One of the most requested topics for our Safe Withdrawal Rate Series (see here to start at Part 1 of our series) has been how to optimally model a dynamic stock/bond allocation in retirement. Of course, as a mostly passive investor, I prefer to not get too much into actively and tactically timing the equity share. But strategically and deterministically shifting between stocks and bonds along a “glidepath” in retirement might be something to consider!

This topic also ties very nicely into the discussion I had with Jonathan and Brad in the ChooseFI podcast episode on Sequence of Return Risk. In the podcast, I hinted at some of my ongoing research on designing glidepaths that could potentially alleviate, albeit not eliminate, Sequence Risk. I also hinted at the benefits of glidepaths in Part 13 (a simple glidepath captures all the benefits of the much more cumbersome “Prime Harvesting” method) and Part 16 (a glidepath seems like a good and robust way of dealing with a Jack Bogle 4% equity return scenario for the next 10 years).

The idea behind a glidepath is that if we start with a relatively low equity weight and then move up the equity allocation over time we effectively take our withdrawals mostly out of the bond portion of the portfolio during the first few years. If the equity market were to go down during this time, we’d avoid selling our equities at rock bottom prices. That should help with Sequence of Return Risk!

So, will a glidepath eliminate or at least alleviate Sequence Risk? How much exactly can we benefit from this glidepath approach? For that, we’d have to run some simulations…

Background on glidepaths

Target date funds use a time-varying asset allocation depending on the participant’s age. The idea is that young investors can and should take on more risk and hold a higher portfolio share in equities. Then, as retirement approaches, investors shift more into bonds to reduce risk. In fact, you don’t even have to do this shift yourself; Vanguard or whoever your provider may be will do it for you! Here’s Vanguard’s take on the glidepath, see chart below. The equity share (domestic plus international) in their target date funds starts at around 90%, drops to around 50% at the traditional retirement age of 65 and then further drops to 30% by age 72.

But recent research has shown that Vanguard (and many other providers of target date funds) actually got it wrong, at least for the post-retirement glidepath. The glidepath of equity weights should ideally start to increase (!) again once you retire. Michael Kitces wrote about this topic (on his blog here and here and in an SSRN working paper joint with Wade Pfau) and proposed to keep the minimum equity share at or around the retirement date before starting to raise the equity weight again during retirement.

The rationale is that the rising equity glidepath in retirement would be insurance against sequence of return risk. After all, the number one reason retirees run out of money is bad returns during the first few years of retirement. A low equity allocation shields you from short-term equity volatility, but longer-term you will need the high equity share to make it through 40, 50 or even 60 years of retirement. So, a dynamic stock/bond share would thread the needle to achieve both long-term sustainability and short-term protection.

Of course, as with all of the traditional retirement research, it has limited use for the early retirement community. My experience has been that a lot of the research targeted at the traditional retirement crowd, calibrated to capital depletion over a 30-year horizon, is less applicable to the FIRE crowd. For example, Safe Withdrawal Rates have to be lower over a 60-year horizon than over a 30-year horizon. And, equally important, equity weights have to be higher over a 60-year horizon to ensure long-term sustainability. Case in point, the 30% equity weight at the retirement start and 60% in the long-term as indicated in the Kitces chart above would be way too low for early retirees!

So, when unhappy with the whole Kit(ces) and Caboodle of hand-me-down research, what am I supposed to do? If you want something done and done right, you just have to do it yourself! That’s where the Big ERN simulation engine comes in handy!

Simulation assumptions:

- Monthly data from January 1871 to July 2017.

- A 60-year retirement horizon.

- Retirement dates from January 1871 to December 2015 (with extrapolations using conservative return forecasts for bonds and stocks beyond July 2017).

- Final value targets of 0% (Capital Depletion), 50% of the initial real value and 100% of the initial portfolio (in real terms).

For each of the 1,700+ cohorts, we calculate the safe withdrawal rate, i.e., the initial withdrawal percentage that exactly achieves the final target value after 60 years, assuming withdrawal amounts are adjusted for CPI-inflation regardless of the portfolio performance. As usual, we calculate the SWRs for the 21 different static Stock/Bond allocations (0% to 100% stocks in 5% increments). But we also simulate a total of 24 different glidepaths, comprised of the different combinations of glidepath parameters:

- Two different end points: 80% and 100%. Why not lower end points? As we will see later, the long 60-year retirement horizon necessitates a much higher (long-term) equity weight than the often-quoted 60% or even 50%.

