirdo waking up at 0345 three days a week here in Thailand to sell options…but now I know there are other nuts out there playing the game in their IB accounts, also living the good life 🙂

strangles seem like a way to add more income from the upside. But I have trouble shorting the upside. It feels unpatriotic. 😉

I like the idea. Haven’t implemented it yet, but it’s on my radar screen. For exactly the reasons you mention.

Just finished reading ALL the comments. Wow. There are a lot of smart people commenting here. Thanks so much for all the knowledge. I’m typically short more volatility than long. But “Top Traders Unplugged” has been putting out a fantastic series on volatility and I’m starting to see many of the benefits of a long-vol strategy. Namely: compounding. Is anybody else fearful of compounding these short-vol strategies? I am. I’ve been retired for about four years, so the options-selling income has been great, but I’m fearful to grow my options investment over $150k…and that $150k is spent on the long-dated long option legs of my diagonals I use to hedge and be more risk-defined.

Anyway, I have so much respect for all the commenters in here and really learned from the conversation. If anyone has heard this podcast episode: https://www.toptradersunplugged.com/podcast/07-volatility-series-participate-protect-ft-dave-dredge-january-12th-2022/ I would love to hear your thoughts. My gut is telling me that it IS possible to be long and short vol at the same time without hedging out all profits…but I’m no professional. Thanks again, everybody!

short vol is the way to go because normally realized vol is smaller than implied vol.

If you want to do this tactically, e.g., buy cheap insurance when vol is low, than more power to you. But over long stretches, long-vol is a losing proposition.

Thanks for your response. Yeah, I totally agree. I’m net short vol. But it feels too risky to sell more and more and grow the strategy. I’m hoping a parallel long vol strategy could be the machine that helps me start compounding…or maybe just throw long vol profits into VTI and grow that investment. I don’t know. Fun games we play!

FWIW, I have scaled down my leverage ratio over the years as the account grew from a play-money account to serious business that’s supposed to cover all of our retirement expenses. 🙂

Badass! It’s amazing how people like those of us commenting on this article have independently discovered such similar investing tactics. I “retired” about four years ago thanks to real estate income and dividends. But now about half of my expenses are covered by selling options. By sharing your experience and results, you’ve made me feel even more confident in our shared thesis that there are options strategies out there yielding a lot of cash-flow with very low risk. Thanks for everything!

Awesome! Glad this is material was helpful! 🙂

I found his podcast appearance here: https://www.youtube.com/watch?v=zak2fSit1m8&t=41s

Much more informative!

Interesting guy!