June 17, 2020 – Welcome back to another post centered around Put Option Writing. Today we got a real treat because my blogging buddy, fellow option trader and frequent commenter “Spintwig” offered to do a guest post to perform an independent review of my trading strategy. If you don’t know Spintwig, he also retired in 2018 (at age 30!!!) from a career in ITnd now writes about FIRE and options strategies at his blog. He does a lot of interesting and important work, including careful and comprehensive back-tests of different option trading strategies, i.e., different underlying assets, different Deltas, different horizons (days to expiration), etc. I highly recommend you check out his work if you’re interested in option writing!

Oh, and following the guest post, I’ll also give a quick update on how my portfolio did during the crazy, scary volatility last week! Stay tuned!

Over to you Mr. Spintwig…

Thank you BigERN for the opportunity to peer review your options strategy and publically share the results with you and your readers. I’ve relied on your research in my own journey to and through FIRE and I’m happy to be able to add to the discussion and body of research.

A few years ago I stumbled upon BigERN’s blog as I was researching safe-withdrawal-rate topics. Among the material was a novel idea: selling put options on the S&P 500 index could mitigate sequence-of-return risk.

The concept was straightforward but I wanted to know if there was an optimal approach or if it could be applied to other indices and have similar results. Would it be advantageous to replace a traditional buy-and-hold portfolio with an options trading strategy? Unfortunately, there were no definitive or trustworthy answers to this question on the internet so I set out to do my own research and publish what I find.

Research Basics

The act of evaluating how a trading strategy performed over time is called backtesting. What I wanted to do was backtest various option strategies on the S&P 500 to see how they perform. I won’t bore you with the details of my research methodology; the takeaway is that the backtest results are publicly documented, fully transparent and, most importantly, compared against a relevant buy-and-hold benchmark.

There are two key attributes to keep in mind when evaluating performance: compound annual growth rate (CAGR, or sometimes called geometric return) and volatility. The timing and severity of volatility is the driving factor behind sequence of returns risk.

According to BigERNs data, an investor is better able to handle equity volatility, and consequently reduce sequence of returns risk, by writing options on an equity index as opposed to investing in the index directly. Let’s see how BigERNs option strategy performs when maximizing the effects of the central limit theorem by performing a formal backtest. The option strategy will then be compared against popular buy-and-hold benchmarks.

Backtest Structure

In BigERN’s 3rd update on option writing, he makes note of a few details regarding his strategy. In particular:

- Positions are opened every Monday that expire Wednesday, every Wednesday that expire Friday and every Friday that expire Monday

- Positions are held till expiration

- The time value target is roughly equivalent to a 5-delta position

- 2-2.5x leverage is used

- The underlying is SPX (the S&P 500 index). I’ll be substituting this with SPY (the S&P 500 ETF) for the purposes of making the strategy more accessible to those with smaller accounts.

This is enough information to perform a backtest. To spice things up, let’s see what happens when different amounts of leverage are used. Also, there’s a popular strategy that says to close short option trades at 50% max profit to boost performance. We’ll look at that as well.

As for the benchmark (data courtesy of Portfolio Visualizer), let’s compare against the following buy-and-hold portfolios with dividends reinvested:

- 100% SPY

- 80/20 SPY / IEF

- 60/40 SPY / IEF

[ERN: The SPY is one of the most widely used S&P 500 index ETFs and the IEF is a popular ETF to get exposure to (intermediate) 7-10-year U.S. Treasury Bonds. ]

The backtest will measure from Feb 21 2018 through June 5, 2020.

[ERN: The way I understand the underlying calculations that spintwig sent to me, the SPY and SPY/IEF returns refer to the Feb 2018 to May 2020 monthly returns from Portfoliovisualizer.com, so the returns don’t line up 100% with the put strategy returns!]

Feb 21 2018 is a special date in that it’s right after Monday-expiring weekly options on SPY were introduced (see SEC release 34-82733).

[ERN: Too bad this doesn’t capture the Feb 5, 2018 drop, but so be it! We do have enough vol spikes in there, including the fourth quarter of 2018 and February/March 2020!]

