Welcome, everyone, to another installment of the Safe Withdrawal Rate Series! See here for Part 1, but make sure you also check out Part 26: Ten things the “Makers” of the 4% Rule don’t want you to know for a more high-level, less technical intro to my views on Safe Withdrawal Strategies! Today’s topic is something that has come up frequently in reader inquiries, whether through email or in the blog post comments. Let me paraphrase what people normally write:

“Here’s how I can guarantee my withdrawal strategy won’t fail: I simply hold a portfolio with a high enough yield! Now the regular cash flow covers my expenses. Or at least enough of my expenses that I never have to worry much about Sequence Risk, i.e., liquidating principal at depressed prices.”

I’ve seen several of those in the last few weeks and it’s a nice “excuse” to write a blog post about this very important topic. So, what do you think I normally reply? Want to take a guess? It’s one of the two below:

A: Oh, my God, you got me there. This is indeed the solution to once and for all, totally and completely eliminate Sequence Risk! I will immediately take down my Safe Withdrawal series and live happily ever after.

B: Your suggestion sounds really good in theory but there are serious flaws with this method in practice. It will likely be no solution to Sequence Risk. And in the worst case, your “solution” may even exacerbate Sequence Risk!

Anyone? Of course, it’s option B. It sounds like a great idea in theory but it has very serious flaws once you look at the numbers in detail. Let’s take a look…

Chasing higher yields: A quick guide

If you’re familiar with the Safe Withdrawal Rate Series, you’ll notice that I focus mainly on equity and bond portfolios comprised of U.S. large-cap stocks (e.g., S&P 500 index) and 10-year U.S. Treasuries. (But make sure you also check out my free Safe Withdrawal Simulations Google Sheet where you can also simulate returns of portfolios with short-term bonds, gold as well as Fama-French style biases!) So, what I call a 60/40 portfolio would be closely matched by a portfolio holding 60% in an S&P 500 index fund (e.g., iShares Ticker IVV or State Street’s SPY) and 40% in the corresponding U.S. Treasury bond fund, something like the iShares ETF Ticker IEF. But that’s not the entire ETF universe! Here’s a table with a selection of ETFs in different asset classes: bonds (U.S. Treasuries, Aggregate, Corporate) and equities, together with their Expense Ratio and Dividend/Interest yield.

Side Note: The reason why I put the “Yield” in that table in quotation marks is that this is the 12-month rolling (backward-looking!) yield according to Yahoo Finance, so especially for the bond indices, the actual forward-looking yield is even a little bit higher.

That 60/40 portfolio would have a weighted dividend/interest yield of about 2.1% today. If you were to plan a 4% withdrawal rate, you’d be forced to generate an additional 1.9 percentage points, roughly half of your withdrawals, from withdrawing principal. Scary when facing Sequence Risk, right? So, I can understand the temptation to look for a higher yield. To that end, I also consider two additional portfolios. They are the ones mentioned on the fellow FIRE blog Millenial Revolution (MR), specifically, in their post on how to generate higher yields to guard against sequence risk. They call this method the “Yield Shield.” Here they are:

Portfolio 2 (MR baseline portfolio): 30% VTI (the ETF version of the famous VTSAX U.S. Total Stock Market Index), 30% International Stocks (Vanguard Ticker VEU) and 40% in the U.S. Aggregate Bond index and the aggregate bond index a higher yield because it also includes corporate bonds. This portfolio already has a higher yield (2.55%) than the Big ERN 60/40 portfolio: non-U.S. equities have higher yields and the Aggregate Bond index includes a significant portion of corporate bonds in addition to the relatively low-yielding U.S. government bonds.

Portfolio 3 (“Yield Shield” Portfolio): With Portfolio 2 as a starting point, let’s really juice up the yields:

- Out of the U.S. equity portion, move 10 percentage points into REITs with a pretty impressive yield of more than 5% and an additional 5 percentage points into the Vanguard High-Dividend-Yield ETF (Ticker VYM) with an also pretty impressive 3.2% yield!

- Out of the U.S. aggregate bond portfolio, move 10 percentage points into investment-grade corporate bonds (LQD) and 20 percentage points in Preferred Shares with a Dividend yield North of 6%.

Side note: I took the liberty of replacing their proposed Vanguard BND and VTC funds with the iShares AGG and LQD, respectively. They are very similar funds but have a longer return history. Especially, the VTC only starts in 2017 so it would be impossible to simulate how the yield shield portfolio would have performed during the Great Recession of 2007-2009.