- Three different starting points: 20, 40 and 60 percentage points below the end point.

- Two different slopes. Notice that I had to increase the slopes for the glidepaths that cover more ground, otherwise, the transition would take way too long:

- 0.2% and 0.3% per month for the glide paths starting 20 percentage points below the max,

- 0.3% and 0.4% for the paths starting 40 percentage points below the final target,

- 0.4% and 0.5% per month for the paths that start 60 percentage points below the final target.

- Two different assumptions for the glidepaths: Passive vs. Active

- Passive means that we stubbornly increase the equity weight every month by the slope parameter.

- Active means that we increase the equity share only when equities are “underwater,” i.e. when the S&P500 index is below its all-time high. We want to avoid shifting out of bonds too early, i.e., before the market peak and then having insufficient bond holdings when equities take a dive.

The “active” glidepaths, of course, are dependent on the retirement cohort. The transition from, say 60% to 100% equities would take a little bit longer depending on how equities perform during that time, see a sample of active glidepaths for the January 1965 to January 1980 cohorts below:

Results:

Let’s start with the failure rates of our preferred safe withdrawal rate, 3.50%. In the chart below, I plot the failure rates of three static equity weights, 60%, 80%, 100%, as well as the various glidepaths. Those with a final equity weight of 80% at the top and with a final equity weight of 100% at the bottom. First, let’s do this for all 1,700+ monthly retirement cohorts regardless of equity valuations (“All CAPE”):

Some patterns emerge from this chart:

- There will be at least a few glidepaths with lower failure rates than the static allocations. It seems that the 80% to 100% and 60% to 100% glidepaths deliver consistently lowest failure rates, regardless of the final value target!

- Who would have thought that the maximum long-term equity weight delivers the lowest risk? This goes back to the superior equity long-term expected returns; once you make it through the shaky first 5-10 years exposed to sequence risk you want to max out the equity weight!

- The very long transitions over 60 percentage points (20 to 80% and 40 to 100%) tend to be pretty consistently inferior to the other glidepaths. The 20 to 80% glidepaths are even inferior to the static 80% and 100% allocations! Apparently, the initial stock weight was too low and/or the transition took way too long (even with the accelerated slopes of 0.4% and 0.5%!)

Do glidepaths become more useful when the Shiller CAPE is high?

As we have pointed out numerous times before (for example, in Part 3 of the series), the Shiller CAPE is strongly correlated with safe withdrawal rates. Plain and simple: Sequence of Return Risk is elevated when the CAPE ratio is high! Is that also reflected in the glidepath performance? You bet, see chart below:

- First, notice that the failure probabilities of the static rules are now much higher due to the higher CAPE ratio. Even a capital depletion target fails with about 17%, 7% and 12% probabilities for the static equity weights of 60%, 80%, and 100%, respectively.

- Most glidepaths pretty consistently beat the static equity weights. The consistently best performers are the 60 to 100% glidepaths and the active glidepaths perform slightly better than the passive ones. The failure rates are less than half those in the static allocation simulations!

- The 20 to 80% and 40 to 100% glidepaths are still inferior to the other glidepaths. And the 20 to 80% glidepaths are inferior to the even the static asset allocations.

More on the distribution of SWRs: Failsafe and other SWR percentiles

A lot of very risk-averse retirees like to set their SWR to the failsafe SWR in historical simulations. That seems very conservative, but I can see where they are coming from. If your strategy would have handled the Great Depression, the nasty 1970s/early 1980s, and the volatile 2000s you can probably also use it in 2017 without too much worry!

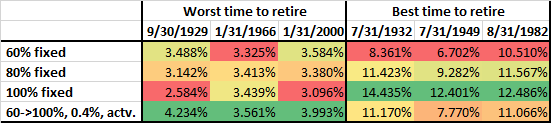

In the table below, I calculate the failsafe SWR, i.e., the minimum historical safe withdrawal rate (60-year horizon, 0% final value), as well as some other percentages (1st percentile, 5th, 10th and 25th). So, for example for the 80% fixed equity allocation, the absolute lowest historical SWR would have been 3.14%. A 3.43% initial SWR would have failed 1% of the time, 3.59% would have failed 5% of the time, 3.86% would have failed 10% of the time and 4.48% would have failed 25% of the time. I don’t think planning for a 25% or even 10% failure probability is very prudent – personally, I try to target a failure probability in the single digits, e.g., 5% – but I display the numbers just in case someone wonders.