All in, we have the following backtest configuration:

- Symbol: SPY

- Strategy: Short Put

- Start Date: 2018-02-21

- End Date: 2020-06-05

- Position Entry:

- every Monday

- every Wednesday

- every Friday

- Trade Timing: 3:46pm ET

- Strike Selection

- 5 delta +/- 0.5 delta, closest to 5

- Position Exit:

- 50% max profit or expiration, whichever comes first

- hold-till-expiration

The nitty-gritty details and assumptions of the backtesting methodology such as margin collateral, margin calls, moneyness of positions, commission, slippage and more can be found here.

Let’s see how the strategy performs!

Backtest Results

Starting Capital

Since backtests are backward-looking, hindsight bias can be used to identify the starting capital necessary to achieve various leverage targets.

The rule of thumb is 20% of margin utilization = 1x leverage. Thus, using all available margin is comparable to 5x leverage.

Due to the dynamic nature of options, maximum margin utilization is not a linear function. In other words, the capital needed for 2x leverage is not exactly half the capital needed for no leverage (1x).

Compound Annual Growth Rate

Here we see the returns of BigERN’s strategy, namely the 5D 2x hold till expiration, outperforms 2 of the 3 benchmarks with regard to geometric return.

Since we know his leverage target is between 2-2.5x and thus the CAGR will be between 7.03% and 9.79%, we can reasonably conclude that his strategy outperforms or is on par with all relevant benchmarks.

[ERN: This is a slightly unfair comparison because it ignores the fact that my strategy is purely on margin whereas the benchmark portfolios eat up your entire margin cash. Specifically, with my put writing strategy, you have essentially all of your margin cash available to earn some additional interest income. But depending on how crazy you go with pumping up your yield, it will also increase the risk. 🙂 So, a fair comparison would have been to subtract a cash yield from the SPY/IEF benchmarks or add some interest-bearing asset to the put strategy returns!]

Meanwhile, exiting trades at 50% max profit lowered returns. This is from a combination of 1) lower premium capture, which we’ll see next, as well as 2) increased commission drag (the cost to close a position).

[ERN: Exiting the position early after earning 50% of the profit only makes sense if you immediately write another option so as to avoid any zero-delta days. In other words, if my Wednesday options already earned almost all their premium on Tuesday, I might as well close them and sell a new batch of options with either the Wednesday or Friday expiration. That will increase your revenue but also your risk!]

Premium Capture

Premium capture is the same across leverage targets, which is expected. By managing trades at 50% max profit we see average premium capture is closer to 50%.

Another way of looking at this table is: when holding till expiration, losses consume 44.57% of profits. When taking profits, leave a little less than half of the proceeds in the trading account for the eventual loss.

Speaking of losses, how often does this BigERN’d strategy lose?

Win Rate

Not very often – less than 4% of the time. However, those losses are substantial. Just 3.33% of the trades wipe out nearly half of the gains!

[ERN: Yeah, you got that right! The spirit of the strategy is “picking up nickels in front of a steamroller,” so the occasional loss can be substantial! It’s not “Picking up Benjamins in front of a baby stroller” for sure!]

There were 330 trades in the 5D hold-till-expiration backtest; 11 of them were losers. The average win was $13.29 and the average loss was $163.45. The largest win was $93.50 and the largest loss was $428.50.

[ERN: For comparison, I had 9 loss events during that time. During the high-vol periods, I normally reduced my Delta a little bit (as detailed in last week’s post) so, I might have avoided some of the losses along the way, though also at the expense of lower gross option revenue!]

Volatility

It’s easy to see that introducing and increasing leverage increases volatility.

BigERN’s strategy has 82% less volatility than a 100% SPY portfolio despite the strategy being based 100% on the SPY equity index. It even has 66% less volatility than a conservative 60/40 portfolio!