Wow, now we’re getting somewhere! A yield of 3.69% in our portfolio! And again, that’s likely a little bit underestimating the true expected yield. Keep this portfolio and maybe a really tiny “cash cushion” to finance the gap between the 4% withdrawal rate and the 3.69% yield for a few years and we’re done and never have to worry about Sequence Risk, right? Wrong! Let’s look at how the three portfolios would have performed over the last decade or so:

- The simulation period is May 2007 to December 2018. This is the longest time horizon for which I can gather returns for all 9 ETFs used in the 3 portfolios.

- The returns come from PortfolioVisualizer.com and they are the monthly total returns, i.e., including dividends. If you like to check the returns for yourself, see this permalink with my inputs and the returns of all underlying ETFs and the three portfolios.

- I calculated how a $1,000,000 portfolio would have performed using the three different ETF allocation. This is assuming a 4% withdrawal rate, i.e., with the first month $3,333.33 withdrawal and subsequently adjusted for inflation.

See the results below. Uhm, bad news for the dividend chasers. The low-yield portfolio (60% IVV and 40% IEF) would have performed the best and ended the simulation period roughly where we started (in real terms). Portfolio 2 would be down about 25% and the Yield Shield portfolio would be down almost 30% by 2018. Clearly, this Yield Shield Portfolio doesn’t eliminate Sequence Risk. It doesn’t even lessen Sequence Risk. The Yield Shield actually exacerbates Sequence Risk! Look at how far the portfolio fell at the bottom of the 2009 bear market trough!

I could just leave it at that and be done for today. But that’s not a thorough and comprehensive exercise. I like to mainly understand why this yield chasing strategy would have failed so badly!

So, let’s look at the potential problems of this method:

Problem #1: Efficient Markets

At first glance, the higher yield strategy makes perfect sense. If you assume that you can edge out a higher yield, then, all else equal, you should be better off, right? Well, the emphasis is on the phrase all else equal. Unfortunately, that “all else equal” assumption doesn’t work so well in the real world. So, the first objection is that if this was so easy then everyone would do it and the advantage of the higher yield is arbitraged away, see below:

Case in point, Vanguard’s high-dividend yield index fund VYM. How did it perform during the simulation period? Not very differently from the VTI (U.S. Total Stock Market Index) or the IVV (S&P 500 Index). See the cumulative return chart below. Not only did the VYM fail to outperform the broader indexes by the gap in the dividend yield, the total return (= price return plus dividends) even underperformed a little bit. Thus, if you had banked on the higher dividend yield you would have lost all of it – and more – in the price return. Bummer!

Side note: I’m not here to bash the dividend investing crowd. I’ve even grown quite a bit more sympathetic to the dividend growth investing approach. I even used some “play money” to built my own little dividend portfolio replicating the “Dividend Aristocrats” ETF (Ticker NOBL). I did that in my M1 Finance account (affiliate link) where I can buy fractional shares and M1 would automatically reinvest my new contributions and dividends to rebalance to the target weights. But even I have to admit that the higher dividend yield is not all alpha. I’m OK if I lose some of the extra yield through a lower price return. Hopefully not all of it!

Problem #2: Confusing Nominal and Real Returns

When computing how much yield you need to pull this off, keep in mind that many retirees assume that their withdrawals will grow (roughly) in line in with inflation. It’s probably fair to assume that equity dividends grow in line with inflation over the long-term (and often much faster than inflation). But the same is not true for bonds and preferred shares. If you buy a bond with a principal value of $100 and a 4% yield then you may generate enough income to sustain your 4% withdrawal rate in the first year. But in subsequent years, your income will be eroded by inflation! So, for bonds, you’d need to target a yield of not just 4% but 4% plus your CPI projection! The same is true for Preferred Shares. Normally, Preferreds are structured as essentially “perpetual bonds” with a notional value of $25 and a certain fixed yield. There is no growth in your dividend income, neither explicitly nor implicitly, so you’d have to target your withdrawal rate plus CPI. Otherwise, you’d erode your purchasing power!

Problem #3: More yield may imply less diversification

That would be the scenario below: Not only is the price return lower when you chase yields but it’s so much lower, that your total return lags the low-yield portfolio! How is that possible? Well, the reason people want to hold bonds in their retirement portfolio is not exclusively to generate income but also to diversify equity risk. Holding higher-yielding bonds may expose you to more downside risk the next time a recession hits. In other words, for every dollar you generate in extra yield you may lose much more than that dollar in the price return.