The left portion of the table is for all possible retirement start dates (about 1,700 of them, monthly data from 1871 to 2015). The right part of the table is for those months when the Shiller CAPE ratio is above 20. In the top portion of the table, I also marked with green boxes the maximum value among the static asset allocation rules in each column. Notice how the maximum in each column is at between 75 and 100%! To make it through a 60-year retirement, you can’t have a 60% or even 50% equity share. That only works for 30-year horizons! Also notice that with a CAPE>20 all numbers in the far right column are <4%, so the 4% had a failure rate of over 25% regardless of the equity glidepath!

In any case, 60 to 100% glidepaths generate the consistently best SWRs. For the über-conservative FIRE planners who are looking for the failsafe 60-year SWR conditional on our current 20+ CAPE environment, a fixed 75% stock allocation would allow a withdrawal rate of only 3.25% and that’s already the max over the static allocation paths! The 60 to 100% glidepaths would have allowed between 3.42 and 3.47%. That’s an improvement of between 0.17% and 0.22%. It doesn’t sound like much but it’s an improvement of between 5 and 7% of annual withdrawals. Not bad for doing a simple glidepath allocation.

Likewise, if I’m OK with a 5% failure probability conditional on a CAPE>20, then the static stock allocation of 80% would give me an SWR of 3.47%. The glidepaths would have allowed between 3.57% and 3.63%. Only an additional 0.16%, but that’s about 5% more consumption every year!

So, we won’t get all the way to 4%, but we bridge about one-third of the way, simply by playing with the asset allocation over time.

A small caveat, though; the calculations raise the question: do we get something for free? Is this some sort of a money-making arbitrage machine? Of course not! A glidepath will deliver a higher safe withdrawal rate if you have an equity drawdown early on in retirement. But the opposite is true as well. That 60 to 100% glidepath that performed so well during the major Sequence of Return Risk disasters will also underperform if stocks rally during the first few years of retirement. Let’s look at the table below that displays the SWRs of the 60%, 80% and 100% static equity weight and the 60 to 100% glidepath with a 0.4% monthly slope conditional on equity performance. As we already know, it beats the static equity allocation rules significantly when retiring at the market peaks (=worst time to retire). But the glidepath also falls significantly behind the 100% equity allocation if you were to retire at one of the three market bottoms (=best time to retire). It handily beats the constant 60% allocation and is slightly inferior to the 80% constant equity allocation. But I wouldn’t really care too much about falling behind in that case. You still get phenomenal SWR, just a little bit worse than the even more phenomenal SWRs of the 100% equity allocation.

Conclusion

Early retirees need the power of equity expected returns to make the nest egg last for many decades. Even more so than the traditional retiree at age 65! But that exposes us to Sequence of Return Risk. An equity glidepath can alleviate some of the negative effects of Sequence of Return Risk. But it shouldn’t come as a surprise that you will never completely eliminate the risk. For a given withdrawal rate, say 3.5%, we can only reduce the failure rate while leaving some residual risk. And likewise, the 4% rule would still not be safe for today’s early retirees even with an equity glidepath.

Moreover, an equity glidepath is like an insurance policy. A hedge against a tail event! On average it will cost you money, but if and when you need it the most it will likely pay off. Exactly when the static stock/bond allocation paths had their worst sustainable safe withdrawal rates you get slightly better results but you also give up some of the upside if the equity market “decides” to rally some more right after your retirement. But that’s a good problem to have!

Fascinating post! I listened to you on the ChooseFI podcast! Thanks for providing further details on how to deal with Sequence of Return Risk. Both part 18 and 19 were very thought-provoking! I never expected one can avoid SORR, except for becoming a market timer, but good luck with that. Have you considered combining the equity glidepath with the CAPE rule? Sorry if that’s a stupid question? 🙂

Thanks, Ron!

Exactly, we can never completely avoid SoRR. Only mitigate it.