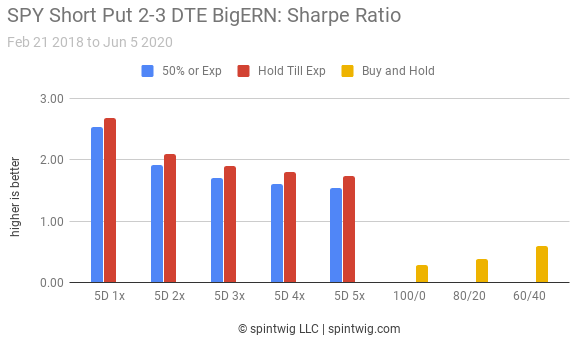

Sharpe Ratio

When we divide the compound annual returns by the annual volatility we get a number called the Sharpe Ratio. It describes a strategy’s risk-adjusted return, or how much return is generated per unit of risk.

The BigERN strategy has a substantially higher Sharpe ratio than any of the buy-and-hold portfolios. Let’s dig a little deeper into the risk details to see what the max drawdown looks like.

Max Drawdown

The max drawdown of BigERN’s options strategy is a fraction of the benchmark portfolios. This is exactly what we want as it mitigates sequence of returns risk.

Overall Performance

BigERN’s strategy is highlighted in neon green. Commensurate with the high Sharpe ratio, the equity curve moves up and to the right while experiencing a fraction of the volatility associated with any of the buy-and-hold portfolios.

Discussion

BigERN’s strategy performance is pretty impressive and it appears to check all the boxes to solve the sequence of returns challenge – far lower volatility and ample returns. When we consider the fact that BigERN’s leverage target is a little above 2x, the bright green line is actually higher than all three buy-and-hold equity curves.

Despite the backtest duration being only 2 years and 3 months, there is a good mix of swift and deep declines along with strong and prolonged recoveries over the evaluation period. This timeframe should provide a decent survey of strategy performance over different market environments.

I’d like to turn it back over to BigERN to get his input and reaction.

OK, back to Karsten again:

In this day and age, everyone can just post on the web and showcase their awesome, foolproof strategies and how smart they are. But you lack credibility unless other people try for themselves and repeat and replicate your success.

That’s why I thought it was such a great idea to get Spintwig involved to perform an independent review. This was extremely helpful! Thanks for doing this!

Of course, I should state the obvious: my actual strategy, the way I implement it is still slightly different, for (at least) three reasons:

1: I don’t strictly adhere to the 5-Delta rule, as I outlined in last week’s post. Here’s my actual Delta over time. You can see that I started out with a slightly higher Delta but I’ve since scaled it back a little bit from a 6 to 7 Delta to a ~5 Delta. Also notice that occasionally I’m operating at a much lower Delta. Those periods coincide with the vol spikes (see the orange line, inverted scale on the right).

2: I occasionally trade some additional discretionary contracts, sometimes only intra-day, sometimes on the off-days (Tuesdays and Thursdays). I wrote about the philosophy last week!

3: I keep some additional interest and dividend-paying assets in my portfolio, so the margin cash isn’t sitting around and getting bored. So I like to look at both the put-option-only portion of the portfolio (comparable to Spintwig’s numbers) but also the total portfolio return with the interest/dividend-income-producing asset included. Over the same 2/21/18-6/5/20 time span, I had return and risk values just below the 3x strategy in Spintwig’s simulation even though I was running this at only about 2.4x leverage. I guess I added a little bit of extra return but also risk through my discretionary trades.

As I’ve mentioned here before, the biggest risk in my portfolio, recently came from holding some more exotic dividend-paying assets (muni bonds, leveraged muni bonds through closed-end funds and individual preferred shares), while the scary-sounding derivatives trading has a pretty low risk right now.

But despite all the differences, we still get qualitatively and quantitatively consistent results if we compare the ERN Puts Only strategy and the Spintwig 3x version.

A quick favor to ask before we get to the issue of last week’s market drop: Please head over to the site “Hack Your Wealth“. I chatted with my buddy Andrew on his podcast about FIRE, Sequence Risk, Safe Withdrawal Rates, the flaws of the 4% Rule and much more. I had a lot of fun and I’m sure you’ll all enjoy that episode, too!