So, let’s look at the correlation matrix for the nine ETFs in the three portfolios, see the table below. I sorted the nine ETFs by their correlation with the S&P 500. And guess what, the three bond alternatives to the low-yielding IEF all have higher correlations with the equity indexes. Not only that, moving to higher and higher yields (IEF to AGG to LQD to PFF) you increase the equity correlation in exactly that order!

So, it’s no surprise that some of the ETFs proposed for the 40% bond share had a very underwhelming performance during the simulation period, especially during the 2007-2009 period when Sequence Risk hit your portfolio. Look at the cumulative performance below:

- PFF (Preferred shares) with the highest yield among the four ETFs had the worst performance overall and a 50%+ drawdown in 2009, even worse than the S&P 500 equity index. Bad news from a Sequence Risk perspective!!!

- LQD did perform on par with the IEF if you look at the endpoint only. But don’t be fooled! This is the cumulative return chart without withdrawals. Because the gray line spent so much time below the blue line, LQD would have done worse due to Sequence Risk!

Problem #4: Dividends can be cut!

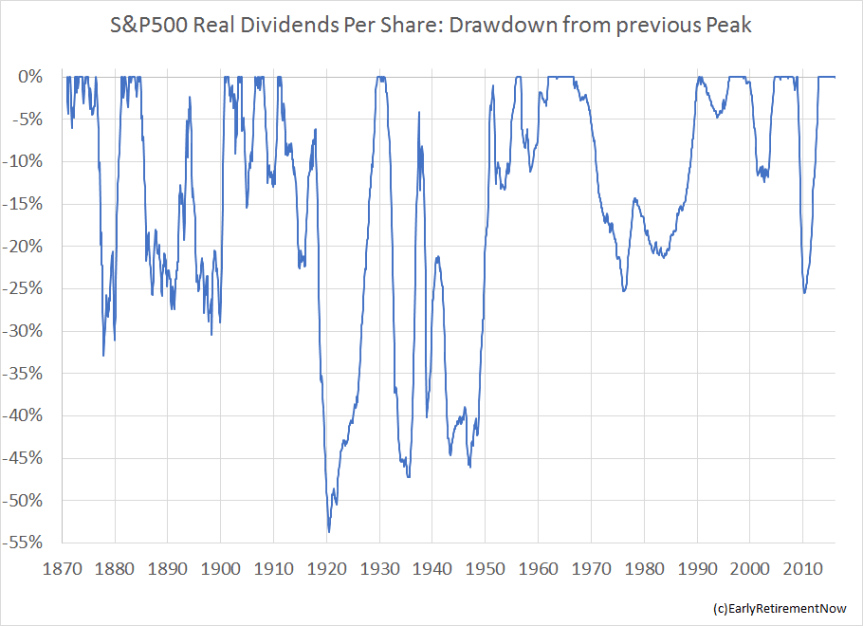

Part of the poor performance of the yield-chasing portfolio is due not only to poor price performance. One ugly little detail that the Yield Shield fans seem to ignore is that even your dividend income will take a hit when the next recession strikes. It certainly did during and after the Great Recession. This is true for the broad market indexes (e.g., the S&P 500) as I have alluded to in a previous post, see the chart with the drawdowns from the peak of real dividends per share:

And it gets even worse; some of the popular dividend boosters – REITs and Preferred Shares – experienced even worse dividend payment streams during and after the Great Recession! Let’s look at the dividend payments per share of the Vanguard REITs ETF (VNQ) and the iShares Preferred ETF (PFF) since 2008 (the peak in per-share income). (Side note: I couldn’t find the USRT dividend stream in Yahoo Finance, so I used the VNQ for this chart!) In the chart below are the per share dividend payments, both in nominal terms and adjusted for inflation. REITs had a sharp drop in dividends (-40%, much worse than the S&P 500!) almost immediately. It took until 2016 to recover to the pre-recession level in inflation-adjusted terms (much longer than the S&P 500).

Preferred Shares kept up their income a little bit better initially but eventually got hit. Really badly! And Preferred Shares look like their dividend income is now down pretty much permanently! More than 40% from their peak in 2008, see below!

Well, the lesson here is that dividends are in no way contractually guaranteed. They can be cut at a moment’s notice. Also, be really careful with preferred shares. They are frequently (mis-)interpreted as a bond alternative, see the Millenial Revolution post. But there’s an important distinction between corporate bonds and preferred stocks! Here is the kind of language you’ll frequently find in a Preferred Stock prospectus (Source: Goldman Sachs Group Inc 6.20% Non-Cumulative Preferred Stock, Series B (GS.PRB) Prospectus, retrieved through PreferredStockChannel.com):

“In the event dividends are not declared on Series B Preferred Stock for payment on any dividend payment date, then those dividends will not be cumulative and will cease to accrue and be payable. If we have not declared a dividend before the dividend payment date for any dividend period, we will have no obligation to pay dividends accrued for that dividend period, whether or not dividends on the Series B Preferred Stock are declared for any future dividend period.”