Very interesting suggestion: one can (actually SHOULD) also run a Glidepath and combine it with dynamic/flexible withdrawal rates. It’s definitely on my To-Do list. Most definitely not a “stupid question”!

Another Great Post (really outstanding work)! Ron’s question about combining the your Glidepath and dynamic/flexible WR work was exactly where I went, as well.

I’ve enjoyed using your google spreadsheet as a tool, using it’s SWR outcomes to compare to an ongoing manual CAPE calculation. Considering valuations gives me higher confidence in the WR max that I use in my own planning (retired in 2015 when CAPE was ~26). From your work above, it’s obvious that incorporating glide path into the mix would absolutely take this to the next level.

I wonder if the existing spreadsheet could be augmented with a field for selecting from a number of Glidepath options, and the incorporation of withdrawals determined using a selectable WR formula (fixed, or one of several CAPE dynamic options). (Not sure if what I’m suggesting is a big job, or a small one…just thinking that it might be awesome!)

Thanks!

Regarding the GPs in the Google Sheet: That’s likely impossible the way it’s implemented right now. Currently, the big SWR calculation that computed the SWR for each possible retirement start date relies on the fact that S/B allocations don’t change. That’s why the calculations are so simple. Relatively speaking! 🙂

In today’s simulations, I had to use a real number crunching software with lots of loops which is not possible to replicate in Excel/GoogleSheets. If I do find a solution I will put it in, though.

You can write javascript that runs in the background of the google sheets. Just go to Tools -> Script Editor…

Oh, my, now I have to learn javascript?! OK, I will look into that! 🙂

Hi. Any chance you’ve run (or could run) these #s for a 35 year retirement horizon? Do you have any conclusions you could share for a 35 year horizon regarding the various questions you addressed above? Do you agree with the conclusions reached by Kitces and Pfau (although they use a 30 year horizon, not 35, so don’t know if relevant?) ?Thanks.

I will look into that. I might do a 30 or 35-year simulation. Long story short, I disagree with the Kitces and Pfau conclusions. Their Monte Carlo simulations don’t take into account the mean-reversion of equity valuations.

Will do a follow-up post on that next week!

Thanks! Would be interested in what you have to say about Pfau and Kitces work in more detail (in lay persons terms). Haven’t read much disagreement with Pfau’s work. Are you able to give him feedback directly? He strikes me as an open and nice guy. Regarding someone else’s comment, did I miss something about a 5-7 year bond ladder? It must be difficult to have an audience with such an age range and such varied quant ability (me being older and with limited quant skill)! I appreciate your work to the extent I understand it!

I will prepare another blog post next week and compare and contrast my results with theirs. The main difference is that they use Monte Carlo simulations. In my view that taints their results because you can’t generate the mean reversion in equities that we observe in the data. I will then reach out to them and ask check if they want to comment! Let’s see!

And regarding the “5-7 year bond ladder” that was an inside “joke” between the PIEs’ and Big ERN!

I mentioned a bond ladder in a recent comment. It is generally useful to match the duration to the expected need date.

A 10 year bond ladder with expenses for each year would be about 35 to 40% bonds and about corresponds to the 0.3 to 0.4% ramp above.

There is no interest rate risk this way. But if interest rates crash, you can always sell the bonds early to implement the active glide path.

I woukd not actually use bonds for the first couple years though since you get better returns from cd or online savings.

Good point. Though, sometimes you WANT the interest rate risk. Bond returns had a negative correlation during the last few recessions. So if equities go down, so do interest rates, so your bond portfolio is going up.

Fantastic as always. I too was going to ask about combing strategies CAPE based withdrawals and the glide path. It took you 18 posts but you’re finally offering some good news lol. In all seriousness though I appreciate all you do and it makes me far more informed as I approach FI. Thanks

Bring out the Champagne (Costco brand, of course)! Finally some good news on the ERN blog!

Even though I always considered the Part 16 post pretty upbeat, too: https://earlyretirementnow.com/2017/06/07/the-ultimate-guide-to-safe-withdrawal-rates-part-16-early-retirement-in-a-low-return-world/ (Even in a Bogle scenario, we’ll still be OK!)

What do you think?

Thanks for stopping by, Jeff! 🙂

Yeah you’re right Part 16 was upbeat. Thanks again I’m far more confident that I’ll succeed with all this valuable information than I should have been with my original 4% and stick my head in the sand strategy.