A quick update on last week’s volatility spike

When I published my post last week on Wednesday I proudly declared how well the strategy has performed so far in 2020. Ironically, it took only a single day for Mr. Market to catch up and get me a little bit nervous. Shouldn’t have tempted the market Gods! 🙂

But fortunately, my portfolio survived the event. Just to be sure, it was a scary time, especially because the big drop occurred on Thursday, only one day into the 2-day option trade. But luckily, the market recovered again on Friday and only half my put options landed “in the money.” So the loss was manageable. Here’s the YTD P&L from the put writing strategy:

My strikes for June 12 we between 3010 and 3055. Since the index dropped all the way to 3,002 on Thursday we saw this significant intermittent loss on Thursday. But with the recovery on Friday I ended up with “only” half of my options in the money with strikes at 3050 and 3055. My other options with strikes at 3010, 3025 and 3030 were safe.

So, there you go! The strategy is still holding up pretty well despite the big drop last week!

Hi Ern ,

I have been trading this strategy for a while already. One of my thoughts is to diversify through time, is this something you do consistently?

Maybe place 1/3 of the position on the close (2DTE) , 1/3 on next open and 1/3 at midday. In that way you minimize the dependence of luck , and is a more pure game over time.

I am wondering if you go all inn at one time or spread de allocation

thanks !

But are less diversified over time. You take more risk on M/W/F than on T/Th. That’s undiversified.

It still all boils down to my point in Part 4: Try to equalize the delta. Then you have equal risk throughout the week.

Of course, that may imply that on a T or Th, I sell seome additional puts if the W/F options are way OTM.

Or it may mean that on a M/W/F if the options expiring that day are way OTM I sell a few more same-day options and/or sell the next expiration day options already early that morning.

HI Ern,

I am trying to do this strategy in my retirement account and had bad loss- 30 X. Is there a back test with 6 x and 12 X stop loss? Thanks

What is the definition of “30X”?

30x weekly income?

Big ERN…I started trading this method a month ago using paper money in my TOS platform. I have a bunch of winning trades at this point, and I am still refining how I trade each Mon, Wed, Friday. I am a retired Army Colonel and I have traded the stock market using buy and hold methods for over 25 years. I am liking this selling puts at the 5 & 6 Delta with 2-3-4 DTE days to expiration. Many thanks for your Blog and your articles they help and mentor us newer traders on selling Put options. I plan to continue to trade this method, and eventually move to my live TOS account. Please keep your great Blog posts coming our way. You are a Patriot and Great American.

Thanks, Keith! That’s awesome. Always keep in mind that most of your trades will be winning trades until a big loss happens. So, don’t lever too much. I did that in 2011 and lost >60% in a week after getting overly confident from lots of winning trades. So, work yourself into this slowly and see how you handle the risk and the bad days! 🙂

And likewise, thanks for your kind words and thank you for your brave service to the greatest country in the history of the world! You’re a Great American, too. 🙂

Hello ERN,

thank you for your blog and this interesting strategy. I am wondering what happens to it if we experience a crash akin to October 1987. If I get it right, it would destroy almost 50% of the put writing part of your portfolio given your leverage. What should we do if this were to occur? Can we somehow hedge against it? Is this something to be afraid of when implementing your strategy?

No, it wouldn’t. Not sure where that 50% number comes from. You’d have sold puts at least 10% OTM, so with a 21% drop on Oct 19, you’d have lost around 10% on the put. With 2-2.5x leverage that would have been a 20-25% loss. Bad but not fatal. Certainly not 50%.

Thank you for the answer. I am new to selling puts so excuse me please if I ask stupid questions – a) how do we know we would have sold puts in October 1987 with strike 10% below market price at that time?

20-25% is a lot to swallow. b) What would you do after such a loss? Would you continue selling puts and try to get back to even with option premiums being significantly higher after such a large drop in SP500? Or would it be better to abandon the put writing strategy and invest the option part of the portfolio into the stock market and hope for a quick recovery?

The VXO index was at 36 the Friday before the Black Monday. Looking through my trading diary, I have sold puts 10%+ out of the money when the VXO index was equally elevated.