In other words, the issuer has the option to skip dividend payments. Not only that, there is no obligation to ever make up for that in the future (i.e., the phrase “Non-Cumulative”). This is a stark contrast to a corporate bond where a missed payment would usually be considered a default. So if someone tells you that you can avoid Sequence Risk with Preferred Shares I’d be really, really cautious!

Side note: I don’t want this to sound like I’m bashing Preferred Shares. We hold a small amount in the PFF ETF and a six-figure portfolio of individual Preferred Shares. I also enjoy the impressive yield but I am aware that this is a reward for taking on a risk premium!

Conclusion

Oh, my, I got carried away! I have some more material but we’re already pushing 3,000 words. I’ll do a follow-up soon (see Part 30, published on 3/4/2019). Anyhow, what have I learned over the last few days putting together this post? What can we do about Sequence Risk? Nothing can really solve the problem unless you come up with a market timing algorithm that avoids the occasional equity drawdown altogether. I have studied a few legitimate techniques that alleviate (not solve!) Sequence Risk:

- Guyton-Klinger (see SWR Series Part 9 and Part 10)

- CAPE-based withdrawal rules (see SWR Series Part 18)

- Glidepaths for the equity/bond shares (see SWR Series Part 19 and Part 20)

- A “cash bucket” (see SWR Series Part 25)

But none of these will ever completely shield you from Sequence Risk. And the “Yield Shield” method is even inferior to that. It’s a bit like prescribing Marlboro Reds for enhancing pulmonary health. It ain’t working! In other words, the Yield Shield has the potential to make Sequence Risk even worse, as evidenced in the last recession. Of course, we can’t really tell how this asset allocation will work in the next bear market, but the previous failure of the Yield Shield was probably not just a fluke. As long as you believe that in future recessions dividends will be cut, preferred shares will get into hot water, inflation erodes some of your fixed-income yields, etc. – all pretty reasonable assumptions – then there’s a pretty good chance that this strategy will fail again! I have consistently recommended to my readers to stay away from this strategy. But if you want to be the guinea pig and try this in real-life, best of luck in the next bear market!

Also, make sure you check out the two follow-up posts:

- The Yield Illusion Follow-Up (SWR Series Part 30)

- The Yield Illusion (or Delusion?): Another Follow-Up! (SWR Series Part 31)

Thanks for stopping by today! Please leave your comments and suggestions below! Also, make sure you check out the other parts of the series, see here for a guide to the different parts so far!

Picture Credit: pixabay.com

Seems like the thesis here can be put very simply: If a company gives away money, its valuation will be negatively affected.

Haha, it may actually be that simple! Thanks for stopping by!

So, like General Mills (GIS) who gives away money for over 100 years, its value will be ground zero or even negative?

Come on. Who gives money (dividend) and Who decides value?

No. That’s a gross misrepresentation of my point.

Here is another more reasonable way to ensure you get yield plus growth in yield over time (with the benefit of the security not falling as much as the market due to high yield). Primarily investing in less liquid alternatives that provide high yields. If you invest in NNN leases, infrastructure, re-insurance or specialty high-yield lenders (like TPG Specialty) you can get high yield & growth. If you look at well covered (dividend yield) NNN firms like O, NNN or STOR (which I like the best) they recovered from 2008 quite quickly. TPG Specialty’s team (which I have know since the early 2000s when the they were working at a large bank) has done great navigating the financial crisis. You can also look at Brookfield Infrastructure Partners (an infrastructure fund) or Lancashire Re (a re-insurance firm with the best underwriting in the business).

Packer

I agree with the “less liquid” point, but the caveat is that anything publicly traded is not “less liquid.” Any REIT that’s publicly traded may face the same issues as the USRT fund: the price craters and the dividends are cut.

I can’t comment on the individual REITs you mentioned. They certainly did all right post-2008 but there’s no guarantee you’d have been able to identify the good ones a priory back in 2007.

Personally, I like priveate equity funds with a focus on multi-family housing.

The issue with USRT is the “look through” expense ratio is about 5%. Any REIT fund is a fund of funds. The one type of REIT that has a cost advantage is NNN REITs their expense ratio is 3% or less. If you focus in the low cost NNN REITs (like O, NNN or STOR) you can find a REIT expense ratio close to 1%. So you have a built in 4% expense advantage which is probably cheaper than your apartment fund.