You have amazing knack for pulling together kick-ass awesome stuff that also happens to be at the forefront of our discussions.

We expect to start around 66-70% equities (lower side if we incorporate the 5-7yr bond ladder in my cash balance pension rollover – wink, wink….) and mentioned in our recent Taming SoR beast post about incorporating a glide-path strategy. And then we have this timely post! Cool!

This may be a dumb question but do you see any differences in a “stepped” glide-path? e.g. 2% increase at mid year and at end of year, each year for 10 yrs instead of the 0.4% monthly over 100 months for the 60 to 100% passive glide-path. Or a once-yearly increase of 4%, for 10 years.

Trying to get a handle on a practical implementation of the glide-path instead of repeated monthly transactions at your favorite brokerage house(s). Especially with multiple accounts – taxable, individual IRA(s), more than one brokerage etc.

Good stuff this!! Mrs. PIE especially liked the post and was texting me this afternoon to get onto reading it…..

Awesome, thanks for the feedback. Glad you found the bond ladder suggestion useful! 🙂

Good question! For simplicity, I assume a smooth monthly glidepath. I don’t see a problem with stepping up just once a year. But remember, the assumption here in the simulations is that the portfolio is rebalanced monthly, so I assumed the shift is done together with the monthly shift.

Thanks for stopping by!

Cheers!

Amazing work, ERN!

I too was wondering about a shorter timeframe. I’m looking at 30-35 years of retirement and I’m 5 years away. I’m around 80-90% equities right now and nervously wondering if I should “steep glide” my way toward more bonds.

Good suggestion! I have so much left-over material that didn’t fit in today’s post, I will certainly do another post on this topic with a shorter horizon and also address some other questions from the comments section. Next Wednesday! Stay tuned!!!

You can write javascript that runs in the background of the google sheets. Just go to Tools -> Script Editor…

Wow, this is the best post yet in the SWR series, and that’s really saying something since all the other posts have been so amazing! My question: For someone still in the accumulation phase, presumably invested in 80 to 100% equities, what’s the best way to transition to 60% equities in anticipation for beginning the glidepath? Is there a similar, but opposite, “100% to 60% glidepath” for that?

Thanks for the kind compliment! 🙂

That’s a great question! In my view, that’s exactly how I would do it. 100% during most of the accumulation phase and then do a transition to 60/40 during the last few years before you retire. The only question is: How slowly or how quickly do you do the transition?

For people who are really comfortable with a lot of equity risk, you could do what JL COllins recommends: 100% equities until you retire, then go “cold turkey” to a higher bond share. Not everyone might be up for that.

Most folks might want to stretch out that transition to maybe 2-5 years.

But it’s a difficult question! I want to do some more research on the glidepath during the accumulation phase, that’s for sure!!!

Great stuff, good comments — very educational.

I would agree that divesting equities before retirement seems trickier than the opposite transition once in retirement. One reason is, for those of us who have been accumulating for a while — or those who were lucky to start at a fortunate time — divesting comes with a sickening dose of CG tax, esp. since we are still earning income and aren’t likely to harvest any gains tax-free.

Looking forward to your future research!

Agree completely. The divesting has to be done in a tax-advantaged account. And only there! I would definitely keep mostly equities in a taxable account!

Sorry for what may be a ‘dumb’ question but if equities are mostly in a taxable account, how do you divest (equities I assume) in a tax-advantaged account?

Wow, awesome question! Most folks in the FIRE community will have around 50% of their net worth in tax-advantaged accounts (Roth, IRA, 401k). You should be able to do the shift inside those accounts without generating capital gains taxes.

But let’s assume, in a crazy extreme case, that someone has 100% equities in taxable accounts and no retirement accounts and is a few years away from retirement. You can still invest new contributions in bonds and reinvest the dividend income in bonds. That will definitely shift a few % of the portfolio every year. A slightly unattractive solution because for the last few years, that bond interest will get hit with ordinary income taxes. For the handful of people in that situation, you might want to reconsider if you want to do a glidepath.

> For the handful of people in that situation, you might want to reconsider if you want to do a glidepath.