After a big loss I do exactly what I always do. Sell more puts. Because everybody’s hair in on fire, the premiums will be extremely rich following a big blowup. In March 2020 I made record profits selling puts. Not a single put went in the money.

Hoping for a quick equity recovery would have worked in 2020. But not in 2007/8/9. I’d be careful about that. Normally, selling puts is the better strategy during a extended equity bear market.

Thank you ERN for your time and the answer. I get it.

Thanks for this series of posts on options writing. I have been getting my feet wet on this for the since the beginning of the year and after a while one begins to see the options pricing nuances more clearly which got me wondering. Rather than 5 DTE and 2-2.5x leverage, why not 10 DTE and no leverage to 1.25x?

As far as SPY/SPX is concerned, higher leverage at a lower delta usually yields a higher sharpe than lower leverage at a higher delta.

My buddy Spintwig (https://spintwig.com/) has done all sorts of backtests ith different DTE.

My case for the shortest possible DTE is always: the Central Limit Theorem: Have the highest # of trials to make the skewed distribution closest to Normal when looking at the annual average. When using longer horizons you lose that.

That’s only if you’re holding them to expiration though. You could sell a long DTE put, buy it back 2 days later, and you’d be selling just as many as if you sold 2 DTE puts and let them expire.

Seems like the real advantage of short DTE is the high negative theta- their time value declines rapidly. But it comes with the most gamma risk too (any random thing could change their price dramatically).

No. The long-DTE will have a lot of downside risk and negative skewness even when held over only 2 days. So, I still prefer the 2-3 DTE and holding to expiration.

Hi , I performed some back test with strike price 3% to 9% away. Time from 2007 to 2021. I found that

2007 to 2009 most profit: 9% away

2010 to 2014 most profit: 6% away

2015 to 2017 most profit: 3% away

2018 to 2021 most profit: 7% away

Adds up: Regular sell put strike price at under 5% will lose money, sell at 5%-9% away is profitable, 6% to 7% most profit.

PS: If we can read the market, sell put 3% at steady bull market, 7% up at dangerous market.

Repege,

When you say 2018 to 2021 most profit: 7% away ?

Can you clarify that ?

Do you mean to sell at a Delta 7 ?

I am trying to understand exactly what you are saying in this post.

Thanks in advance.

Not native speaker sorry for poor English. I chose open price as a reference point. For example, SPX open at 3000, 7% means just sell at 2790 for very few premiums. If we try to disciplinarily sell at a 3% lower price 2910 (delta maybe 6-7). We will lose so much money last year March and make less profit.

In other words, %OTM is the criteria for strike selection (as opposed to delta).

This has the effect of dialing up risk during high-volatility periods and lowering it during low vol periods.

What DTE were the positions in your backtest? Based on the numbers presented, my guesstimate is that these were 45DTE.

That’s clear. Thanks!

As I mentioned here and elsewhere, the fixed % OTM strikes will not be very useful in practice. 7% OTM looks like a lot today: ~4100 strike if the index is at 4400. Not much delta and option premium there.

7% OTM would have been an extremely risky short-put in March 2020.

In other words, the Lord gave us the Option Greeks. Why not just them?

People have replied already. But let me weigh in.

I’m not a fan of this approach. I prefer targeting the Delta plus a few other metrics. See Part 4 of the series, section “What strikes do I target?”

https://earlyretirementnow.com/2020/06/10/passive-income-through-option-writing-part-4/

Besides, how do you know *ahead of time* what % OTM works best? Are you sure 7% will remain the best for the rest of 2021? What should I use in 2022?

I’ve a question, which is: how is this passive?

Seems like if I were to follow the strat I’d obsessively follow the markets which seems not passive at all — or maybe there’s some obvious thing where one could ‘passive-fy’ this by having these orders go through automatically through their broker, and I just never login?

It’s passive in the sense that there is no market timing. I do the same every M/W/F.

I do not have to follow markets “obsessively”.

If need be I can do all my daily trades on my Android phone on one single ride up the ski lift.