Overall steady state real estate generates returns (pre-fee) in the low teens on a levered basis. IMO the key to getting reasonable returns in real estate is low fees. These funds also have claims equivalent to bond funds first claims on the underlying businesses cash flow & are well underwritten. Given the fee structure you could have identified these before 2008.

I agree with you that with tradable underlying assets you are not going to find a way to get reasonable total returns with an efficient market. However, if your underlying assets are private (such as NNN leases) or some private credit assets is some BDCs or leasing assets you can take advantage of marketability discounts & inefficiencies in these markets. The key in each of these cases is understanding the underwriting for each of these investors in these assets.

I agree with you that multi-family is a good segment especially B grade multi-family that can be upgraded. I know a local REIT manager that has done well that strategy. I personally like the NNN space which this manager also manages and has a fund that is currently yielding 6% with built-in 4% NOI increases via contractual rent increases.

Packer

Something else many don’t think of, is the future total return of the bond market. The standard 60/40 asset allocation approach has worked great the last 40 years when, during a general falling-rate environment, the total return of bonds (the stock “hedge”) were in the 6% range. How are things going to work if/when 40% of your assets are earring 1-2%, or are negative, as we’ve seen just recently. Most new and recent retirees have not experienced the impact of rising rates on the total return of a bond portfolio.

That’s something on my mind, too. I am afraid that we might have a repeat of the 1970s again. Bonds go through multi-decade “phases” see chart below.

From: https://earlyretirementnow.com/2016/05/19/bond-vs-stock-risk/

Phau argues for replacing part of your bond portfolio with SPIAs takes care of that.

I don’t think that works so well for extreely early retirees: in my 40s I get a really paltry annuity payment. And then there’s great risk about how much those nominal payements will be worth 40-50 years down the road.

But I agree that for traditional retirees, age 65+, there’s an advantage to the SPIA, just like Pfau claims!

I agree that traded bond expectations is low, probably the current yield you receive (so may be 2-3% nominal). What I find interesting about some of the alternatives mentioned above is they are structurally like bonds (first liens against growing assets) but have yields of 5 to 9% & solid & growing underlying asset bases. Take TSLX as an example. You a portfolio of first lien loans with a yield of 9% whose underlying collateral value is growing. I have known the team there for about 20 years in their past lives as commercial bank underwriters before they started TSLX. Their underwriting was superb then & is now. They are one of the few BDCs who has a growing NAV. They have about 3% of the portfolio that is below origination grade and have generated about 12% RoE since IPO. Their “look through” interest coverage is about 3x implying a BB credit rating. On top of this, the duration is close 2.5-3 years. The team is value oriented & very opportunistic. Similar “bond like” similarities can be found in NNN real estate firms such as STOR (4% with 5% growth) or other private NNN REITs (that yield 6% with 4% growth). There are also other private first lien fixed & flip loan funds which generate low teens rates of returns or mobile home park funds which can yield mid teens total returns. Other similar types of situations can be found in airline or capital equipment leasers and infrastructure owners like BIP (5% yield with 7% growth). I think if you mix these together you can get a diversified mix of bond-like assets that will provide higher returns than large-cap US stocks.

Packer

All nice suggestions! Will have to check those out.

I was once offered an investment in a private BDC. They certainly look attractive. Good to know that this also exists in the public space.

But notice how this is still very different from the promise of the Yield Shield. If you want to do this high-dividend strategy you better do a lot of analysis before. A far cry from the passive index investing approach.

I agree about the research aspect & the yield shield is just re-assembling public assets in a form that gives you more dividends vs. cap gains which is like moving chairs on the deck of the Titantic.

Packer

ERN, I am a bit late to this party, but recently read a number of your posts (particularly this series on the Yield Shield fallacy) and decided to run a PortfolioVisualizer back test on some assets that I own compared to the baseline IVV/EF portfolio you used. Portfolio 1 contains 60% IVV and 40% IEF. Portfolio 2 contains PDT (a good performing CEF), EPD as a representative of MLPs, O/WPC/CCI as representatives of triple net lease REITs, and ARCC as a representative of BDCs. The Portfolio 2 mix was 25% PDT, 15% EPD, 40% REITs (10% O/20% WPC/10% CCI), and 20% ARCC. The reason I picked them is that I own most of them (except EPD and O) and they have relatively long histories so work better for back testing purposes. I own several other BDCs, REITs, MLPs, CEFs, ETFs, as well as preferred stocks and a couple of bonds but they have somewhat shorter histories. Anyway, from Jan 2005 to Aug 2020 Portfolio 1 had a CAGR of 8.16% and Portfolio 2 had a CAGR of 11.63%. The Portfolio Visualizer-calculated perpetual safe withdrawal rates are 5.95% and 9.0% respectively.