Exactly! That’s precisely why I thought it’d be tricky. Many more variables. Cost basis in taxable equities and taxes on bond yield (or missed yield opportunity, if munis are used) are just two. Probably hard to quantify for a mere mortal… although just might be doable for Big ERN 🙂 .

Thanks for the confidence. Do you know anyone who has no money in retirement accounts, though? I always thought, the problem for most FIRE planners is the other way around: Too much money in 401ks, which is why all the Roth Conversion ladder hacks have been invented. I’m pretty confident that most investors can shift to 80/20 or even 60/40 without realizing taxable gains before retirement starts…

Your SWR fail-safe chart is amazing. Would it be possible to get one with 0%/50%/100% final value and fail probabilities between 0% (failsafe) – 5% in 1% increments?

Forgot to mention – with 60y time horizon.

OK!

Good question! Will look into that!

Thank you ERN. You’ve built, hands-down, the best FIRE blog out there.

Thanks! You made my day! 🙂

One thing confuses me about ending with 100% equities on the glide path. Is it assumed that this glide path approach will get you to an elderly age and then you can start becoming more conservative again with your percentage of equities? Hard to imagine most 80+yr olds want to have 100% equities. I am understanding your data to mean this will take you through a 50-60yr retirement but at some point you will want to back down to a lower percentage of equities such as 60% to the end of your life? Does your data show which age is appropriate to start transitioning back down- 75, 80, 85?

Thanks for the comment. The 100% equity portfolio is a hedge against the rare cases where for the first ten or so years equities took a nosedive. If your portfolio is down by 50% and equities are cheap again, then 100% may be the less risky path forward.

But hey, if you get lucky and you avoid sequence of return risk and your portfolio is not impaired 10-20 years into your retirement, most definitely go ahead and keep 70% equities if it makes you sleep better.

You’ve probably commented on this, and I know you can’t predict the future, but just wondering if you think folks retiring in the next 2-3 years will likely be retiring into some kind of market correction and may very well be dealing with sequence of return risk? Thanks.

I definitely think that equities will return less in the foreseeable future (see my post here), but pinpointing how the exact path may look like (drop early on then a recovery or a continued bull market and then an even more severe crash in the end or just a straight line up at 5.75% p.a.) is impossible. So, yes, it’s definitely possible that folks who want to retire in 2-3 years might have to delay their plans. But I wouldn’t say that’s the most likely outcome.

Big ERN,

WOW!!! How do you keep doing this quality of work while gainfully employed?!?!?!

Even though I am dealing with post-Irma effects (fortunately relatively mild for my neck of the woods), I have gone through this 5-star post 3 times and still find it to be of immeasurable value. While I find McClung’s Prime Harvesting compelling, the complexity of implementation leaves a lot to be desired and my compliments on illuminating “simplicity that lies on the other side of complexity”.

This post may even cure my severe case of OMY syndrome!!!

Haha, thanks for the compliment! Yes, I have a job, so blogging is done mostly at night and on the weekends. Good point on McClung. Sometimes simple advice is cloaked on a lot of mumbo-jumbo. Much easier to just look for the main simple mechanism and be done! Thanks for stopping by!

Did you by chance listen to Kitces’s interview of Dana Anspach? Her firm runs projections assuming a 5% return + 3% inflation so a 2% real return (this also nets out her 1.5% advisory fee) and I think assumes a 60/40 allocation, not sure about that. She said she wants a 85% success rate I.e. 15% of the time one might need to make a ‘small’ adjustment. I know you approach this differently but just wondering if this make sense to you and/or if you have any thoughts about it? Her clients are mainly baby boomers so a more traditional retirement time horizon. Many thanks.

I presume it’s this one: https://www.kitces.com/blog/dana-anspach-rma-sensible-money-podcast-control-your-retirement-destiny-retirement-decumulation/

For the traditional retiree (65yo), you can actually withdraw 4% and inflation-adjust and have only a 2% real return. That’s because you exhaust the principal over time and the money lasts probably between 25-35 years, depending on sequence of return risk. But it’s not workable for the folks in the FIRE crowd. But even for 65-year-olds, I would find it irresponsible to use an 85% success rate. And I wouldn’t want to pay a 1.5% fee for that either. 🙂

Hi, Big ERN! I just started reading your blog after hearing you on the ChooseFI podcast. Your blog is in that perfect niche (SWR for early retirees) that I’ve been looking for! Although I’m truly impressed with the amount of work and details you put into each post, it does go over my head sometimes and I need to re-read it a few times with no distractions. I’ll admit that I rely on your conclusion section to highlight your findings. Keep up with the great work!

Regarding 0.2%-0.4% monthly glidepath, how are you changing the asset allocation? I’m not sure how practical it is for me to a do monthly rebalance, so my proposed glidepath plan for me is to withdraw the bond portion to arrive to 100% equities. (I guess I can rebalance every year or few years if the target asset allocation is off.) Do you see this approach have any significant impact?

Regarding the ‘active’ glidepath, what decision do you use to prevent the conversion? Do you decide based on a threshold value (% range of what was the all time high)? Or do we look at the CAPE to see if it’s an all time high?

I assume monthly rebalancing because that’s easier to simulate. But if you prefer less frequent rebalancing that’s fine, too. Results wouldn’t change much if you go with quarterly or even annually.

Another option is to simply withdraw bonds until they are exhausted. I looked into that in Part 13: (“Forced Bond Liquidation”) which did just as well as some of the other active glidepaths.

https://earlyretirementnow.com/2017/04/19/the-ultimate-guide-to-safe-withdrawal-rates-part-13-dynamic-stock-bond-allocation-through-prime-harvesting/

For the active GP, I assume you ratchet up the equity weight only if the S&P500 is below its all-time high. Independent of the CAPE.

ERN – tremendous work, I shall have to read this again, and I assure you there is no higher commendation from me than that!

I’m intersted in whether you think the difference in glide-paths between the Target Date Fund (Vanguard et al) and your solution is a real paradigm difference – you are coming up with radically different solutions? Or are they essentially solving for a differenct scenario? You are solving for the 60 year scenario, and they solving for the 30 year scenario. Are they irreconcilable, or are they both suitable solutions to two different problems?

I don’t know any institutional TDFs or corporate 401k’s with glide-paths like you describe. And I would like to get to the bottom of whether they are “wrong” or not…

I’ve blog-posted some (much more modest) research of my own on trying to isolate the SORR component. I want to filter out the mean reversion of equity returns and try and figure out how much risk is genuinely due to SORR. So I view my work as purely statistical, and your work grounded in the economics. I now want to revisit that to test out the ERN versus Vanguard glide-path on a purely statistical SORR basis. [hopefully I didn’t breach any etiquette with that last paragraph!]

To be perfectly honest, I have no idea why TDFs don’t adjust to the SoRR realities post-retirement. To me, it seems that this is a herding problem. Since everybody is doing it wrong nobody wants to be first to deviate.

I’m not 100% sure but….the Pension Protection Act that went into law under George W Bush defines exactly can be a “Qualified Default Investment Alternative”. The final rule from the Department of Labor says,

“Consistent with the proposal, the description provides that such products and portfolios change their asset allocation and associated risk levels over time with the objective of becoming more conservative (i.e., decreasing risk of losses) with increasing age.”

So my guess is that rising equity glidepaths don’t currently count as a QDIA meaning they are difficult to offer in 401(k) plans (or wouldn’t attract much investment) and the companies like Fidelity, Vanguard, T. Rowe Price, etc — even if they DID agree about rising equity glidepaths (and they probably don’t) — almost certainly don’t feel like going back to the government and arguing about changing the rules to get them included as a QDIA.

Wow, thanks for that! That is apparently the reason for the downward sliding glidepath! You rock!

In addition, and perhaps compounded by, the fact that TDFs are put in place by corporate sponsors who are advised by institutional advisers. For a Company your fiduciary responsibility pretty much stops when the participant retires and it’s not in the company’s interest to spend a lot of time thinking about the best withdrawal strategies for its ex-employees. Similarly the advisers have a fiduciary responsibility to the companies (their clients) but not the participants. The participants therefore fall between the cracks. Subject of a blog post perhaps?

My limited experience with the details of 401k plans is that most often retirees can stay with the company’s plan if they choose to. But most people roll over their 401k to an IRA. So, there is very little incentive to get the post-retirement path “right” in most 401k plans.

Thanks for stopping by!