When I ran the backtest withdrawing $50,000 per year (inflation adjusted, from an initial portfolio value of $1 million), I got the following results:

Port 1 Port 2

CAGR 2.71% 7.85%

Final Value $1.5 M $3.3 M

Perpet. W.R. 5.95% 9.0%

Sortino Ratio. 1.31 0.97

Std Dev. 14.57% 17.59%

Portfolio 2 is more volatile than Portfolio 1, with a higher std deviation and lower Sortino Ratio, but in terms of stability of inflation-adjusted withdrawals, ability to withdraw a higher percent, while still ending with a noticeably higher portfolio balance it seems like Portfolio 2 is clearly the winner (though only over 16.5 years, not 30 or 60 years).

The results were not materially different when I ran the P-V backtest using various weights of IVV and IEF (i.e., 80%/20%, 90%/10%, and 100%/0%).

I don’t dispute the results of your Yield Shield analysis, but I think that the results of your analysis may depend on the specific assets and asset classes you chose for your analysis, rather than be generalizable across all higher-yielding assets. It is difficult to do good backtest analysis on a lot of these higher-yielding asset classes because most of the specific stocks and ETFs have been around less than 15 years. And the index ETFs that do exist for backtesting purposes, tend to include a lot of lower-performing, higher-risk assets. For example, REIT index ETFs will typically include mortgage REITs and hotels and some other REITs that have generally not performed very well and are often shunned by DGI investors that use a quality screen. Personally I focus on triple-net lease REITs in essential infrastructure asset categories, as well as MLPs that focus on essential infrastructure (e.g., BIP). I also have a couple of BDCs that have performed well over a reasonably long period of time (MAIN, GAIN). I know that doesn’t guarantee that they will continue to perform well in the future, but virtually nothing is totally guaranteed, except maybe annuities. I also have a bunch of individual cumulative preferred stocks (used to also own PFXF but noticed that it didn’t perform very well so dumped it). I wish I could include individual preferred stocks in P-V but it seems to not let me select them, and anyway, most of the ones I own haven’t been around long enough to include in a back test.

I would be interested in your thoughts on this. And thanks for all of your very interesting contributions to the field of retirement investing.

Thanks for pointing this out.

My exercise here was to showcase how the SPECIFIC asset allocation recommended by some fellow bloggers would have failed relative to the simple 60/40 portfolio.

We can always find “better” portfolios by using the benefit of hindsight and replacing everything that didn’t perform well in the YS portfolio with something that performed really well. But who would have known this in 2005? What if you had replaced the YS ETFs with CEFs that would have blown up during 2009?

Also, if you give the benefit of “pick and choose in hindsight” to the yield-shield crowd, I’d also demand that same benefit for the low-dividend-yield crowd. Let’s replace the IVV ETF in my initial allocation with some “good performing” stocks: GOOG, AMZN, AAPL, etc. and there you go, I get a double-digit return for the low-yield portfolio and easily beat the portfolio stats in your portfolio 2. And you’d have a good point accusing me of “hindsight bias” and “data-snooping.” 🙂

ERN, your point about hindsight and bias and cherry picking are good points. To some extent, even IVV suffers from a weakness of the S&P500 index – a capitalization weighted index definitely is biased toward the most successful, surviving companies, while people’s real-life portfolios typically aren’t. However, the NAREIT equity REIT index (effectively comparable to IVV in your analysis) performed very well from 1972 – 2019 and from 1994 – 2019. No specific REIT selection needed – some performed much better than others, but overall, they performed very well, and in fact better than IVV. Overall, the CAGR from 1972 – 2019 was 11.82%, with 79% of the years having positive returns. It would be interesting to see your analysis repeated but with a healthy slug of REITs (perhaps using the NAREIT equity REIT index data) used in place of some of the Yield Shield portfolio. My guess is that you would get a rather different result.

Disagree. My real-life portfolio is (mostly) the S&P 500.

And by the way, if a company fails in the S&P it will also impact the S&P. Enron, Lehman, etc. all dropped all the way to essentially 0 before being dropped from the index. There is no significant survivor bias in the S&P for that reason. Very different from the “dividend aristocrats” index, etc.!