Great article! Thank you so much for the effort you put into these! Assuming you have 100% in stocks and plan on doing the 60% -> 100% glide path, how would you handle changing your asset allocation from 100% -> 60%? Would you transfer the 40% into bonds the day you retire, or would you ease into it a few years early like the TDFs do? I’m guessing that flexibility on retirement date plays a factor?

Quoting ERN from an earlier response to a similar question:

“For people who are really comfortable with a lot of equity risk, you could do what JL COllins recommends: 100% equities until you retire, then go “cold turkey” to a higher bond share. Not everyone might be up for that.

Most folks might want to stretch out that transition to maybe 2-5 years.”

Yup! Great suggestion! Thanks!

Great question! Jeff answered this one already really well.

One thing to consider: Do you already know your exact retirement date? Then transition the bond allocation to that date. Alternatively, if you’re still saving toward FIRE and want to get there as quickly as possible, but are generally flexible about the date: then keep as much in equities as possible because of the higher expected return.

That’s exactly how I look at it. Since we’re aiming at early retirement does it matter is we reach it in 8 years or 10 or even 12? Probably not, so I’ll stick to high equity allocation for now transitioning to higher bond percentage slowly. When I get within a couple years I’ll look at transitioning more quickly if I think I’ll reach it.

Awesome! We think very much alike! 🙂

Have you looked into using margin at all? That’s another way to limit the sequence of returns risk – you withdraw using margin to cover your expenses each year, so you don’t have to sell any of your holdings and can remain fully invested. It seems very promising – I’ve been running some monte carlo simulations, and they’re showing better SWR with margin withdrawals than either fixed stock/bond allocations or equity glidepaths.

For example using an fixed 80/20 allocation with a bunch of assumptions (real returns of 4.5% on stocks, 0.5% on treasuries, -1.5% on margin interest, 50 year time frame, 3% dynamic withdrawal rate, etc.), I get a 7.6% failure rate when withdrawing on margin vs 15.0% when covering expenses the normal way by selling off positions each year. And besides the lower failure rate, the median terminal net worth after 50 years is also massively in favor of the margin strategy: $26.3m vs just $6.6m.

Margin comes with its own set of risks and wrinkles of course, but it’s definitely worth a close look IMO.. I’d love to hear your thoughts.

Intuitively I guess this is not entirely unlike leveraging your entire portfolio in the first place. If you use leverage, everything will improve: expected end-balance, SWR, failure rate… The only thing that will be worse is risk — and, unfortunately, this one matters.

How are you defining risk though, volatility? I would argue that’s largely irrelevant.

I wouldn’t leverage the portfolio at the beginning of retirement. That would exacerbate Sequence Risk.

But, if you have access to cheap leverage and use that to load up on equities at or close to the market bottom that should help. But in a way, it’s not that different from an equity glidepath. Selling bonds might be the cheaper option compared to margin interest.

Cheers!

It doesn’t surprise me that margin helps. You lever up high expected return with low margin interest. Caution though: margin interest will not always be -1.5% real. The Fed will eventually raise the short-term rate above 2%, maybe even 3%!

That said: Do you post your results somewhere? Thanks!!!

I finally started a blog for this! My first post goes more in-depth on the simulations I ran showing how using margin can actually reduce risk of ruin (as well as boost performance) in retirement – https://defuzzify.blogspot.com/2018/05/reduce-retirement-risk-with-leveraged.html

I’ve been thinking about this a lot lately, so I’ll have more posts soon.

Wouldn’t we expect nominal stock returns to increase to offset any rate hikes?

I don’t post anywhere at the moment – just run numbers for my own entertainment.

Not really. Once the Fed starts to bring the real Fed Funds Rate back to above zero that’s not going to lift stock returns. It might even be slightly negative for stocks.

Thanks for the great research and article. I have been looking for more information on safe withdrawal rates for early retirees. I have read the studies done by Kitces and Pfau where they highlight the SRR during the first decade of retirement, so it is helpful to see it laid out in a usable manner.

However, I do have one question on the execution of the rising glidepaths…..when do they start in your modeling? Is it the 1st year of retirement or 5th year or 10th year?

For the smaller 20% rises (i.e. 60->80 or 80->100), these are accomplished in 5.5-8 years as shown on your chart which is inside the first decade of retirement assuming the rise starts in the 1st year.

In the model, I start the glidepath in month 1.