I very explicitly mentioned that REITs and/or international stocks performed better during SOME recessions. And WORSE during some other events. There is no point investigating further what I’ve already conceded. And conceding this point will in no way invalidate the whole issue I tried to raise here: That in 2008/9 a high-yield portfolio, REIT-heavy and over-weighted on non-US high-div stocks would have done worse from a SoRR perspective.

If you have an idea on how to “fix” the train wreck of asset allocation advice that is the Yield Shield, it is your job to do the work, not mine. Please read the section “But, but, but, have you tried X or Y or Z?” in SWR Series Part 31) where I write:

And it is also your job to prove that your “solution” doesn’t suffer from hindsight bias. Especially on the last point, you’ve already lost. If you look at our discussion here (and many discussions I’ve had with folks before you), the “solution” always relies on some over-fitted asset allocation that would have worked beautifully in hindsight, but nobody would have found this reasonable in 2007.

Well I think if your point is that the specific portfolio recommended by a specific person would have failed, then I can see your point. But you seem to have strongly implied a more general point in this series on Yield Shield that all higher yielding portfolios with an income-focused (i.e., dividends/interest/distributions) objective will fail on the SORR issue and it is that point that I am disagreeing with and suggesting that you should set the record straight for your readers. There are some higher-income portfolios focused on income (without an explicit focus on capital gains) that can and did do significantly better than your IVV/IEF portfolio and do tend to mostly solve the SORR problems (though not completely in all circumstances and not guaranteed). And I think that your later posts about real estate do half-way acknowledge this point. It seems that the higher proportion one has of fairly stable (hopefully growing with inflation) income and the closer one is to normal retirement age the lower the risk. I guess one of the things I have noticed about your research is that, since it is mostly focused on very early retirement (in a person’s 30s or 40s), some of the conclusions that are reached may not be completely applicable to someone who retires in his later 50s (still “early”) like me. I only have less than 4 years until I can claim SS. I have a small pension with a COLA that I am getting now, I have lifetime group health insurance for which I have to pay my share (about 30%), I have pretty stable rental property income, and I have quite stable and growing income (not price stability) from my financial portfolio. Obviously real hyperinflation could wipe things out, and some really serious and long-lasting downturn in the US economy and stock markets could damage our ability to live the way we want, but that is also true for the IVV/IEF portfolio as well.

Look, we’re talking in circles here. You have not convinced me in any way how a rational investor should have picked the “right” income assets in 2007. What objective, replicable screen/asset allocation rule would you have used in 2007 to screen out the bad REITs in 2007and buy only the good ones?

Shifting and pivoting to real estate is not going to do the trick. I know I use RE myself. But keep in mind that a lot of mom-and-pop RE investors were wiped out in 2008/9 even worse than the 60/40 portfolio. So, RE is not as fool-proof as many people think.

Since there didn’t seem to be any way to reply to your comment below I’ll reply here. As you noticed in my comment above, I said that you don’t need to pick specific REITs (and weed out the bad ones) to win. The equity REIT index handily beat the S&P 500 over that period.

Look, I’m not saying that the IVV/IEF portfolio has been a bad portfolio to own in the past, although it will be interesting to see how the IVV/IEF does over the next 10 years, given how low interest rates are. Clearly that portfolio has done well and with very low volatility. But I am saying that there are portfolios that focus on income (partially as a solution to SORR) that might do better than the IVV/IEF portfolio (or at least as well). And you seem to be stubbornly refusing to accept any feedback that this series of articles on high-yield related to SORR make overly generalized conclusions about the results from analyzing 2 very specific portfolios that don’t represent what a lot of other dividend-focused retiree investors incorporate in their portfolios. You would be doing the entire universe of your readers a big favor to have a more open mind and consider how to analyze the problem more broadly and incorporate varying combinations of REITs, MLPs, BDCs, DGI stocks (e.g., the dividend aristocrats) and preferred stocks (not just the PFF ETF which is heavily non-cumulative financial stocks) into your analysis in order to arrive at a broad conclusion that is reasonably justified by the evidence.

‘Nuf said. Moving on.

All that matters is the total return. We can dance around this issue all day long. But TR matter, nothing else.

Late in an expansion, like now, I have moved more into Treasury bonds. The next recession will likely arrive in the next 12 months. That means stocks will sell-off 6 to 9 months before that.

At that point I would consider 30% VYM 20% PFXF, and the remainder in dividend growth stocks and REITs to be a high yielding portfolio with growth. If I find more attractive stocks I would buy less PFXF.

As the market recovers, I will sell shares of PFXF and replace with companies that are showing good growth, along with a 4% dividend. The goal is to create a portfolio with 4% yield and capital appreciation.

That should provide stable and growing income for quite some time.

Late in the next expansion, if I am still around, I will sell over-priced stocks and buy some Treasuries again.

I’d not call the recession over the next 12 months yet.

Also, depending on what’s the nature of the recession, your high-yielding REITs and PFXF will get hammered a lot more than the 60/40. So, same answer as before: beware of high-yielding assets: they are no solution to Sequence Risk!

Your strategy is dependent upon being “right” 2x:

– Accurately choosing the date that you leave the market

– Accurately choosing the date that you return to the market

That’s a tall order. Good luck.

That’s a good point! And what do you do when you’re wrong about the exit and the market keeps going up? I know people who got out long time ago and are still waiting for the S&P 500 to drop below 1800 again. 🙂

This is a tremendous post!

Can you explain this: “Side Note: The reason why I put the “Yield” in that table in quotation marks is that this is the 12-month rolling (backward-looking!) yield according to Yahoo Finance, so especially for the bond indices, the actual forward-looking yield is even a little bit higher.”

Good question! The 12-m rolling might be too low in a rising yield environment. If today’s actual forward-looking yield is 3%, but the yield was rising from 2% to 3% (linearly) over the last year then the average backward-looking yield is 2.5%, much lower thatn the actual forward-looking yield of 3%.

Hi ERN,

Thanks for the write-up. Chanced upon it recently. I came out with a portfolio structure that consist of 20% equity, 20% long term treasury 40% REITs and 20% Gold portfolio and found that this combination works best in terms of weathering a economic downturn, particularly one that includes significant inflationary risks such as the one in the early 1970s. I used the website portfoliocharts.com to generate that structure where it details that such a portfolio structure actually has a safe withdrawal rate of 6.3% and much less volatility compared to your standard 60:40 equity to bond structure.

If you simplify the portfolio structure into 4 asset classes using IVV to represent equity, TLT to represent bond, VNQ to represent REITs and GLD to represent gold, the gross returns would be 6.45% over 2007-2018 and inflation-adjusted return at 4.6%. This underperforms the standard 60:40 structure but I believe if we have a high-inflation environment, this structure will significantly outperform that of your standard structure and yet generate higher yield from the REITs component.

Any thoughts on this?

I’d be cautious about portfoliocharts because the historical range is far too short. It ignores the worst possible historical retirement starting points (1929, 1965/66, 1968).

Gold and REITs worked pretty well in the 1970 (inflationary recession).

REITs would have been a tota unmitigated disaster in 2008/9, of course, so you are hoping/betting that the next recession is different from the last. Which is usually a good assumption, but again, be aware of the risks you’re taking there.

I’ve just finished reading the “quit like a millionaire” book and glad I came across your post. I do specifically remember that the author said the yield shield portfolio is not intented to be used long term though. And she’s said that after the first 5 years (once you ride out the sequence risk period) then you should allocate your asset back to the original risk profile/allocation. Is that what you’ve done in your simulation? Just curious here as I’m trying to take everything in and learn. Thanks for your insight.

Well, they clearly don’t know what they’re talking about. As if the Yield Shield wasn’t bad enough, the approach they propose to save their failed model, i.e., Yield Shield for 5Y and then moving back to the non-YS allocation would have made the performance even worse. You get hit initially because you allocated to the risky assets during the worst of the bear market, but then moving back to the safer assets you’d have missed out on the eventual recovery of the risky assets.

What I showed in my Glidepath posts (Parts 19,20): you want to do the exact opposite, i.e., cautious asset allocation initially and then moving back into risky assets. THAT would alleviate Sequence Risk (somewhat).

So you don’t agree with Kristi and Millennial-Revolution’s approach for initial period of FIRE? Why exactly in popular language? I was planning on doing something like that so I don’t have to sell any shares to pay my bills. So you don’t recommend that apparently for what I got from the post (sorry I’ve dyslexia)

This is not about agree/disagree. The data/facts don’t agree with MR. You do have to sell shares only because

a) dividends can be cut,

b) preferred share dividends can be cut,

c) REITs can go bust,

d) your corporate bonds go into default

e) your corporate bond interest income may not keep up with inflation

Read the post again (and parts 30 and 31) and this will be clearer! 🙂

All this is just too much for my brain to grasp. Ern.. ..I’ll just use a broad market index and withdraw 3% ok? No overthinking this thing and trying to get extra juice.

Oh, that’s OK. As long as your approach makes sense to you and passes the smell test, you should just run with that. Don’t worry about the details! 🙂